Today’s Headlines

- ASX 200 up 9 to 6107. Rally fades again.

- High 6130 Low 6094. Modest volumes.

- Shorts playing catch up.

- Banks and resources better with energy a standout.

- TLS steadies. A2M Sours.

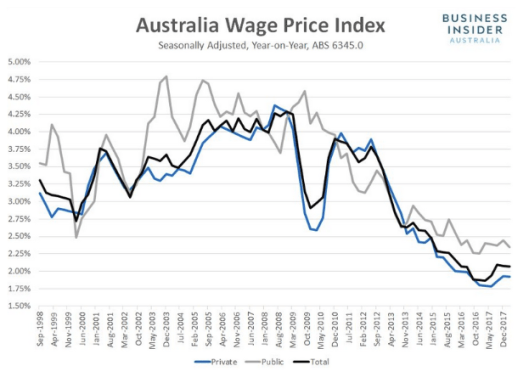

- AUD dips on wage growth or lack of. 74.34c

- Bitcoin slips to US$8214

- AUD Gold $1294 weaker still.

- US futures up 14.

- Asian markets mixed with Japan and China

STOCK STUFF

Movers and Shakers

- AMP +1.03% Geoff Wilson warns on ‘rotten to the core’.

- BAL -9.89% follows A2M down.

- SM1 -4.33% A2M sentiment as supplier.

- TTT +0.74% opens new facility in Melbourne.

- NBL +15.74% successful raising.

- WHC +6.81% NHC +3.75% better commodity prices.

- DMP +4.23% short covering perhaps.

- IVC +5.14% brokers upgrade.

- ELD +3.80% rally continues post numbers.

- HVN +2.58% short covering.

- CYB -4.97% company presentation.

- VOC -5.41% sector woes.

- TLS -0.35% steadies.

- APT -2.68% profit-taking.

- TCL -1.62% bond proxy stocks ease.

- CPU +2.75% European acquisition.

- Speculative stock of the day: Envirosuite (EVS) +65.85% after a major contract win worth $1.5m in the Middle East for its city-wide odour monitoring and management systems.

- Biggest risers – WHC, WPP, IVC, FXL, DMP and JBH.

- Biggest fallers – A2M, BAL, SIG, CYB, VOC and SM1.

TODAY

- Computershare(CPU) +2.75% Has entered into an agreement to acquire Equatex Group, a leading European employee share plan administrator based in Zurich, from Montague Private Equity for EUR354.5m. The acquisition is expected to be EPS accretive in FY19 and estimates it can make savings of at least US$30 million annually from integrating the business. It will be funded from existing cash and available debt facilities.

- A2 Milk(A2M) -13.11% Trading Update and F18 Outlook. Revenue for the 9 months ended 31 March 2018 were up 70% to NZ$660 million, reflecting continued sales growth in both nutritional products and liquid milk. A2M also warned it includes the impact of seasonal sales from key China selling events weighted towards 1H18. Outlook – FY revenue of NZ$900-920m, taking into account the planned move to the new infant formula packaging during Q4. FY gross margins broadly consistent with 1H18. Marketing investment NZ$82-87m given higher expenses in the US and China in 2H.

- Myer (MYR) +16.00% Q3 FY2018 sales for the 13 weeks to 28 April 2018: Total sales down 2.7% to $635.3m and down 3.1% on a comparable basis; Online sales up 49.4% to $35.9m; Total year to date sales down 3.4% to $2,355.0m or down3.0% on a comparable store basis; Online sales year to date up 49.0% to $141.1m. Sales affected by warm weather, particularly for winter apparel, shoes and New CEO and MD John King will start on 4 June. No more quarterly sales updates from FY19.

- Coca-Cola(CCL) +0.11% Catherine Brenner will not run for re-election.

- Fletcher Building (FBU) –0.83% has completed the NZ$750m retail component of its entitlement offer, raising NZ$229.5m

- Qantas (QAN) +0.79% 2018 foreigners potentially held relevant interests in 44.13% as at 2 May, up from the 43.6% held at 29 December 2017. (Foreign investors are not permitted to hold more than 49%, and notice must be given when foreign ownership exceeds 44%).

ECONOMIC NEWS

- Westpac-Melbourne Institute consumer sentiment fell 0.6% to 101.8 in May. Sentiment index was 99.9 before the budget and 104.8 post budget.

- Wages rise less than expected in 1Q, up 0.5% in the first quarter slightly below market consensus of a 0.6% rise and after a downwardly revised 0.5% increase in the previous period. Wages were +2.1% from a year earlier, according to the Australian Bureau of Statistics.

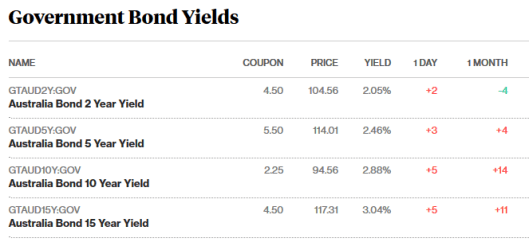

BOND MARKET UPDATE

ASIAN MARKETS NEWS

- North Korea has pulled out of peace talks after military exercise stokes uncertainty.

- Anwar Ibrahim freed after 11 years.

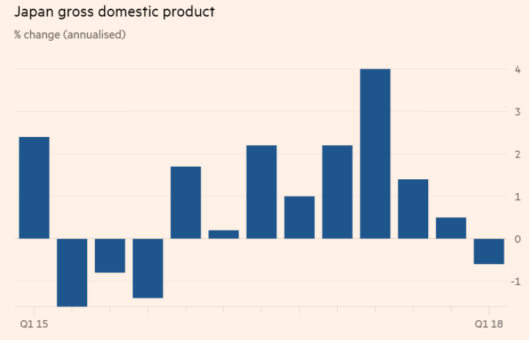

- Japan’s economy contracted in the first quarter for the first time since 2015, according to an early reading that showed a drop of nearly 1 per cent in domestic demand.

- Sign of the times. WeChat is working on a messaging app for trading bond without breaking compliance rules.

EUROPE AND US MORNING HEADLINES

- Paddy Power Betfair is in talks to acquire fantasy sports site FanDuel, as the UK and Ireland-based bookmaker looks to capitalise on the lifting of a federal ban on sports betting across the United States.

- The author of Bonfire of the Vanities has died. Tom Wolfe RIP.

- UK Government continues to be bogged down with Brexit issues. Thomson Reuters will shift its forex derivatives business out of London in Brexit preparation

- Britain’s economy is entering a “menopausal” phase after passing peak productivity, a deputy governor of the Bank of England has suggested. Ben Broadbent compared the current slowdown in growth and wages to a lull at the end of the 19th century, when the height of the steam era was over but the age of electricity was yet to begin.

- UK shares are the cheapest on record, at least during peace time,with the yield gap now at 2.2%. Citi suggested a number of British companies to consider. Its “top six” larger companies, all rated a “buy” by the firm, are pharmaceutical giant AstraZeneca, insurer Aviva, building materials company Ferguson, miner Rio Tinto, bank Standard Chartered and advertising firm WPP. The FTSE All Share index has gone nowhere this year and now yields close to 4%.

And finally………………

For the audio version of this report click here

Clarence

XXX