Today’s Headlines

- ASX 200 up 20 to 5881.

- High 5903 Low 5877.

- Royal Commission continues to take its toll.

- May run and run says Corman.

- Joyce suggests breaking up banks.

- Miners rally on BHP report and commodity prices.

- Energy gaining strength.

- Switching from tech to resource stocks

- AUD flops then rallies to 78.06c.

- Bitcoin rallies to US$8173.

- US futures up 36.

- Asian markets rally with China CSI up 1.31% and Japan up 0.28%.

STOCK STUFF

Movers and Shakers

- PLS +4.82% ORE +5.30% lithium back.

- IGO +7.69% metal prices.

- WSA +7.82% nickel price rise

- AMP -2.92% still in the dog house. No surprise.

- CBA -0.01% charges dead clients for advice.

- LNK -1.20% broker downgrades.

- WTC -4.14% profit-taking.

- APX -4.40% more profit taking.

- API -2.33% results underwhelm on discounting fears.

- AWC +7.09% Alcoa results.

- JMS +3.75% finding support.

- FXJ +5.34% merger rumours with SWM +3.03%

- CYB +3.85% brokers keeping the faith post-PPI hit.

- Speculative stock of the day: Aura Energy (AEE) +28.57% update on its Haggan Vanadium project in Sweden containing 13.1bn pounds vanadium as an inferred resource. Vanadium is 18 times the uranium grade. AEE will maintain 70%-80% of spin-off.

- Biggest risers –IGO, AWC, WSA, MIN, CLQ, FXJ and COE.

- Biggest fallers –MOE, CGF, WTC, APT, APX and ECX.

TODAY

- BHP – +2.83% Production numbers – FY guidance unchanged for oil, coal both metallurgical and energy. Iron ore production guidance narrowed to between 1700-1785kt. Olympic Dam though revised down 135Kt. The company now expects to produce between 272m tonnes and 274m tonnes for the full 2017-18 financial year, just down from its previous guidance of 275m tonnes and 280m tonnes with problems on car dumpers. Copper production expected to be up around 6%. US shale sale is progressing to plan. All major developments are on track and according to plan.

- Challenger Financial(CGF) –3.14% Total assets under management up 3% to $78.6bn. Life net book grew 74% to $629m and funds net flows were $1.2bn. Guidance of NPBT of between $545m-$565m representing an 8% growth. ROE is expected to be 18% pre-tax.

- Iluka Resources(ILU) +0.60% Quarterly review as the company noted strong market conditions in zircon and titanium dioxide. Zircon/synthetic rutile increased 10% in the March quarter. Net debt reduced to $183m. Cataby is on target and on budget.

- South32 (S32) +4.58% Production record at Mozal Aluminium. Increased guidance at Australia Manganese by 6% and South African Manganese by 5%.

- Santos (STO) –+0.33% Free cash flow breakeven at $36 a barrel and free cash flow generation strong. $246m generated in free cash in the quarter. Total debt is now at $4bn and had cash of $1.5bn giving net debt of $2.5bn. With regards to the takeover, shareholders are urged to do nothing. The company has warned that the bid may be certain given issues surrounding FIRB.

- Wesfarmers (WES) -0.27% Quarterly coal update with coal production of 2,869,000 tonnes 3.5% below previous quarter. Met coal though was up 4.9% whilst steaming coal down 20.5%. The company also completed the sale of its Curragh Mine to Coronado Coal Group at the end of March.

- Alumina (AWC) +7.09% Alcoa first-quarter earnings results out on the AWC Production of alumina was 3mt. Gross distributions from AWAC was US$266.2m with AWC expecting to receive distributions of US56m from AWAC entities. Alumina net debt was US$114m.

- Adelaide Brighton (ABC) +0.96% extends the contract with BHP for the supply of cement and lime to its Olympic Dam mine.

- WAM Capital (WAM) –1.26% Will cover the shortfall in the dividend reinvestment plan at a price of 235c per share, a premium to NTA.

- Speedcast International (SDA) +0.93% is refinancing its existing bank loans and arrange a new revolving credit facility.

ECONOMIC NEWS

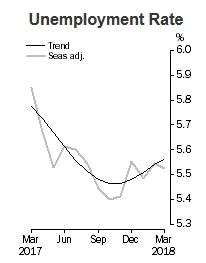

- The ABS labour force results show that unemployment has increased for March, rising 3,500 to 735,000 people to site at 5.6%.

- Employment increased by about 14,000 with part-time employment accounting for a majority of that growth. Just 1,000 new full-time jobs were added during the month of March.

- February’s gain was revised to a 6,300 loss after a seasonal reassessment

- Western Australiarecorded the biggest jump, going from 6.2% to 6.4% and remains the worst state for unemployment figures.

- The jobless rate hit 5.6% and the participation rate came in at 65.5%.

- Momentum slowing in jobs with only 4,900 added. Bloomberg had been expecting 20,000 jobs to be added to the economy in March. Some analysts have forecast the next RBA meeting could be live for a rate cut. Dreaming.

BOND MARKETS

ASIAN MARKET NEWS

The top bureaucrat in Japan’s Ministry of Finance has resigned after allegations that he sexually harassed a number of female reporters.

EUROPE AND US MORNING HEADLINES

- Amazon has disclosed it has more than 100m members of its Prime subscription programme — the first time the e-commerce giant has revealed the figure.

- The IMF has warned against excessive global borrowing. The world’s debt load has ballooned to a record $US164 trillion ($211 trillion). Global public and private debt swelled to 225% of global gross domestic product in 2016, the last year for which the IMF provided figures.

- May is looking like a pivotal moment for oil markets as Trump could impose sanctions again on Iran. The sanctions waivers are next due for renewal on May 12. If sanctions do “snap back” there could be a 180-day period to wind down business operations involving Iran. Friday sees a meeting of some OPEC nations and their allies.

- Angela Merkel is set to lend her backing to a eurozone bailout fund, modeled on the world’s lender of last resort, the International Monetary Fund. the EMF would act as a “rainy day fund”, set up in order to safeguard against future recessions and financial crises such as that seen in 2009.

- Deutsche Bank lost another senior executive on Wednesday with chief operating officer Kim Hammonds stepping down from her post, in further proof of growing turmoil at the top of the bank.

- Is this the next flashpoint in the wall of worry? This from a Citigroup analyst: “The historical relationship between the curve and implied recession probabilities are highly non-linear: implied probabilities grow very fast when the curve moves into inverted” Clear.

- This could halt the commodity rally. Rusal officials met Chinese companies and traders this week to discuss the possibility of buying alumina and selling aluminum in the Asian country as U.S. sanctions freeze out the Russian producer from markets around the world.

And finally………

Another torrid day in the Royal Commission…the one they didn’t want because the regulators were on top of it..yeah right!!!

So…..

Negotiations between union members and their employer were at an impasse. The union denied that their workers were flagrantly abusing the sick-leave provisions set out by their contract.

One morning at the bargaining table, the company’s chief negotiator held aloft the morning edition of the newspaper, “This man,” he announced, “called in sick yesterday!”

There on the sports page, was a photo of the supposedly ill employee, who had just won a local golf tournament with an excellent score.

A union negotiator broke the silence in the room.

“Wow!” he said. “Just think of the score he could have had if he wasn’t sick!”

Clarence

XXXX