Today’s Headlines

- ASX 200 limps to close down 5 at 5904 as politics takes focus.

- High 5938 Low 5902. Strong volume.

- War breaks out in Coalition.

- Results season continues.

- Banks mixed, resources take a breather.

- Healthcare in focus.

- AUD stronger at 79.56.

- Bitcoin rallies hard to US$10,148.

- AUD Bullion around $1356.

- US futures up 16 points.

- Asian markets better with Japan up 1.09%. China closed.

STOCK STUFF

Movers and Shakers

- IPH -6.10% broker downgrades following results.

- PME -6.76% results disappoint.

- S32 -5.14% selling continues as brokers downgrade.

- FXJ -4.69% goes from bad to worse.

- HSO +6.46% positive broker comment.

- SSM +6.21% rally continues.

- BWX +3.50% gaining friends.

- BRG +3.88% positive broker upgrades.

- NCZ +11.86% zinc price rises.

- JIN +4.24% good results. Again.

- FMG -0.74% two billion opportunities milestone to aboriginal business.

- FLN +12.12% rock bottom?

- MEA -3.53% John has a betting account.

- PRT -15.38% disappointing results.

- BIG -3.06% profit taking.

- BFC -4.00% merger with DataDot (DDT) +33.33%.

- MOC +6.14% strange move.

- Speculative stock of the day: New IPO Pearl Global (PG1) +35.00% after a successful listing for the tyre recycler.

- Biggest risers – HSO, SSM, GSC, CDD, VRL and BWX

- Biggest fallers – IPH, PME, SGR, WHC, S32 and FXJ.

TODAY

- IOOF (IFL) –2.19 1H net profit A$94.8m, down 39%. Underlying profit A$94.8m, up 19%. The company said the acquisition of ANZ Wealth Management is progressing as planned. Interim dividend of 27c, up 4%.

- Medibank Private (MPL) +3.62% 1H net profit A$245.6m versus A$231.9m, up 5.9%. 1H income A$3.53bn, up 1.7%. Health insurance operating profit $277.3m, up 11.2%. Net claims up 2.5%. Interim dividend of 5.5c. Expects underlying revenue trends to continue for the FY, and management expenses to be slightly higher in the 2H, but less for the FY.

- Primary Health Care (PRY) +3.40% 1H net profit A$22.1m, up 4.7%. Revenue A$856.5m, up 5.9%. EPS 4.2c versus 4.0c on the pcp. Interim dividend 5.1c. The company said its improved EBIT contributions from Pathology, Imaging and Corporate offset a decline in Medical Centres that were moving to a new operating model. Primary medical centres EBIT was down $4.9m; Imaging EBIT increased by 14.7%, and pathology EBIT up 3.1%. PRY said its results included $19.7m of non-underlying items which related to restructuring and investment in strategic initiatives. Profit guidance of A$92m – A$97m was confirmed.

- Baby Bunting (BBN) +5.76% 1H net profit A$3.5m, down 33% on year. Interim dividend of 2.8c.

- iSelect (ISU) +7.29% 1H net profit A$478,000, down 81% on year. Revenue up 7% to $83.3m. Dividend of 1.5c. Customer leads up 5% to 2.1m. Unique visitors down 500k to 4.1m. Conversions were underpinned by Energy and Telcos at 10.4%. Sales units up 6% to 224k.

- Star Entertainment (SGR) –6.28% 1H net profit $32.9m, down 77%. EBITDA A$200m, down 34%. Revenue A$1.2bn, up 0.5%. Interim dividend of 7.5c. The results were impacted by low international VIP rebate business win rates, and significant items from debt restructuring. Domestic revenue up 4% for Sydney; and 8.7% for Queensland. The company said 1H trading for Sydney was softer than expected, and the start to the 2H has been mixed.

- Sims Metal (SGM) +1.31% 1H revenue A$2.98bn, up 25%. Net profit A$8.2m, up 17%. Cash of A$390m. Interim dividend of 23c. The company said external market conditions are steadily improving and ferrous scrap prices have remained firm so far in the 2H. Underlying return on capital is on track to exceed FY targets.

- Whitehaven Coal (WHC) -4.51% NPAT of $257.2m driven by a 32% increase in margins per tonne. Met coal average price of US$111/t and thermal coal at US$95/t. EBITDA of $460.6m. Interim dividend of 13c. Net debt down 4% to $146.9m. FOB costs at $60/t as previously announced.

- Rio Tinto (RIO) +0.48%% could face higher costs on its $US5.3bn expansion of Mongolia’s Oyu Tolgoi mine, after Mongolia ordered the miner to source power for the mine domestically within four years.

- Citi upped its average gold price forecasts for 2018 by around 7% to $1355 an ounce.

- Copper is on track for its biggest weekly gain since November 2016, up 6.3% so far on the back of optimism over global growth and weakness in the USD.

ECONOMIC NEWS

- RBA governor Philip Lowe said he expected property price growth and debt to expand at a slower pace than incomes to help defuse a dangerous build-up in housing debt, reiterating that his next move was more likely to be a rate hike. “Above-trend growth at a time of low unemployment should be expected to see inflation lift, even if that lift is gradual because of factors that are affecting wage and price pressures globally,” Dr Lowe told a hearing of the House of Representatives economics committee. Dr Lowe said an infrastructure construction surge was generating jobs and expanding the economy’s future productive capacity.

- Lowe also said that US tax cuts were ‘very problematic’ because they blow out the budget deficit and Australia should not go the same way. He says that over the next six years US budget deficits will average 5% of GDP even though unemployment is low and the economy is strong.

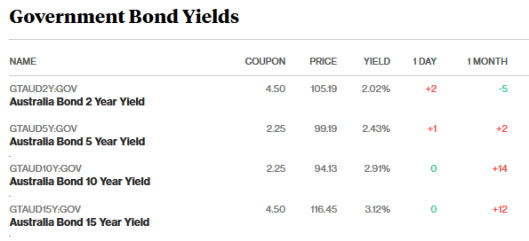

BOND MARKET UPDATE

ASIAN MARKETS

- Prime Minister Abe nominated Haruhiko Kuroda to lead the BOJ for another five-year term.

EUROPE AND US MORNING HEADLINES

- 5 days of US rallies best since 2011.

- Investors withdrew US$6.3bn from U.S. high-yield junk bond funds in the past week, the second-biggest amount ever, as concern mounted that equity-market volatility was spreading.

- S. regulators rejected a bid by a Chinese-linked consortium to take over the Chicago Stock Exchange.

- HNA Group has further cut its stake in Deutsche Bank

- Uber could be hit with tough new regulations under proposals from Transport for London (TfL) to improve passenger safety among private hire vehicle operators.

- Who is the most miserable country? Stand up Venezuela. Take a bow South Africa.

And finally……Thank as usual Hans

| Sex on the Sabbath A man wonders if having sex on the Sabbath is a sin, because he is not sure if sex is WORK or PLAY. So he goes to a Priest and asks for his opinion on this question. After consulting the Bible, the Priest says, “My son, after an exhaustive search, I am positive that sex is WORK and is therefore not permitted on Sundays.”

In other words, he goes to see a Rabbi. The Rabbi ponders the question, then states, “My son, sex is definitely PLAY. Shocked, the man replies, “Rabbi, how can you be so sure it is PLAY when so many others tell me sex is WORK?” The Rabbi softly speaks, “If sex were WORK, ………..my Wife would have the Maid do it. |

=

Have a great weekend

Clarence

XXX