Today’s Headlines

- ASX 200 down 14 to 5972.

- High 5986 Low 5949.

- Banks weigh as Telstra rallies.

- Miners fail to fire with

- US futures up 55.

- Aussie dollar firms after retail numbers at 76.50c

- Bitcoin hanging tough at US$11,510.

- Asian markets mixed with China CSI 300 up 0.53%, Japan down 0.20% and HK down 0.30%

STOCK STUFF

Movers and Shakers

- JBH +6.76% Amazon fizzer. Better retail sales.

- GEM +5.29% oversold yesterday. Brokers still keen.

- REA -2.46% Broker downgrade.

- CSL -0.65% R&D update with Phase III trials.

- S32 +3.68% Reaffirms guidance.

- ALQ +0.44% director buying.

- MTS +3.00% still gaining support following results.

- TLS +3.14% potential NBN write off helping.

- BIG -4.89% Apple TV update

- GSW -13.95% Industry superfund buying.

- APX -4.61% Profit taking.

- MFG +6.24% Fund inflows and strong equities.

- Speculative stock of the day: RTG Mining +90.00% after Philip Miriori was confirmed as Chairman of SMLOLA with formal reconciliation signed

- Biggest risers – MFG, JBH, HVN, SGM, GEM and S32.

- Biggest fallers – EWC, PLS, KDR, BWX, GTK.

TODAY

- South 32 (S32) +3.68% The company has a strategy and business update today in Perth. It has reaffirmed production guidance for FY18. Sustainable capital expenditure of US$470m with the reduced amount from US$500m the result of deferral at the Appin Colliery.

- AWE –10.00%The indicative bid from CERCG has been withdrawn.

- CSL –0.65% The company will spend US$550m on phase III trials of a new treatment aimed at preventing secondary heart attacks. The clinical trials of the potential breakthrough therapy, CSL112, will be the largest ever undertaken by CSL, take four years to complete and have 17,000 patients enrolled from 1000 sites around the world.

ECONOMIC NEWS

- The Reserve Bank of Australia decided to once again leave the official cash rate unchanged at 1.5% for the 16th consecutive month.

- See here for the full details of the RBA statement

- Retail Sales have risen by 0.5% beating consensus of a 0.3% rise. This follows a 0.1% rise in September 2017.

- The current account deficit fell $539m to $9,125m in the September quarter 2017

- There was a fall of $376m on the balance on goods and services, resulting in a surplus of $3,056m in the September quarter 2017. The primary income deficit fell $1,044m to $11,968m.

- Sydney and Melbourne combined accounted for more than two-thirds of Australia’s economic growth during 2016-17, a concentration rare on a global scale.

- Sydney is Australia’s hottest capital city economy. Analysis suggests that to rein in Sydney’s economy, the Reserve Bank would have to push up its cash rate from 1.5% to 3.5%. To rein in Melbourne’s it would have to push it 2.25%. In Brisbane, Perth and Adelaide, the cash rate would have to be pushed down to 0.25%.

BOND MARKET

ASIAN NEWS

- The Chinese Caixin/Markit services purchasing managers’ index (PMI) rose to 51.9 in November, up from 51.2 in October and the highest reading since August.

- World’s biggest Starbucks to open in Shanghai. Unlucky.

- Australian government to legislate against political meddling by foreign powers.

- Uniqlo owner hits two-year high as rebound continues.

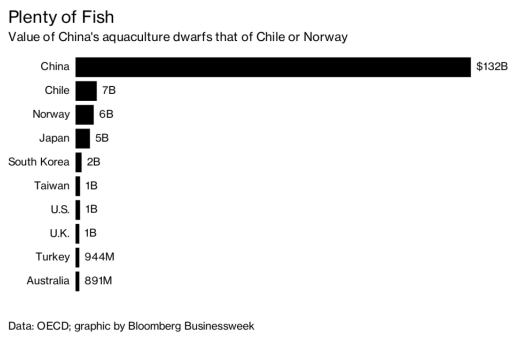

- Bit scary for our local aquaculture companies. China has tripled fish output in a decade.

EUROPE AND US MORNING HEADLINES

- Brexit deal falls through over Irish border dispute.

- London has attracted more visitors than any other European destination this year, despite a spate of terror attacks in the capital. The number of European visitors to London rose by 24%.

And finally……….

Clarence

XXXX