Today’s Headlines

- ASX 200 rallies hard up 33 points to 6049 as cash put to work.

- NAB ex dividend knocks 10 off index.

- High 6052 Low 6018.

- Banks and miners lead charge.

- Industrials kick too. Telcos and energy struggle.

- AUD firmer at 76.82c.

- US futures up 26.

- Asian markets higher with Japan up 1.68% and China CSI up a modest 0.05%.

STOCK STUFF

Movers and Shakers

- VAH +9.09% on delisting hopes.

- NUF +5.28% acquisition cheers/substantial holder

- PLS +5.38% GXY +1.55% ORE +5.18% KDR +9.09% lithium rally continues

- PNI +3.09% investor presentation

- BUD +9.59% another positive deal announced.

- BIG +11.71% positive revenue update.

- NAB -3.38% ex dividend.

- STO -2.72% investor day.

- DMP -3.47% AGM guidance under-whelms.

- GSW -4.20% profit taking.

- GMG +2.59% operational update.

- NCZ -4.48% profit taking.

- COH -0.66% Citi downgrades.

- PMV +4.00% short squeeze.

- WSA +3.34% higher nickel prices.

- PTM -2.79% profit taking continues.

- XRO -1.20% delists in NZ in January.

- Speculative stock of the day: IAB -48.00% following a trading update with its Hostworks business performing well below expectations. Hostworks provides cloud hosting and cloud solutions. Will not contribute meaningful earnings.

- Biggest risers – BIG, VAH, KDR, JHX, NVT and PLS.

- Biggest fallers – YAL, SM1, DMP, PTM, APX and MLD.

TODAY

- Santos (STO) –2.72% Investor Day today, and an opportunity to brief on its Transform-Build-Grow strategy which was presented to the market last year. It said it focused on five core assets: Cooper Basin, Queensland, PNG, Northern Australia and Western Australia Gas – all of which are set to provide a stable base for production for the next decade, and deliver higher production in 2018 (allowing for planned plant shutdowns). Non-core assets and their natural field decline, are expected to offset the gains. Production guidance is expected to be towards the upper end of 58-60 mmboe and sales volumes guidance: 72-78 mmboe, due to lower forecast third party gas sales volumes and lower non-core asset volumes. rallied from 320c to 470c

- James Hardie (JHX) +7.60% 2Q results this morning. NPAT US$73.9m and US$135.6m for the half year – a decrease of 1% and 4% on the pcp respectively. EBIT US$104.1m for the quarter and US$192.4m for the half, another decrease of 2% and 6% on the pcp respectively. Fibre cement volume decreased 2% and was flat for the half year, net sales were up 4% for the quarter and 5% for the half.

- Domino’s Pizza (DMP) 3.47-% Sales in Europe grew 8.5%, and stopped going backwards in Japan, where they edged up 0.1% after falling 0.6% last financial year. Same-store sales worldwide increased by 5%. DMP has opened 32 new stores so far this financial year, and expects to open another 180 to 200 new stores by the end of the year. Affirmed guidance for Australian and New Zealand same-store sales growth of 7% to 9% and between 0 and 2% in Japan. It upgraded its guidance for Europe to 6% to 8% from 5 to 7%. It also affirmed guidance for its net profit to grow by about 20%.

- Xero (XRO) -1.20% Net loss after tax for the six months to the end of September narrowed to NZ$21.1m ($14.7m), from NZ$43.9m for the same period the previous year. The company has also announced it will formally delist from the NZX on February 2nd. Last day of trading in NZ is 31st January.

- Zipmoney (ZML) +1.42% Quest Payment Systems has made the ZML platform available on its payments terminal. Under the deal Quest will offer ZML across its entire Australian network.zipPay does not require any change to existing POS software either so integration should be no problem.

- Flight Centre (FLT) +1.98% AGM today with forecasts from CEO that profit before tax for the full year would come in between $350m and $380m, which would represent growth of between 6.2% and 15.6% on the group’s 2017 results. Flight Centre’s international businesses is shaping up as key growth drivers for 2018, with its North American unit and its Europe, Middle East and Africa unit on track to beat their 2017 results. They were responsibly for 30% of group profit in 2016. Bullish outlook for its 2018 financial year earnings, tipping a strong first half could see profit rise by more than 15% in the full year.

ECONOMIC NEWS

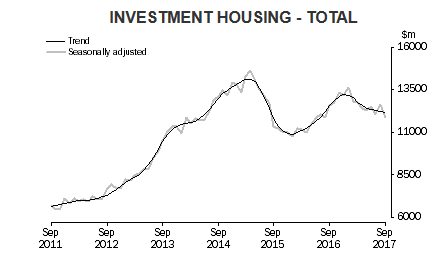

- Housing finance

- The total value of dwelling commitments excluding alterations and additions (trend) fell 0.1% in September 2017 compared with August 2017, and the seasonally adjusted series fell 3.6% in September 2017.

-

- The number of owner occupied housing commitments (trend) rose 0.7% in September 2017, following a rise of 0.8% in August 2017.

- The number of commitments for owner occupied dwellings financed by banks (trend) rose 0.6% in September 2017, following a rise of 0.8% in August 2017. The seasonally adjusted series fell 2.5% in September 2017, after a rise of 1.3% in August 2017.

- The value of outstanding housing loans financed by Authorised Deposit-taking Institutions (ADIs) was $1,616b, up $5b (0.3%) from the August 2017 closing balance.

- New Zealand’s central bank forecast it may need to raise interest rates slightly earlier than previously expected as capacity pressures and a weaker currency stoke inflation. The central bank said inflation will reach its 2% target much sooner than previously expected, and it brought forward its forecast for a rate hike to the second quarter of 2019 from the third. The RBNZ also said new government’s restrictions on foreign home buyers would likely help to moderate house price inflation.

BOND MARKET

ASIAN MARKETS

- The Chinese producer price index (PPI) rose 6.9% in October from a year earlier, in line with the growth rate in September when it hit a six-month high, data released by the National Bureau of Statistics.

- China’s consumer inflation, which has stayed well within Beijing’s 2017 target of 3% this year, also accelerated more than expected to 1.9% from 1.6%in September, due to higher food prices and low base effects.

- Food prices fell 0.4% on year versus a 1.4% drop the prior month

- Sectors including coal mining and iron and steel both saw price gains decelerate to the slowest paces since late last year.

- A 26-year high in the Japanese market. But only a slight gain for a decade.

- It’s only a few days away from Singles Day in China. 11th Analysts estimate US$24bn in sales with Alibaba dominating. It has a novel idea and has enlisted 10% of Chinese convenience stores to sell its goods and get parcels delivered.

EUROPE AND US MORNING HEADLINES

- Trump pledged on Thursday to change a US-China trade and economic relationship that is “far out of kilter”. Massive Chinese love in. No sign of a trade war at all. Presidential Trump is doing well.

- AT&T has been told by the US Department of Justice that it needs to sell CNN, Time Warner’s cable news channel, to get its $84.5bn acquisition of the media company approved.

- Chinese search engine company Sogou has priced its American depository shares at US$13, coming in at the top of the expected range and putting the size of its November 9 initial public offering at US$585m.

- You think NAB was ‘visionary’ Deutsche Bank chief hints at thousands of job losses. CEO Cryan sees tech bringing lender into line with peers at ‘half’ its 97,000 headcount. Makes NAB look good.

- Tencent has taken a 10% stake in Snapchat’s parent company Snap, a vote of confidence after the messaging app’s horror results this week. Tencent has a US$2bn stake.

And finally……………..

Hawk and Tom were talking in the bar.

Hawk said, “I just got kicked off the course for breaking 60.”

Tom looked at him, amazed. “Breaking 60? That’s amazing!”

Hawk smiled and said, “Yeah, I never knew a golf cart could go that fast!”

I was hiking once with my girlfriend.

Suddenly a huge brown bear was charging at us, really mad.

We must have come close to her cubs.

Luckily I had my 9mm pistol with me.

One shot to my girlfriend’s kneecap was all it took.

I could walk away at a comfortable pace.

I finally got one of those roof boxes for the car. It’s very practical. I can barely hear my kids now.

Clarence

XXX