All this talk about Harvey!

- ASX 200 falls another 51 points to 5669

- Decisively breaks range at 5700.

- Late rally saves blushes.

- High 5706 Low 5646.

- North Korea launches missile over Japan.

- Banks and financials lead market down as risk rises.

- BHP now bigger than CBA.

- Gold miners buck the trend.

- Energy slips but contained. Miners outperforming slightly.

- Consumer and healthcare stocks weaken.

- Discretionary stocks slide as USD earners fail too.

- Builders under pressure.

- AUD slightly higher at 79.26c.

- US Futures down 100.

- Asian markets slightly weaker on missile threat. China CSI down 0.22% and Japan -0.63%

MT STUFF: Stopped out of BEN for a 9.1% gain. BKL good results today.

STOCK STUFF

Results Today

- ALU +11.76%

- CAB +4.46%

- BUB -10.22%

- CTX +0.90%

- DOW +2.04%

- BKL +7.48%

- SDA +1.48%

- MTR -2.05%

- TPW -1.64%

- SFH -23.08%

Movers and Shakers

- AGO +11.11% better profit results.

- FMG +1.36% iron ore still holding up.

- NAN -5.08% profit taking after bounce.

- RWC +2.19% positive broker sentiment.

- MMS -3.97% recent run unwinds.

- CNU -6.55 % broker downgrades following results. A NZ TLS?

- MSB -10.91% entitlement offer closes raising $50.7m

- NEC -0.68% increased competition.

- SWM -4.76% on CBS/TEN news.

- TPW -1.64% tips maiden profit.

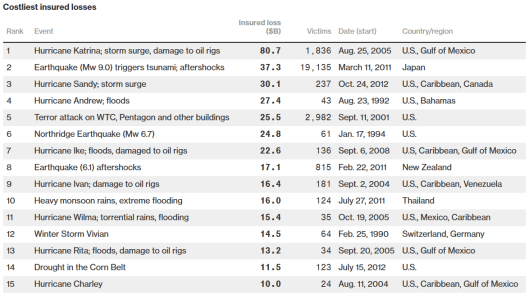

- QBE -% has limited exposure to Hurricane Harvey.

- Speculative stocks of the day: Core Exploration (CXO) +50.00% after making a strategic placement to a Chinese company, Yahua, to advance the Finniss Lithium project. Yahua is a $2.2bn listed company in Shenzen. There is also a commercial offtake agreement

- Biggest risers – ALU, BKL. RSG, BIN, SAR, AGI, and WGX

- Biggest fallers – CNU, AAC, PNI, SRV, RCR and ASB.

TODAY

- Downer EDI (DOW) +2.04% Full year results. Excluding any contribution from Spotless, NPAT was up 0.5% to $181.5m, revenue was up 5.7% to $7.8bn and EBIT up 0.3% to $277.8m. These results all beat full year guidance. The company will pay a final dividend of 12 cents per share, in line with prior corresponding period. For FY18 the company has given NPAT guidance between $85m -$100m or around $190m excluding Spotless synergies and contributions.

- Specialty Fashion Group (SFH) -23.08% Full year results. The company posted a net loss of $8.4m. EBITDA was up 6.6% to $26.7m, revenue was down 2% to $808.9m and net debt was reduced to $8.3m (pcp $13.3m), reflecting subdued Australian retail conditions and low wage growth. The company will pay no final dividend.

- Blackmores (BKL) +7.48% Full year results. The company reported Revenue down 3% to $692.79m, NPAT down 42% to $58.028m and the company will pay a final dividend of 140 cents per share.

- Atlas Iron (AGO) +11.11% FY17 net profit of $48m versus net loss of $159m for FY16. Revenue up 11% to $871.1 due to rising iron ore prices. Net operating cash flow up 394.5% generating $122.9m of positive cash flow. C1 cash costs up 2.9% to $35/t. Iron ore shipments were down 0.7% to 14.4mt.

- Cabcharge (CAB) +4.46% FY17 net loss $90.6m. Net profit from continuing operations rose 33% to $13.7m. Final dividend of 10c. The company says it intends to spend an extra $8m on marketing and technology in FY18.

- Mantra (MTR) -2.05% FY17 net profit up 14.2% to $47.2m. Total revenue up 13.7% to $689m. Underlying EBITDAI up 12.7% to $101.2m. Keys under management up 10%. MTR met FY17 guidance, supported by six new property acquisitions during the year and strong revenue growth from key markets such as Sydney, Melbourne, the ACT and the Sunshine Coast.

- Bingo Industries (BIN) +4.86% Full year results. Net revenue came in at $209.7m, pro forma EBITDA was $64.1m and pro forma NPAT was $32.0m. These results were all above guidance. The company highlighted its strong balance sheet supported by high operating cash flows and expects to introduce a dividend in H1 FY18. FY18 pro forma EBITDA guidance has been lifted to $89m as the company’s national expansion on track, Victorian entry is ahead of schedule.

- Caltex Australia (CTX) +0.90% Half year results. The company posted a 1H replacement-cost net profit of $307m, up 21% pcp and towards the top end of guidance. However, NPAT attributable to equity holders was down 17% to $265m. Higher 1H oil prices lead to a 20% increase in total revenue of $10.16bn and the interim dividend will be 60c, up 20% pcp.

- Regis Resources (RRL) +2.53% Full year results. Profit after tax was up 24% to $138.16m largely due to increases in delivered gold prices and gold production. EBITDA was up 8% to $253.3m and the final dividend will be 8 cents per share fully franked, bringing the full year dividend to 15 cents per share.

- Retail Food Group (RFG) +0.83% Full year results. Revenue was up 27% to $349.3m, EBITDA was up 12.1% to $123.4m and NPAT was up 14% to $75.7m. The company will pay a final dividend of 15 cents per share resulting in a full year dividend of 29.75 cents per share (+8.2% pcp). FY18 NPAT guidance has been lifted by 6% excluding acquisitions, integration and restructuring costs.

- Speedcast (SDA) +1.48% Revenue up 143% to US$246.3m Underlying EBITDA US$52.8m. Fully franked dividend of 2.40c.

ECONOMIC NEWS

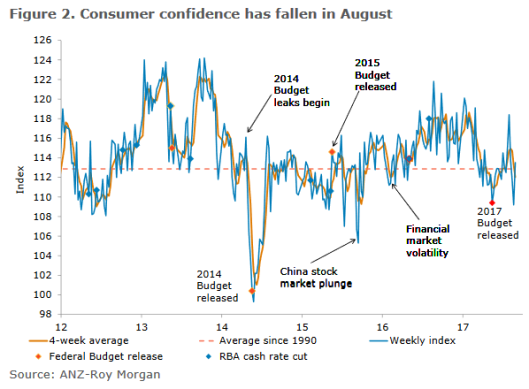

- The ANZ Roy Morgan consumer confidence number this week broke the down trend, jumping 3.9% as sentiment rose across the board.

- The HIA reported new home sales fell to their lowest level in four years in July as apartment sales dropped nearly 16%.

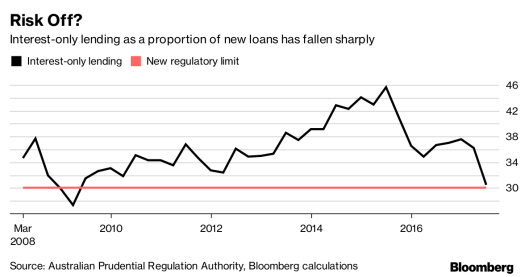

- The proportion of interest only loans has fallen to its lowest level in more than 8 years. 30% is the new normal.

- The value of alterations and additions is expected to grow 8.3% in 2017/18 and 6.8% in 2018/19 according to IBIS World. The average cost for house renovation is expected to be between $30,000 and $40,000.

- The NSW plate #4 has sold to a Chinese billionaire for $2.45m.

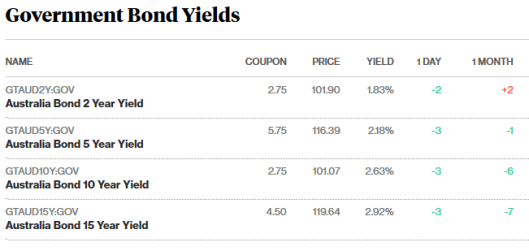

BOND MARKET UPDATE

ASIAN NEWS

- Short sellers do not always win. China Evergrande Group, the developer targeted by short sellers this year for its high debt levels. Shares up strongly today after a promise to reduce debt and up 400% for the year.

EUROPE AND US MORNING HEADLINES

- Amazon has slashed the prices of its newly acquired Whole Foods group on its first day of ownership.

- Domino’s and Ford are testing driverless cars for pizza delivery in Michigan. Not completely driverless as the technician who monitors the car will then give the pizza to the customer once they knock on the window. The question is how ill customers react to the walk out the front to collect the pizza. It is not about A to B but car to customer.

- How big is Harvey going to get?

- The EU has accused the UK of not taking the Brexit negotiations seriously. The sides are a (EU) country mile apart. There are three main sticking points before they even start trade negotiations. How much will the UK have to pay in the settlement? How will the only hard border between Northern Ireland and Ireland work and citizen rights? Anyone who thought this was going to easy will be very much mistaken. Highly unlikely to make the deadline set out under Article 50. Will get messy. Really messy.

- Penzance has narrowly failed to become the world record holder for the number of pirates in one place as some did not manage to make it out of the pub. Not even an inflatable parrot could not seal the deal. The town needed over 14,231 pirates to claim the record. Aaah!

And finally….

A couple met on separate trips at Myrtle Beach and fell in love. They were discussing how they would continue the relationship after their vacations were over.

“It’s only fair to warn you Jody.” the man said. “I’m a golf nut. I live, eat, sleep and breathe golf.”

“Well, since you’re being honest, so will I,” Jody said. “I’m a hooker.”

“I see,” he said. Then brightening, he smiled. “It’s probably because you’re not keeping your wrists straight when you hit the ball.”

Boom Boom!

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com