On the tapes…

- ASX 200 rises 22 points to 5765 on CBA results.

- High of 5777 Low 5693.

- CBA results cheer bank sector.

- Consumer confidence falls again, stocks weaker as a result

- BAL back with a vengeance.

- USD earners rally. Gold miners rally too on AUD bullion price.

- Energy sector down. Telcos continue to struggle.

- Dalian iron ore futures are up 0.1%.

- North Korean issues pull Asia back

- Japan down 1.31% China CSI 300 down a more modest 0.05%

- US Futures down 28.

- AUD back below 79c at 78.83 on North Korean issues.

STOCK STUFF

- MYX -7.45% continues slide on profit downgrade.

- JHG +5.59% after results and increased focus on cost cutting.

- CSL +1.20% on falling AUD.

- LYC +3.23% continues recent run.

- IFL +3.18% broker upgrades after result.

- ACX +3.23% shorts covering.

- GEM -2.84% heavy volume.

- TME -2.19% Amazon woes and broker downgrades.

- Speculative stocks of the day: ZIP +94.44% after doing a deal with emerging Convo app to integrate core Zipt IP. Good pedigree and could be company changing. Company entered a trading halt late.

- Biggest risers – JHG, EVN, CGC, OGC, MSB and MSB.

- Biggest fallers –MYX. SRX, IRI, SKC, CVW and MCY.

TODAY

- CBA +0.57% has reported another record full-year profit. Total income was up 5%, coming in at $26,005m and Cash profit was up 4.6% to $9,881m. Commonwealth Bank plans to pay a final dividend of $2.30 a share, up from $2.22 last year and bringing the full-year payout to $4.29. The bank said its financial performance supported the board’s aim of stable

- com (CAR)+2.96% has reported their full year results. Revenue was up 8% to $372m and EBITDA was up 4% to $177m. Reported NPAT came in flat at $110m, primarily due to a $7.1m iCar write-down in the first half. The final dividend has been declared at 21.5c, up 10% on pcp.

- ResApp Health (RAP) –77.42% The company has been down as much as 77% this morning following disappointing study results.

- Bellamy’s (BAL) +4.06% Chinese authorities lifted a licence suspension on the infant formula maker’s recently acquired Camperdown canning facility.

ECONOMIC NEWS

- The survey of 1200 people by the Melbourne Institute and Westpac Bank found consumer sentiment fell 1.2% in August, from July when it edged up 0.4%. The index reading of 95.5 was 5.5% lower than in August last year, the lowest since April 2016.

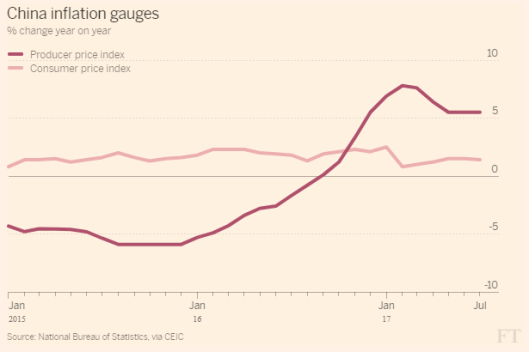

- China Inflation rose less than expected in July; CPI up 1.4% following a 1.5% lift in June; while PPI increased 5.5% – same as previous month.

- Local home loan approvals fell short of expectations, rising only 0.5% in June, missing market hopes for an increase of 1.5%. value of loans for investment housing rose 1.6%.

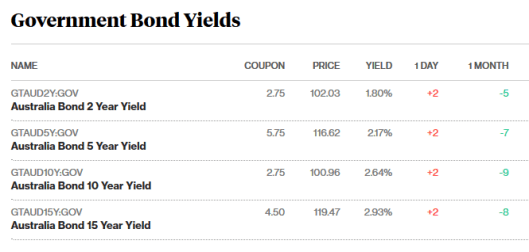

BOND MARKET UPDATE

ASIAN NEWS

- Chinese CPI rose 1.4% over the 12 months, following a 1.5%rise in June, while PPI gained 5.5%, the same as the previous month.

- Dalian Wanda’s Hong Kong-listed subsidiary, Wanda Hotel Development, requested a trading halt on Wednesday for a “possible asset restructuring”.

EUROPE AND US MORNING Headlines

- Disney axing distribution deal with Netflix and will no longer provide Buzz Lightyear or Woody from 2019 No more infinity and beyond.

- Italy industrial production, Greece CPI.

- UK housing market held back by stamp duty a study shows. Chancellor urged to change it. Fat chance.

- Murdoch faces more questions and scrutiny in GBP 11.7bn takeover of Sky. The UK government has asked the regulator to look at 21st Century Fox’s broadcast record.

And finally….

Clarence

XXX

Get a Global take on things at http://www.ntmarkets.com