ASX 200 reverses early strong gains but survives to close up 6 points at 5862.5 as US launches Syrian missile strike. Gold and energy stocks rally as risks rise. Consumer stocks slid after a profit warning from The Reject Shop (TRS) and banks rally late to save blushes. Asian markets buck ‘risk off trades’ with Japan up 0.49% and China up 0.15%. AUD falls to 75.20 before recovering to 75.31c. US Futures down 39.

For the week, the ASX 200 has fallen from 5865 to close today at 5862.5, a loss of very little.

The Big Bank Basket fell from $186.13 last Friday to $182.90 as the AFR Wealth and Finance Summit rolled through town this week with APRA waring of capital issues ringing in investors ears.

STOCKS AND SECTORS

- Miners slipped on the missile strike with BHP -0.32%, RIO -1.10% and Fortescue Metals (FMG) -3.02%. Base metal stocks also slid with South 32 (S32) -1.36% still feeling the effects of the Cannington underground fire reported yesterday.

- Energy stocks higher as risk off was embraced and the oil price kicked, Woodside (WPL) +1.26%, Santos (STO) +2.94% and Oil Search (OSH) +1.23%. Coal stocks eased back after recent gains with Whitehaven (WHC) -0.90% and Stanmore Coal (SMR) -unchanged.

- Gold miners the big beneficiaries of the uncertainty with miners rising led by Newcrest (NCM) +2.78%, Northern Star (NST) +5.58% and St Barbara (SBM) +2.96%

- Industrials gave up gains with consumer stocks badly affected by the update from The Reject Shop (TRS) -35.48%, JB Hi-Fi (JBH) -1.30%, Premier Investments (PMV) -1.19%, Harvey Norman (HVN) -1.84% and Mantra Group (MTR) -2.41%

- Healthcare mixed as Mesoblast (MSB) -3.95% came off the wave on profit taking. Fisher and Paykel (FPH) -0.44%, Sigma Pharma (SIP) -1.59% and Mayne Pharma (MYX) -1.44%

- IT and telcos continue to trend lower as questions on sustainability of the Telstra (TLS) -0.22% dividend were raised by one broker. Vocus Group (VOC) -4.27% resumed SOPs today and Superloop (SLC) -2.95% also lost momentum.

- Banks and financials started well but the midday reversals saw them close slightly lower with the Big Bank Basket down to $182.90. Insurers rallied in the last hour with Suncorp (SUN) -0.15%, IAG +0.17% and QBE Insurance (QBE) +0.39%

- Speculative stock of the day: De.mem (DEM) +125.00% raised $4.5m in an IPO for the waste water treatment membrane technology developed in Singapore.

CORPORATE NEWS

- The Reject Shop (TRS) -35.48% after a horror day for shareholders, another downgrade in ‘challenging’ retail conditions. The company now expects full year profits of around $12.5m versus $17.1m last year. The company also warned that it may not be able to declare a final dividend in 2016-17 as it struggled with a weaker retail environment and execution issues.

- Estia Health (EHE) -2.15% received some clarification from a Queensland property group Sentinel, on its plans for the aged care provider. The property group is looking to acquire a controlling interest in EHE and require an unnamed operator to acquire 60 out of the 68 centres.

- Helloworld (HLO) +6.67% upgraded guidance today from between $47m-$51m to between $52m- $55m. Trading conditions remain challenging but margins are being maintained and the synergy benefits from the recent AOT merger will be delivered by June year end.

- Seek (SEK) +2.45% has moved to privatise its Chinese jobs portal Zhaopin and delist it from the NYSE. Seek and its private equity partners will buy the outstanding Zhaopin shares for $US18.20 in cash per ADR, or $US9.10 per ordinary share. The deal values Zhaopin at $US1.01bn. Seek, which currently owns 61.2% of shares in Zhaopin

BOND CORNER

ECONOMIC NEWS

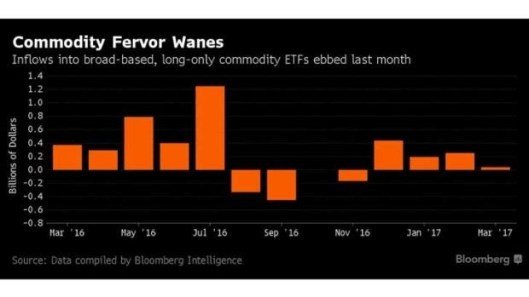

- The Bloomberg Commodity Index, which tracks returns for 22 components, has dipped about 4% since this year’s peak in mid-January. The gauge fell 2.7% in March, the first monthly loss since October.

- Ratings agencies have warned of an unwinding of Australia’s overheated house prices, but say the strength of the banking system and its regulators would ensure any falls are “orderly”. S&P Global Ratings said risks within the system were elevated, but regulators had acted to cool demand and ensure the resilience of the banking sector.

- The Insurance Council has indicted that total losses from the cyclone are expected to top $1bn.Aurizon (AZJ) said today that repair work would take longer than expected on its Blackwater coal haulage line, and would reopen on April 10 under restricted conditions. The railway link from Moura to Gladstone is now expected to be restored by April 12, a week earlier than expected originally.

- Scott Morrison has talked down the prospect of any major changes to the Petroleum Resource Rent Tax (PRRT) as a result of the current review. Positive for the sector. Last year the tax provided revenue of $880m, $120m short of expectations, and a further shortfall in excess of $200m is expected this year. PRRT receipts averaged around 0.2% of GDP in 2000-01 but have fallen to an average 0.12% in the period 2002-03 to 2015-16.

ASIAN NEWS

- President Trump has been compared to President Duerte of the Philippines, and his Asia brother from another mother is implementing a tax amnesty to boost revenue to pay for big infrastructure spending. The government will target tax evaders and beef up compliance before adopting an amnesty program. The government needs funds to pay for US$160bn of infrastructure projects.

EUROPE AND US

- US jobs number tonight. Expect a number around 180,000 for non-farm payrolls in March. Of the 235,000 added in February, 28,000 were in manufacturing, a sector that had added only 7,000 jobs year-over-year. There were 8,000 mining jobs added that month, bringing total hiring in the sector to 20,000 since it hit a low in October.

- A former FX trader has been cleared of market manipulation in London and spent most of his time in court tweeting about the experience.

- Uber rival Lyft is raising more than US$500m to give the group a valuation of around US$6.9bn.

- Spotify plans to go public this year without selling any new shares. The company is going to conduct what is known as a ‘direct listing’ where no new shares are issued or sold but it creates a market for existing shareholders to sell if they want. The company is expected to be valued at over US$10bn. Spotify is under pressure to go public due to the terms of a $1bn bond it issued last year which carries an increasing interest rate the longer it stays in private hands. This gives it an incentive to go public even if it does not have to raise extra cash.

And finally…..

A man comes home after a terrible round of golf, his worst ever. He plops down on the couch in front of the television, and tells his wife, “Get me a beer before it starts.”

The wife sighs and gets him a beer. Fifteen minutes later, he says, “Get me another beer before it starts.”

She looks cross, but fetches another beer and slams it down next to him. He finishes that beer and a few minutes later says, “Quick, get me another beer, it’s going to start any minute.”

The wife is furious. She yells at him “You’ve been out golfing all day! Is that all you’re going to do tonight? Drink beer and sit in front of that TV? You’re nothing but a lazy, drunken, fat slob, and furthermore…”

The man sighs and says, “It’s started…”

Clarence

XXXX