ASX 200 disappointed yet again after a promising start which saw the index touch 5801 but once again we saw profit taking in banks and jobs numbers derail the optimism for a close up 11 points to 5786, on a match out rally. Miners in vogue, financials and industrials sour. Asian markets up modestly with Japan up 0.18% and China up 0.41%. AUD up to 77.05c and US Futures up 30.

STOCKS AND SECTORS

- Miners had a good day out following the rout in the USD last night on Fed moves. BHP +3.72%, RIO +2.30% and Fortescue Metals (FMG) +4.43%. Base metals also did well Syrah Resources (SYR) +9.83% after announcing a sales and marketing session and Independence Group (IGO) +6.41% doing well.

- Iluka Resources (ILU) +% also another standout. Energy stocks rallied hard led by Santos (STO) +5.35% Origin Energy (ORG) +3.65% and Karoon Gas (KAR) +9.23%. Coal stocks not so enthusiastic with Whitehaven (WHC) -0.35% and New Hope (NHC) unchanged.

- Gold miners boomed as bullion rose. Strange that in AUD terms it was far less impressive but let’s not it stand in the way of a good story. St Barbara (SBM) +6.05%, Evolution Mining (EVN) +4.37%. Stand out in a bull market was Westgold (WGX) -1.54% slipping but they are trending against the grain.

- Industrials sloppy as consumer stocks lid on the jobs data. Harvey Norman (HVN) -2.22%, Super Retail (SUL) -1.84%

- Healthcare still weak with Ramsay Health Care (RHC) -1.73% as aged care providers also slipped Estia Health (EHE) -3.23%. Just for fun a quick look at medicinal cannabis stocks as it’s a hot sector at the moment. Stemcell United (SCU) -8.11%, MMJ Phylotech (MMJ) -%, Medlab (MDC) +1.12% and Ascann Group (AC8) +23.00%

- IT and telcos dominated by Telstra (TLS) +1.28% starting to find friends as a defensive perhaps and with the yield, is running against the tide. Speedcast (SDA) +1.10% and Chorus (CNU) +1.05% also helping the sector out.

- Banks and financials the bull market wrecking ball today with the Big Bank Basket down to $182.29 from $184.10 yesterday. More predictions of housing woes, Basel IV requirements and higher rates being passed straight on to borrowers hurting. Wealth Managers too fell with Macquarie Group (MQG) -1.07%, Platinum Asset Management (PTM) -1.19% and BT Investment (BTT) -0.91%.

- Speculative stock of the day: Queensland Bauxite (QBL) +60.00% another cannabis hopeful announcing today that the investment in Medical Cannabis looks to be paying off as the company has been granted a licence to grow ‘plant’ varieties at a private location in NSW. The company will display its results at the Sydney Hemp Health and Innovation Expo at the end of May.

CORPORATE NEWS

- Myer (MYR) -5.26% after announcing a 5.6% increase in profits to $63m which beat estimates but traders were negative on the comments from Richard Umbers on the January and February numbers. The company hopes it has seen the bottom but fingers crossed does not seem to satisfy the market.

- Chow Tai Fook has bought now not to be floated Atlinta Energy for more than $4bn. This is the HK group’s first foray overseas and means the FIRB will have another deal to look at along with Duet Group (DUE) being bought by a Chinese company too.

- National Australia Bank (NAB) -2.44% has raised rates on variable home loans for both owner occupiers and investors. The new variable rate for owner occupiers is up to 5.32% from 5.25%. Rates on residential investment home loans up to 5.80% from 5.55%.

- Slater and Gordon (SGH) unchanged is now heading for a restructure after local and overseas banks sold their debt positions of around $700m. It is expected the new debt holders will participate in a debt for equity swap, where they will exchange their debt for shares in a restructured Slater and Gordon. Not good news for existing holders who get seriously diluted.

- Seymour Whyte (SWL) +21.82% after another mining service company has fallen to a non-binding bid from Vinci Construction with a 136c-143c cash bid. There is also the possibility of a special dividend to use up the $17.8m franking credits the company has.

- Hats off to AMP Capital (AMP) -% that is selling out of some of its less ethical investments. The fund manager has sold out of the company that makes landmines and cluster bombs. Now that really is unethical.

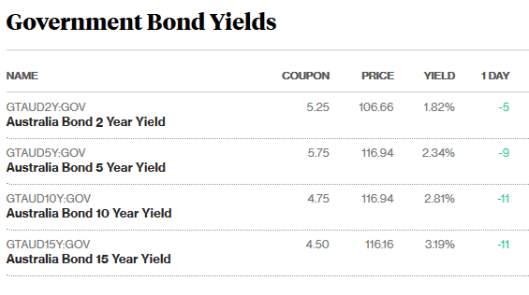

BOND CORNER

ECONOMIC NEWS

- Unemployment has jumped to 5.9% from 5.7% with trend unemployment at 5.8%. Full time jobs rose 27K with Part time down 33.5K. The participation rate was steady 64.6%.

- Seems that economists were pretty underwhelmed with the rise and the underemployment number. Probably puts any thoughts of a rate rise off for some time. Not that it matters when the banks are raising rates anyway.

- Wage forecasts from the RBA going nowhere either.

ASIAN NEWS

- The Bank of Japan kept monetary policy steady maintaining its short-term interest rate target of minus 0.1% and a pledge to guide the 10-year government bond yield at around 0% via aggressive asset purchases.

EUROPE AND US

- The Dutch election turned out to be a non- event. Always had that potential with the complicated proportional representation system. Looks like euro leaders will be breathing a sigh of relief. Just France and Germany to come.

- Backflip with pike from UK Chancellor as he has had to reverse National Insurance (bit like Medicare levy) increases leaving a GBP2bn hole in the country’s finances.

- Indian billionaire Anil Agarwal has launched a plan to buy GBP2bn worth of shares in Anglo American. Mr Agarwal’s controls Vedanta Resources. a FTSE 250-listed company though he does not intend to make a takeover offer. A year ago, he tried to combine Anglo with Hindustan Zinc and was knocked back.

And finally…..

A man went to the Police Station wishing to speak with the burglar who had broken into his house the night before. “You’ll get your chance in court.” said the Desk Sergeant. “No, no no!” said the man. “I want to know how he got into the house without waking my wife. I’ve been trying to do that for years!”

Clarence

XXX

Get more Clarence at http://www.marcustoday.com.au

Get a Global take on things at http://www.ntmarkets.com