ASX 200 finishes on a sour note down 46 points to 5739 as resources, healthcare and banks falter. Industrial results continue to dominate with gold miners better. Asian markets weaker with Japan down 0.52% and China down 0.27%. AUD pushes higher to 77.16c with US Futures down 17.

For the week, the ASX 200 has fallen from 5805 to 5739 around 1.1% as the index played second fiddle to results.

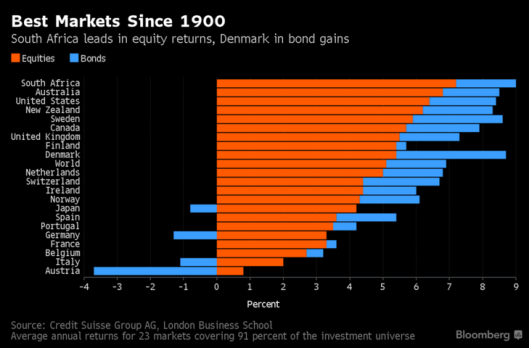

And its official the best equity market returns over the last 116 years came from commodity rich countries.

STOCKS AND SECTORS

- Miners caught in the commodity downturn with BHP -3.02%, RIO -4.15% and Fortescue Metals (FMG) -3.38% together with BlueScope Steel (BSL) -4.39%. Base metal stock s fared slightly better with South32 (S32) -1.60%, Sandfire (SFR) -2.24%, Oz Minerals (OZL) -1.35% and Metals X (MLX) -1.14%.

- Gold miners a bright spot in a sea of troubles. Resolute Mining (RSG) +4.79%, Perseus Mining (PRU) +5.88% and Ramelius (RMS) +2.88% although local producers fared less spectacularly due to the increasing AUD.

- Energy stocks slipped with the exception of Woodside (WPL) +1.01%. Elsewhere Origin Energy (ORG) -3.08% ex dividend, LNG -%, Whitehaven Coal (WHC) -% and Toro Energy (TOE) -5.92%

- Banks and financials weaker but not catastrophic, ANZ -0.67%, Macquarie Group (MQG) -0.76%, Henderson Group (HGG) -1.08% and wealth manager BT Investment (BTT) -1.33%

- Industrials dominated by results with MYOB (MYO) -6.78% following a sell down by Bain Capital of 17%. Consumer staples Wesfarmers (WES) -0.46% and Woolworths (WOW) unchanged. Retailers fell with Lovisa Holdings (LOV) -2.49%, JB Hi-Fi (JBH) -1.39%, Harvey Norman (HVN) -1.56% and Baby Bunting (BBN) -5.56% having a dose of controlled crying. Food stocks mixed with Costa Group (CGC) +5.01%, Huon Aquaculture (HUO) -1.62% and Wellard (WLD) -10.81% and Blackmores (BKL) -0.19%.

- Healthcare in casualty today with CSL -1.88%, Impedimed (IPD) -6.71%. Ansell (ANN) -2.29% and Estia Health (EHE) -4.00%

- IT and Telcos struggled as Touchcorp (TCH) -9.09%, Prophecy International (PRO) –77% -%, Hansen Technologies (HSN) -4.13%, Computershare (CPU) -3.32%. In telcos TPG Telecom (TPM) -1.23%, Superloop (SLC) -2.03% and Vocus Group (VOC) -0.43%. Big winner Nextdc (NXT) +12.30% as shorts scrambled.

- Media and consumer discretionary stocks bucked the down draft with WPP AUNZ (WPP) +6.28%, Event Hospitality (EVT) +3.50% and Prime Media (PRT) +5.08% although Isentia (ISD)-1.51% continued down as did Ardent Leisure (AAD) -2.37%.

- Speculative stock of the day: Ardea Resources (ARL) +50.00% after the company announced the KNP cobalt zone pre-feasibility study now underway in Kalgoorlie. This stock is one of the stable of cobalt stocks we wrote about on Tuesday.

CORPORATE NEWS

- Automotive Holdings (AHG) -4.18% reported a net profit for the December half of $38.6m, down 19.8% on a year ago. Revenue rose 7.6% to $2.96bn.

- Austin Engineering (ANG) +8.82% said net loss narrowed to $5.7m from $22.5m last year. Revenue from continuing operations slid 5.7% to $91.1m. Normalised EBITDA flatlining, down from $2.8m a year earlier, in line with guidance.

- Bellamy’s (BAL) -3.80% said its first-half net profit fell 47% to $7.236m from $13.656m in the year-earlier period. Revenue rose 12.5% to $118.297m from $105.143m a year ago.

- Billabong (BBG) -2.40% said its interim net loss rose to $16.05m from $1.587m from a year-earlier. Revenue fell 9.6 % to $511.03m from $565.44m a year ago.

- Cabcharge (CAB) +6.63% reported a loss of $106.75m from a $24.4m profit. The company is paying a franked 10c interim dividend and an 80c special dividend

- Corporate Travel (CTD) +1.38% half net profit rose 28% to $22.1m due to strong organic growth. Revenue climbed 26% to $150.5m, profit before tax rose 29% to $32m and underlying EBITDA was up 45% to $40.4m.

- Graincorp (GNC) -1.95% said it expected to report full year EBITDA in the range of $385 m to $425m, up from $256m. The company will appoint Graham Bradley as its new chairman to succeed Don Taylor, who is retiring in May.

- Mayne Pharma (MYX) -1.67% EBITDA rose 217% to $129m and underlying EBITDA rose 158% to $108.5m. the company will not be paying an interim dividend. The company is confident it will hit the FY17 revenue and earnings forecast it provided at the time of the Teva acquisition.

- Murray Goulburn (MGC) -5.64% has reported a first-half loss of $31.9m, which compares with a profit of $10m. “The first half of this financial year has been a particularly ‘challenging’ time for MG” according to the new CEO.

- Nextdc (NXT) +12.30% profit rose to $19.3m from $644,000 a year ago, on revenue of $58.7m, up 39%.

- Pepper Group (PEP) -4.85% reported after tax profit for the full year surged to $61.7m from $3.46m a year ago. Total revenue climbed 30% to $684.6m. The company has declared a final dividend of 5.4c.

- RCG Group (RCG) -17.27% net profit rose 31.7% to $21.2m in the December-half, buoyed by the acquisition of rivals Hype DC and the Accent Group. Underlying net profit rose 34% to $23.3m, in line with market forecasts. Not enough apparently.

- Regis Healthcare (REG) -2.59% interim net profit rose 9.4% to $30.932m from $28.279m in the year-earlier period. Regis said it would pay a franked 10.3c dividend.

- Super Retail Group (SUL) +5.34% lived up to its name with net profit rising 66% to $74.4m and revenue rose 6.6% to $1.3bn.

BOND CORNER

ECONOMIC NEWS

- No more rate cuts. Just get on with it seemed to be the message from the new RBA chief Philip Lowe this morning in front of a government committee. Lowe said Australia was also about get the payoff from large increases in production of liquefied natural gas. There were even “green shoots” of recovery in Western Australia. Lowe also said on the dollar that he “would like it to be lower, if I had the choice”.

ASIAN NEWS

- China has appointed financial-sector expert Guo Shuqing as the new head of the nation’s banking regulator. Guo’s appointment comes as the CBRC, together with the central bank, and the securities and insurance regulators, attempt to beat back growing risks from China’s massive shadow-banking sector. The regulators are drawing up new measures to curb the nation’s US$8.7 trillion of asset-management products.

- Remember Bitcon. All time high around US$1186. Bitcoin climbed 125% in 2016, outperforming every other currency, as it did every year since 2010 except 2014.

EUROPE AND US

- The US is rumoured to be looking at a 100-year government debt instrument. The idea has been canvassed by new Treasury secretary Steve Mnuchin to take advantage of super low rates. His team is also considering a short dated 50-year bond. Canada which has a 50-year bond and Ireland and Mexico, both with 100-year bonds.

- Seems that the upcoming (well in 2018) float of part of the Saudi Arabian oil company Aramco is maybe in for a tougher time on a valuation basis. The Saudis hope for around a $2 trillion valuation. As Darryl would say, tell ‘em they’re dreaming”.

- In the UK, the ruling Conservative party has won an historic by-election victory over Labour. The Tories won Copeland, in northwest England, with 44% of the vote. May’s Conservatives won the district for the first time since its creation in 1983.

And finally……………Have a great weekend

A little old man shuffled slowly into an ice cream parlour and pulled himself slowly, painfully, up onto a stool.

After catching his breath, he ordered a banana split.

The waitress asked kindly, ‘Crushed nuts?’

‘No,’ he replied, ‘Arthritis.’

Clarence

XXXXX

Get a Global take on things at http://www.ntmarkets.com