END OF DAY

ASX 200 slips 46 to 5539 as Fed raises and turns hawkish on 2017 rises. Resources feel the wrath as financials outperform. Crown, jobs and Santos $1bn raising dominate markets. Asian markets mixed with Japan up 0.41% and China down 0.52%. AUD bounced to 74.23c and US futures up 42 points.

The script was followed to the letter today with a stronger USD on rate rise fears in 2017 putting pressure on resource stocks, yield plays and REITs. QBE and other insurers looked better on increase rates and outlook. SPI Expiry distorted the volumes.

STOCKS AND SECTORS

- Resources fell in a heap today on a strengthening dollar. BHP -1.82%, RIO -1.43% and Fortescue Metals (FMG) -0.63%. Base metals stocks also sold off with South32 (S32) -3.52%, Independence Group (IGO) -3.11%, and Syrah Resources (SYR) 2.65% as continued takeover stories remain with S32 the most likely interested party. Western Areas (WSA) -6.90%. Lithium stocks too feeling unloved Orocobre (ORE) -5.52% and Galaxy Resources (GXY) -2.91%.

- Energy stocks battered and bruised after the annual Santos capital raising. Almost a Xmas tradition now but $1.5bn sucked most enthusiasm out of the sector. Santos (STO) -10.66% fell below the placement price dragging Woodside (WPL) -2.76%, Oil Search (OSH) -3.12% and Origin Energy (ORG) -3.85% down the rabbit hole.

- Gold another casualty in an end of year party it would rather forget. Newcrest (NCM) -5.18% Evolution Mining (EVN) -3.31% and Perseus Mining (PRU) -4.50%.

- Financials held up well as perceived beneficiaries of higher rates. The Big Bank Basket (BB) closed at $172.20c -0.2% but REITs suffered a big sell off. Westfield (WFD) -2.09% , Vicinity Centres (VCX) -2.03% and Sceptre Group (SCG) -2.47%

- Industrials eased Brambles (BXB) -1.24%, IPH -2.00% and ALS Ltd (ALQ) -1.65%. The IMF sector and Chinese facing stocks fell as Bellamy’s remains in a trading halt. Others in the sector treated as a proxy with A2Milk (A2M) -3.17%, Select Harvest (SHV) -3.75% and Murray Goulburn (MGC) -2.79%

- Healthcare held firm as defensives, Ramsay Healthcare (RHC) +1.19%, and Sigma Pharma (SIP) 2.42% though Estia Health (EHE) -3.24%, Mayne Pharma (MYX) -1.72% and Mesoblast (MSB) -6.00%.

- IT and Telcos soft again with some small pockets of brightness in oversold IT stocks. Aconex (ACX) +1.88%, Nextdc (NXT) +1.82%, Codan (CDA) +6.43% and Netcomm Wireless (NTC) +6.19%. Telstra (TLS) -1.59% slipped as did Vocus (VOC) -3.76% and TPG (TPM) -2.63% despite winning a 4G spectrum auction in Singapore.

- Speculative stock of the day: Sovereign Gold (SOCDA) +33.33% following the recent reconstruction and a solid 102m intercept from surface with high grade, zinc, lead and silver.

CORPORATE NEWS

- Santos (STO) -10.66% tapped into the pre-Xmas spirit with a $1.5bn capital raise with $1bn coming from an institutional placement at 406c and the balance from retail shareholders. The money raised will be used to pay down debt. Which they have a lot of! Given the company raised $3bn in 2015 it is starting to become an annual event.

- Crown Resorts (CWN) has canned its Las Vegas casino project and agreed to sell a portion of its shares in Macau operator Melco Crown back to joint venture partner Lawrence Ho. The sale of 198m Melco Crown shares will raise $1.6bn which will be used to pay down debts and a special distribution and a share buyback. The company still plans to spin off its property assets into a real estate investment trust. The company also updated business conditions

BOND CORNER

- 5-year bonds rose 5bps to yield 2.34%

- 10-year bonds rose 5bps to yield 2.87%

ECONOMIC NEWS

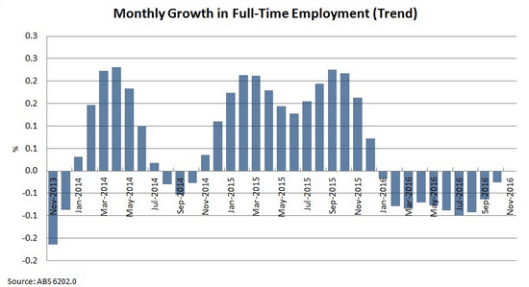

- 39,300 new full-time jobs. Loss of 200 part time jobs.

- The unemployment rate rose to 5.7%.

- Participation rate was higher than expected 64.6%, from 64.4% in October.

- The underemployment rate fell 0.3% over the three months to November.

- The growth in employment is being seen as a good sign for the local economy with the chance of a rate cut diminishing on the number. The AUD dipped slightly on the news before rallying to 74.22c.

ASIAN MARKETS

- South Korea’s central bank held the nation’s benchmark interest rate unchanged at 1.25% as expected.

- China’s yuan at its weakest level against the US dollar in more than eight years, as the USD surged to 14-year high.

- Chinese bond yields are tracking rates upward, with the 10-year yield jumping to a 16-month high of 3.4%.

Rates rising around the world

EUROPE AND US

- Looking at the market reaction across a broad range of currencies to the US rate rise. This year and last.

- Good to see the Greeks back in the news again. We missed them. The country now has a new row with its creditors after the PM has announced spending increases instead of spending cuts and more austerity. Yields on Greek 10 year benchmark government bonds leapt 30 basis points to 7.1% after the announcement. The PM announced a special one-off benefit payment to pensioners earning below €800, in a new spending measure that will cost the Greek Treasury €617m. He also announced a special VAT exemption for Greeks living in the Aegean Isles, and the extension of a free school meals programme for 30,000 pupils.

- Meanwhile in the US, a couple of executives of small drugs manufacturers are set to plead guilty and spill the beans on the whole industry with implications for the current inquiry into price fixing for generic drugs. Mayne Pharma (MYX) may be affected again.

And finally as it’s nearly Xmas.

- Recently sadly leaving us too early was A.A. Gill, who made this observation on Europe as an allegory for the ages of man.

And finally………..

A guy took his blonde girlfriend to her first football game.

They had great seats right behind their team’s bench. After the game, he asked her how she liked the experience.

“Oh, I really liked it,” she replied, “especially the tight pants and all the big muscles, but I just couldn’t understand why they were killing each other over 25 cents.”

Dumbfounded, her date asked, “What do you mean?”

“Well, they flipped a coin, one team got it, and then for the rest of the game, all they kept screaming was, ‘Get the quarterback! Get the quarterback!’ I’m like, hello? It’s only 25 cents!”

Why is Christmas just like your job? You do all the work and the fat guy with the suit gets all the credit.

And a surprise announcement from Amazon

NORTH POLE (API) – Amazon announced an agreement with Santa Claus Industries to acquire Christmas at a press conference held via satellite from Santa’s summer estate somewhere in the southern hemisphere. In the deal, Amazon would gain exclusive rights to Christmas, Reindeer, and other unspecified inventions. In addition, Amazon will gain access to millions of households through the Santa Sleigh. The announcement also included a notice that beginning Dec 20 2016, Christmas and the Reindeer names would be copyrighted by Amazon. This unprecedented move was facilitated by the recently acquired North Pole Court.

Amazon stated its commitment to “all who have made Christmas great,” and vowed to “make licensing of the Christmas and Reindeer names available to all.” It is believed that the guidelines for licensing these names, due before Halloween, will be very strict.

When asked “Why buy Christmas?” Jeff Bezos replied “Amazon has been working on a more efficient delivery mechanism for all of our products for some time, but recognised that the Santa Sleigh has some immediate benefits. We’ll use it first for the next release of the Kindle Fire.”

In a multimedia extravaganza, the attendees were shown a seemingly endless video stream of products that make up the deal. It ended with a green and red version of the Amazon logo, and a new Christmas 2016 trademark, leading into the announcement of the first product from the deal.

Vixen, the new Director of Holidays and Celebrations said, “The first step is to assimilate Christmas within the Amazon Organisation. This will take some time, so don’t expect any changes this year.” He continued, “our big plans are for next year, when we release Christmas 2017. It will be bigger and better than last year.”

He further elaborated that “Amazon users who sign up with Amazon Prime will get sneak previews of Christmas 2017 as early as November first.” Christmas 2017 is scheduled for release in December of 2016, though one unnamed source said that it is dangerously close to the end of the year and may slip into the first half of 2017.

An economist at Goldman Sachs explained that a slip would be catastrophic to next year’s economy and the nation’s tax revenue, possibly requiring the IRS to move the deadline for filing income tax returns to three months after Christmas, whenever that was. “But it could be good in the long term,” he explained. “With Amazon controlling Christmas, we may see it move to May or June, which are much slower months for retailers. This may serve to even out the economy over the year.”

When asked if other holidays are being considered, Mr. Bezos explained that “Christmas is the flagship of holidays, so we wanted to start there. Not all holidays are available for sale, and the remaining will have to show a good long-term business,” suggesting that holidays with a short history may not be in the plans.

Though specific terms of the agreement were withheld, a Santa official confirmed that the deal was “sizeable, even for a man of Santa’s stature.” Some analysts think that Santa has saturated the Holiday market, and is looking for a means to expand his business to year ’round products and services.

Others contend that the Jolly Red Man is looking to retire on the Gold Coast. A spokesperson for the most famous Reindeer could not be reached for comment.

Clarence

XXXXX

No report tomorrow as Clarence will be at a Xmas lunch and does not intend to come back!

Get a Global take on things at http://www.ntmarkets.com