ASX 200 up 65.5 points to 5544 as with one bound we leapt over 5500 on international buying. Banks and miners led the charge with a kicker from WES and WOW together with selected industrials. Asian markets mixed with Japan up 0.69% and China barely changed. AUD 75c and US futures up 10.

For all the naysayers that remind us that we are such a long way from the All-time high on the ASX 200. Here is a chart of the ASX 200 Net Total Return Index. A different story all round. Love those dividends.

STOCKS AND SECTORS

- Resources once again where the alpha lives. BHP +1.20%, RIO +3.12% following some broker upgrades and Fortescue Metals (FMG) +1.67%. Base metals joined the party but were slightly less popular, standing in the kitchen enjoying the vibe. South32 (S32) +1.01%, Independence Group (IGO) +1.16% and Alumina (AWC) +2.31% all unable to hang on to intra-day gains.

- Energy stocks suffered on a falling WTI price despite the restructuring going on with Origin Energy (ORG) -0.62% and Santos (STO) -2.06%. New Hope (NHC) +4.14% rallied strongly on news that coal had been loaded at the QBH Terminal after the storm damage in November.

- Banks and financials continue to power the ASX ahead as we have suggesting for some time. The Big Bank Basket (BBB) +1.25% to $170.70 is hitting with ANZ Bank (ANZ) +2.53% the standout in the sector. Insurers too seeing blue tickets with QBE Insurance (QBE) +4.92% getting a little frothy. Even AMP +3.68% partied like it was 1999 with a solid gain and Macquarie Group (MQG) +1.40% edged ahead.

- Industrials showed good gains especially in mining services Monadelphous (MND) +3.03%, WorleyParsons (WOR) +1.37% and CIMIC Group (CIM) +2.10%.

- Consumer stocks better as expected with Woolworths (WOW) +1.05% and Wesfarmers (WES) +0.97% and Ardent Leisure (AAD) +4.15% recovering from a horror run. Other tourist stocks also seeing good buying Sealink (SLK) +2.53%, Helloworld (HLO) +3.41% and Skydive the Beach (SKB) +9.92%.

- Healthcare continued to be in the summer doldrums given the headwinds from Trump and his latest attack on the biotech drug pricing. CSL -1.08%, Mayne Pharma (MYX) -2.38% and Sirtex (SRX) -1.66%. Local players fared better as Sonic Healthcare (SHL) +2.65%, Ramsay Healthcare (RHC) +0.73% and Fisher and Paykel (FPH) +0.89%.

- IT was mixed with Aconex (ACX) +2.97% up again, can’t last, Hansen Technologies (HSN) +4.10%, Car Sales (CAR) +2.37% and Nextdc (NXT) +2.38%. Telcos modestly better with Telstra (TLS) +0.60%, Vocus +0.74% and TPG (TPM) +1.80%

- Speculative stock of the day: European Lithium (EUR) +27.27% following a research report from respected small cap house EverBlu Research with a price target of 18c. Reading the small print suggests that EverBlu was paid to write the report but that’s the world we live in.

CORPORATE NEWS

- The ACCC will allow News Corp (NWS) to buy APN News and Media (APN) regional publishing business for $36.6m. The sale leaves APN with just radio and out-of-home advertising assets, having demerged its New Zealand business, NZME, earlier this year

- Bellamy’s (BAL) +% says it updated the market the same day it received information on a sales slowdown in China.

- Santos (STO) +% will restructure its business and carve out the non-core assets in a separate business. The restructuring will leave the main company focused on five long-term growth assets, including its LNG projects, its Cooper Basin and Western Australian gas divisions and its prospective Northern Australian business. The non-core company will operate what Santos describes as a “sweat or exit” strategy. The plan is to reduce debt by $2bn by the end of 2019.

- IAG Australia (IAG) +% announced a shake up (must be the time of year) with the company expecting to further outsourcing initiatives and streamlining of IT systems driving cost savings of more than $250 million a year by the end of 2019.

ECONOMIC NEWS

Not quite such a rosy outlook after the GDP yesterday

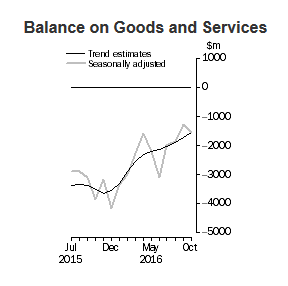

- Australia’s trade balance has actually blown out to $1.54bn in October, from $1.27bn in September.

- Economists had expected a deficit of $610m in October. Exports rose just 1 per cent in a month that was characterised by a leap in commodity prices, while imports rose 2 per cent.

- Goldman Sachs has a positive, or “overweight”, outlook for the Australian sharemarket for the first time in over a decade.

BOND CORNER

- 5-year bonds down 4bps to yield 2.23%

- 10-year bonds down 6bps to yield 2.73%

ASIAN NEWS

- China’s FX reserves fell by $US69.06bn last month, the fifth straight month of declines and more than twice what economist had expected.

Chinese Import/Export numbers

- Exports increased 0.1% while imports rose 6.7% in November

- Shipments destined for U.S. and EU both turned positive

- Japan unexpectedly cut its reading of third-quarter economic growth to an annualized 1.3%, from a preliminary estimate of 2.2% expansion.

- Creative accounting though with the government’s projection for the overall size of the economy rising, thanks to changes in the way gross domestic product is calculated.

EUROPE AND THE US

- UK PM May has made a significant stride towards Article 50 after securing a victory in the House of Commons.

- The board of Monte dei Paschi want more time to cobble together a rescue package. With a history stretching back to Michelangelo di Lodovico Buonarroti Simoni in 1472 a few more months can’t hurt.

- Britain’s oil output dived in October, dragging down overall industrial output to put the economy on a weak footing going into the final quarter of the year. Oil and gas output dropped 10.8%month-on-month, with total production output across the UK falling 1.3%

- Credit Agricole, JPMorgan and HSBC were part of a cartel of seven banks that worked together to manipulate the Euribor interest rate between September 2005 and May 2008, the European Commission said today. JPMorgan has been fined €337.2m, Credit Agricole has been ordered to pay €114.7m, and HSBC has been hit with a €33.6m penalty.

- Following the Italian elections PM Renzi has gone and the President is hopeful that another member of his party can form a government.

- Commodities trader Glencore and Qatar’s sovereign wealth fund are together buying a 19.5% stake in Rosneft, Russia’s largest oil company.

- Not sure what is more worrying the growth of fake news or the fact that people believe this stuff. Even the Pope has joined the growing chorus of disapproval of this new media menace.

And finally……………….Some thoughts….

If quizzes are quizzical, what are tests?

Clarence

XXX

Get a Global take on things at http://www.ntmarkets.com