ASX down 20 points to 5328 after a late bank led rally helped erase early heavier losses. Another mixed day with bond proxy stocks remaining under pressure. Asian markets slightly softer with Japan down 0.08% and China down 0.16%. AUD 75.56c and US futures up 29.

STOCKS AND SECTORS

- Banks clawed back early losses as buyers continue to find reason to be cheerful on the sector. Commonwealth Bank (CBA) +0.33%. Wealth managers also getting a boost from USD strength Henderson Group (HGG) +3.37%, Platinum Asset (PTM) +4.74%, BT Investment (BTT) +2.25% and Perpetual PPT) +1.15%. REITS continue to unwind the 2016 rally on bond proxy selling.

- Insurers slid a little though QBE +0.75% gaining on US Treasury falls. Others fell though, with IAG -1.65%, Suncorp (SUN) -0.99% and Medibank (MPL) +1.2%.

- Iron ore miners saw profit taking as some of the froth is leaving the ore market. Stocks of iron ore at Chinese ports remain close to two-year highs with January ore falling 3% in Singapore. In China the Dalian price was down 4.4%. BHP -1.17%, RIO -0.82% and Fortescue Metals (FMG) -2.56%. South32 (S32) -5.42% fell heavily after its stellar run.

- Gold miners are groping for a bottom as bullion stabilises. Oceanagold Corp (OGC) +8.16%, Newcrest Mining (NCM) +0.53% and Silver Lake (SLR) +2.97%. Base metal stocks playing catch up as analysts throw in the towel with their base metal forecasts and are forced to issue huge upgrades to price targets. Independence Group (IGO) +3.31%, Western Areas (WSA) +3.63% whilst coal stocks are in ‘risk off’ profit taking mode. Whitehaven Coal (WHC) -10.06%, New Hope (NHC) -3.14% and Stanmore (SMR) -8.00%.

- Energy stocks in demand especially Santos (STO) +4.71% as takeover rumours continue to swirl after the Hony Capital purchase of a further 40m shares last week.

- Industrials mixed again as the consumer stocks came in for selling. Wesfarmers (WES) -1.60%, Treasury Wine (TWE) -1.22% and Helloworld (HLO) -4.65%. In consumer stocks Premier Investments (PMV) +5.14% after two broker upgrades.

- Healthcare weaker led by CSL -2.38% with Resmed (RMD) -1.90% and Cochlear (COH) -2.03%. Sigma Pharma (SIP)-2.60% with Virtus Health (VRT) -3.48% a big casualty.

- Bond proxies again in sell off mode, Sydney Airport (SYD) -1.50%, Transurban (TCL) -0.20% and Telstra (TLS) -1.46%.

- Another area of weakness has been the IT sector following big falls in NASDAQ and FANG stocks. Wisetech (WTC) -5.71%, MYOB (MYO) -3.42%, Freelancer (FLN) -5.41% and Nextdc (NXT) -2.56%. IT darling Aconex (ACX) -8.51% announced the retirement of the CFO Steve Recht.

- IPO of the day Dotz Nano (DTZ) +82.50% after raising $6m at 20 cents and announced a $20m research partnership with NTU Singapore.

- Speculative stock of the day: EMU +27.27% after signing a heads of agreement with Prospex SpA and BLC SpA to acquire gold projects in Chile.

CORPORATE NEWS

- OFX -16.98% Results today were very disappointing. Net profit was down 14% to $9.66m for the six months to September. Revenue was just 1% higher at $58.63m. Worryingly transaction size fell 11% to $22,800 which the CEO put down to Brexit. Not convinced. Two more days then a buy perhaps.

- Nine Entertainment (NEC) +2.72% has promised more local content after waring of a short and difficult advertising market to predict. Ratings and softer than expected advertising were the main reasons Nine’s net profit was down 7% last year. The company will also try and cut a further $50 million from operating costs by 2018-19.

- Oz Minerals (OZL) +4.79% after update the mine plan for Prominent Hill. It is a long life asset with underground production of 3.5Mtpa until at least 2028. The underground reserve has grown by 40% due to drill programs, mine planning and cost cutting.

- Steadfast (SDF) -4.21%, Ruralco (RHL)- 0.00% entered into an agreement for SDF to sell its Consolidated Broker business to RHL.

ECONOMIC NEWS

Minutes today from the RBA board meeting in November.

Key points:

- Considerable uncertainty remained about the strength of labour market conditions and the implications for labour cost growth

- The overall assessment was that the risks around the inflation forecast were broadly balanced.

- Members observed that there was uncertainty about the degree of spare capacity in the labour market and how this might ultimately affect inflationary pressures.

- Assessing conditions in the housing market had become more complicated.

- Housing price growth had picked up noticeably in Sydney and Melbourne.

- The transition of activity from the mining sector to the non-mining sector of the economy had continued.’

The yield on Australia’s 10-year government bond spiked to above 2.7% briefly before settling back to 2.64%.

IMF Economists have recommended that the government spend more on growth friendly infrastructure projects and the RBA remains accommodative in monetary policy.

ASIAN NEWS

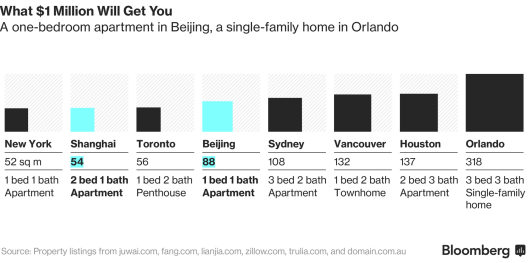

- Seems that the Chinese government moves to block money from leaving the country for property investment are failing. It is estimated the Chinese have bought around $15bn in overseas real estate in the first half of the year.

- Comparative pricing for real estate

- India has taken the extraordinary move to phase out a series of high denomination bank notes in an effort to rein in the black economy, money laundering and tax evasion. With four-hours notice PM Modi declared paper money was gone. Inevitably chaos has ensued and Modi is trying to back track. The PM decreed 1,000 and 500 rupee notes would no longer be valid. Bear in mind that 1,000 rupees is worth $12. 86% of paper money is now useless and has to be exchanged. Indians can exchange 4,000 ($80) of the old rupees every day in cash for new 500 ($10) and 2,000 ($40) rupee notes. Only 1% of Indians pay tax.

EUROPE AND THE US

- US cigarette maker Reynolds American has rejected a buyout offer worth US$47bn from British American Tobacco, according to reports.

- US retailer American Apparel (AA) has filed for its second bankruptcy protection in just over a year.

- Samsung Electronics is buying automotive electronics-maker Harman International Industries for US$8bn as it makes a big push into connected car technologies. It is estimated that the so-called connected technologies market, which goes under the Internet of Things umbrella, will grow to US$100bn by 2025.

- Apparently Steve Bannon (Trump’s right hand man) will call Nigel Farage before Theresa May (UK PM).

- What do you get the Trump kids for Christmas? Top level security clearance it seems.

- And finally in a sign of the times a Patek Philippe watch has sold in Geneva for US$11m. And it is stainless steel made in 1943.

And finally………………

Clarence

XXXXX

Get a Global take on things at http://www.ntmarkets.com