End of Day

ASX up strongly after a long rollercoaster week. The index closed up 42 to 5371 as a match out ‘buy on close’ order doubled the gain at 4pm. Banks and resources led the gains as sector rotation continued and industrials old off. Asian markets up 0.23% and China up 0.45%. AUD 76.16c and US Futures falling 28 points.

‘It was the best of times. It was the worst of times’.

At least if you were in industrials and bond proxy stocks. If you had a resource and banks skew, enjoy. Well a little.

Continuing ‘it was the age of wisdom; it was the age of foolishness’. Sums up this week. We closed last week at 5180 and have risen 3.2%, we are back to where we were on 26th October.

Some serious bubbles developing in commodities which need to unwind. Copper is up 11.7% this week alone. Close to maximum bullishness. Worrying.

STOCKS AND SECTORS

- Resources once again the superstar sector although some of the gloss is coming off and the sector does look overbought short term. BHP +2.13%, RIO +2.44% and Fortescue Metals (FMG) +4.49%. South32 (S32) +5.22% but other base metals were in overbought territory and sellers moved in to square up. Sandfire (SFR) -0.96%, Oz Minerals (OZL) -1.25% and Independence Group (IGO) -0.41%.

- Gold stocks once again sold off as you would expect with Newcrest (NCM) -7.26%, Northern Star (NST) -7.37% and Resolute (RSG) -11.71% some of the biggest losers. Energy stocks mixed with Oil Search (OSH) -1.67% and Paladin Energy (PDN) -11.54% though coal stocks perked back up with Yancoal (YAL) +6.25% and New Hope (NHC) +4.44%.

- Industrials were a waste land of broken dreams today with significant losses across the board. Telstra (TLS) -2.68% was a big casualty as ‘Bondcano’ continues. Utilities were also battered with APA Group (APA) -4.40%, AGL Energy (AGL) -2.14% and Spark Infrastructure (SKI) -3.81%. Infrastructure plays continued to unravel with Sydney Airport (SYD) -1.49% and Transurban (TCL) -3.13%. Other roads stocks fell too Macquarie Atlas (MQA) -2.11%.

- IT stocks also in profit taking mode with Aconex (ACX) -4.53%, iSentia (ISD) -4.00%, MYOB (MYO) -3.81% and Altium (ALU) -3.04%.

- Healthcare and consumer stocks also hit hard. Domino’s Pizza (DMP) -3.28% failed to deliver and Corporate Travel (CTD) -2.84% also suffering.

- Retail slipped Harvey Norman (HVN) -1.47% and Webjet (WEB) -2.17% slipping away. One winner was Austal (ASB) +6.82% on the hope of the 350 new US navy ships to be built in the gospel according to Trump.

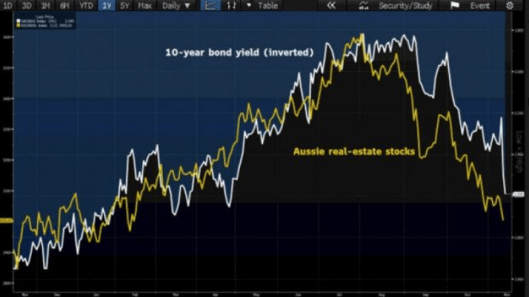

- To the bright spots, financials. Banks improved across the board as US banks charged ahead on Trump reform potential. The big four up around 3% with wealth managers and fundies following in their wake. The big four basket back to $163.80. Clydesdale (CYB) +4.53% was a big winner on a stronger sterling although off highs. REITS an ocean of red with big losses continuing on higher bond yields. Scentre Group (SCG) -1.68% and Mirvac (MGR) -2.23% two of the worst casualties.

- Speculative stock of the day: Activistic (ACU) +96.00% following news it had been selected for the Google Business Partner program. Activistic is a micro-donation platform and the Google program is a no cost one on one guidance for those companies it deems have high growth potential.

- Another big winner today was Silex (SLX) +54.29% after the US Department of Energy and GLE which is the licensee for SLX agreed for the sale of uranium hexafluoride. A big day for long suffering shareholders.

CORPORATE NEWS

- Santos (STO) +6.42% after Hony Capital increased its stake in the energy company with the purchase of another 40m shares at 398c. Hony already has a stake in STO and this brings it to 3.2% after the $159m purchase.

- Private equity firm TPG and its partners have confirmed they have decided to postpone the float of Alinta Energy, which would have been Australia’s biggest this year, to the first quarter of 2017.

- Recently downgraded then upgraded APN Outdoor (APO) -2.59% has a Scandinavian fan as the central bank of Norway, the Norges bank Investment Management announced it now has 5% of the company. Norges manages US$1.4trillion.

- BHP +2.13% has revealed five more cases of Black Lung in Queensland and is now looking at changing work practices and regulation on coal dust.

ECONOMIC NEWS

- Market expectations of another RBA rate cut have fallen to their lowest in months, with Citi seeing a just 4% chance of more easing in December, moving up to a high of 28% in the first half of next year.

- The yield on the benchmark 10–year government bond has jumped another 7bps to 2.57%, its highest since late April. Today’s auction of 12-year bonds raised $1bn at 2.7%. On September 7th a similar bond auction of 11-year bonds was completed at 1.89%.

- This chart helps explain why the REITs have fallen together with infrastructure and other bond proxies.

ASIAN NEWS

- It’s singles day in China. The made up festival is set to break records yet again with Alibaba posting US$1bn of sales in the first five minutes alone. US$5bn in first hour. It took 90 minutes to hit that milestone in 2015, which went on to see sales of US$14.3bn through the day.

- China’s currency is heading for its steepest weekly drop since January. The exchange rate has fallen 0.9% this week to a six-year low as Trump’s unexpected win spurred a seismic shift in fund flows.

- Indonesian rupiah also fell the most in five years with a 2.7% fall to 13,495 to the USD. It seems the fall was exacerbated by short term traders rushing to futures markets to hedge. There is continued speculation that Trump may tear up the TPP and enforce protectionist policies harming the Asian region.

EUROPE AND THE US

Normal service will be resumed in four years

- Remember Trump is going to make America great again. Emerging market sell off has deepened as concerns mount for what it means for them. Whilst the Dow has hot records the MSCI index of Emerging markets has fallen for three straight days. Making US great will not always benefit everyone else.

- Mexico is willing to discuss the North American Free Trade Agreement (NAFTA) with US President-elect Donald Trump, the government said. Canada also is keen to chat. NAFTA has been in place since 1994.

- Traditional investment theory says that as bond yields rise, equities fall. So much for that theory. Same theorists said Hillary would win.

- We have had the Trump Pump. must be time for the Trump Dump. There may well be a Trump Slump. It is just a question of when. May well be tonight.

Leonard Cohen RIP.

And finally………………

Mike Pence walks into the Oval Office and sees Trump whooping and hollering.

“What’s the matter, Mr. President?” The Vice President inquired.

“Nothing at all, I just done finished a jigsaw puzzle in record time!” The President beamed.

“How long did it take you?”

“Well, the box said ‘3 to 5 Years’ but I did it in a month!”

Clarence

XXX

Get a Global take on things at http://www.ntmarkets.com