ASX 200 up 34 points to 5318 in quiet pre Cup trade. Window dressing for end of month helping things along. Banks stage a turn around and materials back in fashion. Asian markets weaker with Japan down 0.20% and China down 0.38%. AUD steady at 76.13c and US futures up 38 points.

STOCKS AND SECTORS

Banks took heart from the ANZ +0.83% deal with big banks gains of around 1%. Insurers and wealth managers missed out as fall-out from the AMP -% update last week continues. Macquarie Group (MQG) -2.40%, QBE Insurance (QBE) -0.99% together with Suncorp (SUN) -0.91%.

REITS firmer with Dexus Property Group (DXS) +2.17%, GPT Group (GPT) +1.30% and Charter Hall Group (CHC) +1.29%.

Consumer stocks slid again with Bellamy’s (BAL) -3.73%, A2 Milk (A2M) -2.78% and Bega Cheese (BGA) -2.18%. Vita Group (VTG) -13.16%, Harvey Norman (HVN) -0.79% and AMA Group (AMA) -1.89%. The switch continues between Woolworths (WOW) -2.39% and Wesfarmers (WES) +1.71% and we saw some bargain hunting in the infrastructure stocks after heavy falls with Sydney Airport (SYD) +2.96%, Transurban (TCL) +1.37% and Macquarie Atlas Road (MQA) +1.51%

IT stocks back in the losers with Aconex (ACX) -5.92%, Car Sales (CAR) -3.53% and Data#3 (DTL) -0.63% whilst telcos did better led by TPG Telecom (TPM) +4.71% and Hutchison (HTA) +7.89%. Healthcare too recovered led by the blue chips Cochlear (COH) +1.56%, CSL +1.20% and Ramsay Health Care (RHC) +2.26%.

Resources a continuing bright spot. Newcrest (NCM) +5.32% after a conviction buy list recommendation, South32 (S32) +1.58%, RIO +0.80% and BHP +0.39%. Energy slightly weaker Oil Search (OSH) -1.91%, Beach Energy (BPT) -3.97% and Paladin Energy (PDN) -6.67%. In coal stocks Stanmore Coal (SMR) +8.21% following a corporate presentation.

Lithium is back in the spotlight with Orocobre (ORE) +20.44% having a very strong day following its quarterly production report. The company posted sales revenue of $33.5m from its lithium facility, up 45% quarter-on-quarter. Galaxy Resources (GXY) +6.06% though Pilbara Minerals (PLS) unchanged.

Speculative stock of the day: Emmerson Resources (ERM) +32.00% after announcing bonanza gold intercepts at Tennant Creek including 8m at 157g/t gold.34.5 g/t silver and 0.5% copper. The current drilling is being funded by the farm-in and JV with Evolution Mining (EVN) +4.15%

CORPORATE NEWS

Qantas (QAN) +4.08% after a trading update showed a 3% decline in revenue due to increased international competition. The company though does still expect an underlying profit before tax of $800-850m. The group also believes that costs will continue to improve from the transformation and fuel hedging policy. A 9% fall at the opening seemed to draw in the shorts looking to cover and the recovery began.

CSR unchanged, Boral (BLD) -0.79% CSR announced that it had acquired Boral 40% interest in the JV for $126.4m. The CSR/BLD JV PGH was formed in May 2015. In the last year to September PGH had revenue of $292m with EBITDA of $53m

Australia and New Zealand Bank (ANZ) +0.83% announced the company had sold its Asian retail and wealth business and will focus purely on the institutional banking space where it is ranked a top four player. The sale price is at a premium to NTA but the company will take a $265m write down on software, goodwill and fixed assets.

Sky TV (SKT) -4.63% after the NZ Commerce Commission has some unresolved issues in respect of the proposed merger between Sky City and Vodafone NZ.

ECONOMIC NEWS

- Private sector credit growth remains tepid, rising just 0.4% in September for an annual rate of 5.4%, coming in below the 10-year average of 6.3% again.

- Business credit grew by just 0.2% in September, after rising by 0.1% in August.

Standard & Poor’s has placed the ratings outlooks of 25 Australian banks, insurers and buildings societies on negative watch as it becomes concerned about rising household debt and property values. Among the largest institutions impacted are AMP Bank, Bank of Queensland, Bendigo and Adelaide Bank, Macquarie whose current ratings were placed on negative outlook.

ASIAN NEWS

- Nippon Yusen Mitsui S.K. Lines and Kawasaki Kisen Kaisha Ltd, Japan’s three largest shipping companies agreed to merge their container operations into one company.

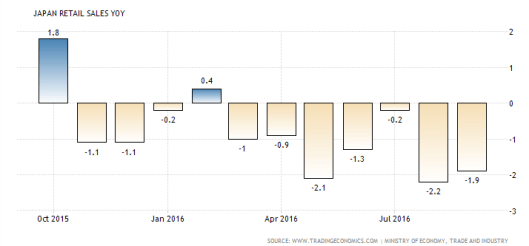

- Retail sales in Japan fell 1.9% year-on-year in September 2016, compared to an upwardly revised 2.2% drop the previous month and worse than market expectations of 1.8% decline. It was the seventh straight month of contraction.

EUROPE AND THE US

- Mark Carney is expected to stay on at the Bank of England extending his term beyond 2018. The governor is expected to make a statement on his future this week.

- The EU and Canada has finally signed the long negotiated free trade agreement known as CETA.

- According to a report from the Leave Means Leave campaign, UK Banks will gain an additional GBP12bn in revenue from leaving the EU. The major boost will be from the removal of Brussels red tape.

- Meanwhile in the US election, one election expert forecaster has the following result.

Click on the map for more details.

d of Day

ASX 200 up 34 points to 5318 in quiet pre Cup trade. Window dressing for end of month helping things along. Banks stage a turn around and materials back in fashion. Asian markets weaker with Japan down 0.20% and China down 0.38%. AUD steady at 76.13c and US futures up 38 points.

STOCKS AND SECTORS

Banks took heart from the ANZ +0.83% deal with big banks gains of around 1%. Insurers and wealth managers missed out as fall-out from the AMP -% update last week continues. Macquarie Group (MQG) -2.40%, QBE Insurance (QBE) -0.99% together with Suncorp (SUN) -0.91%.

REITS firmer with Dexus Property Group (DXS) +2.17%, GPT Group (GPT) +1.30% and Charter Hall Group (CHC) +1.29%.

Consumer stocks slid again with Bellamy’s (BAL) -3.73%, A2 Milk (A2M) -2.78% and Bega Cheese (BGA) -2.18%. Vita Group (VTG) -13.16%, Harvey Norman (HVN) -0.79% and AMA Group (AMA) -1.89%. The switch continues between Woolworths (WOW) -2.39% and Wesfarmers (WES) +1.71% and we saw some bargain hunting in the infrastructure stocks after heavy falls with Sydney Airport (SYD) +2.96%, Transurban (TCL) +1.37% and Macquarie Atlas Road (MQA) +1.51%

IT stocks back in the losers with Aconex (ACX) -5.92%, Car Sales (CAR) -3.53% and Data#3 (DTL) -0.63% whilst telcos did better led by TPG Telecom (TPM) +4.71% and Hutchison (HTA) +7.89%. Healthcare too recovered led by the blue chips Cochlear (COH) +1.56%, CSL +1.20% and Ramsay Health Care (RHC) +2.26%.

Resources a continuing bright spot. Newcrest (NCM) +5.32% after a conviction buy list recommendation, South32 (S32) +1.58%, RIO +0.80% and BHP +0.39%. Energy slightly weaker Oil Search (OSH) -1.91%, Beach Energy (BPT) -3.97% and Paladin Energy (PDN) -6.67%. In coal stocks Stanmore Coal (SMR) +8.21% following a corporate presentation.

Lithium is back in the spotlight with Orocobre (ORE) +20.44% having a very strong day following its quarterly production report. The company posted sales revenue of $33.5m from its lithium facility, up 45% quarter-on-quarter. Galaxy Resources (GXY) +6.06% though Pilbara Minerals (PLS) unchanged.

Speculative stock of the day: Emmerson Resources (ERM) +32.00% after announcing bonanza gold intercepts at Tennant Creek including 8m at 157g/t gold.34.5 g/t silver and 0.5% copper. The current drilling is being funded by the farm-in and JV with Evolution Mining (EVN) +4.15%

CORPORATE NEWS

Qantas (QAN) +4.08% after a trading update showed a 3% decline in revenue due to increased international competition. The company though does still expect an underlying profit before tax of $800-850m. The group also believes that costs will continue to improve from the transformation and fuel hedging policy. A 9% fall at the opening seemed to draw in the shorts looking to cover and the recovery began.

CSR unchanged, Boral (BLD) -0.79% CSR announced that it had acquired Boral 40% interest in the JV for $126.4m. The CSR/BLD JV PGH was formed in May 2015. In the last year to September PGH had revenue of $292m with EBITDA of $53m

Australia and New Zealand Bank (ANZ) +0.83% announced the company had sold its Asian retail and wealth business and will focus purely on the institutional banking space where it is ranked a top four player. The sale price is at a premium to NTA but the company will take a $265m write down on software, goodwill and fixed assets.

Sky TV (SKT) -4.63% after the NZ Commerce Commission has some unresolved issues in respect of the proposed merger between Sky City and Vodafone NZ.

ECONOMIC NEWS

- Private sector credit growth remains tepid, rising just 0.4% in September for an annual rate of 5.4%, coming in below the 10-year average of 6.3% again.

- Business credit grew by just 0.2% in September, after rising by 0.1% in August.

Standard & Poor’s has placed the ratings outlooks of 25 Australian banks, insurers and buildings societies on negative watch as it becomes concerned about rising household debt and property values. Among the largest institutions impacted are AMP Bank, Bank of Queensland, Bendigo and Adelaide Bank, Macquarie whose current ratings were placed on negative outlook.

ASIAN NEWS

- Nippon Yusen Mitsui S.K. Lines and Kawasaki Kisen Kaisha Ltd, Japan’s three largest shipping companies agreed to merge their container operations into one company.

- Retail sales in Japan fell 1.9% year-on-year in September 2016, compared to an upwardly revised 2.2% drop the previous month and worse than market expectations of 1.8% decline. It was the seventh straight month of contraction.

EUROPE AND THE US

- Mark Carney is expected to stay on at the Bank of England extending his term beyond 2018. The governor is expected to make a statement on his future this week.

- The EU and Canada has finally signed the long negotiated free trade agreement known as CETA.

- According to a report from the Leave Means Leave campaign, UK Banks will gain an additional GBP12bn in revenue from leaving the EU. The major boost will be from the removal of Brussels red tape.

- Meanwhile in the US election, one election expert forecaster has the following result.

Click on the map for more details.

And finally…….

A man is trapped on a desert island with a sheep and a dog. After a few months, the sheep starts looking really attractive to the man. However, whenever he approaches the sheep the dog begins to growl in a threatening manner. The man takes the dog to the opposite side of the island giving it some food as a distraction. He runs back to the sheep only to find the dog growling at him. The man ties the dog to a tree with a large leash. He goes back to the sheep only to find the dog growling with a gnawed off leash around its neck. By now, the man is getting depressed and frustrated. As he sits under a palm tree staring out to sea, a beautiful woman in a tight-fitting wet suit emerges from the surf. She asks him who he is and, taking pity upon his lonely state, asks if there’s ANYTHING she could do for him. The man thinks for a moment and then responds: “Could you take the dog for a walk?”

Good luck with the Cup..Clarence is off to the races!!!

Get a Global take on things at http://www.ntmarkets.com