ASX falls another 64 points to 5295.5 on continuing AGM woes. NAB results cheered momentarily before sellers took the upper hand. Asian markets slipped with Japan down 0.44% and China down 0.42%. AUD 76.27c and US futures down 20

STOCKS AND SECTORS

- Another soggy day as losses accelerated across the board. AGMs have become the new battleground. 5300 level holding is crucial. All very Martha and the Vandellas.

- Banks tried to hold up early but succumbed to the selling pressure despite good numbers from National Bank (NAB) +0.47%. Challenger (CGF) +4.29% was one of the few bright spots although a way off its early highs as AGM comments and a new deal to sell its annuity products through the AMP are extremely positive longer term. Bank basket trading at $159.10.

- Bank of Queensland (BOQ) -4.68% ex-dividend today. Commonwealth Bank (CBA) -1.62% announced an advice fee refund program expected to result in customers getting up to $105m in returned fees plus interest.

- Resources weighed with gold stocks suffering another day of substantial losses. Saracen Mining (SAR) -7.66%, Regis Resources (RRL) -5.39% and Newcrest (NCM) -2.60%. One bright spot in the gold miners was much fancied Dacian Gold (DCN) +2.43%.

- BHP -1.44% gave up early gains despite iron ore rising again in Asian trade. RIO -0.13% tried to hold the line and even Fortescue Metals (FMG) -2.73% gave up some of its recent gains. Biggest loser in the sector was Syrah Resources (SYR) -9.16%, together with a reassessment of Lynas (LYC) -9.09% following the debt deal yesterday.

- Profit tasking today in the coal sector with Whitehaven (WHC) -6.15% holding its AGM. New Hope (NHC) -4.51% also gave back some gains with Stanmore (SMR) -4.93% following a quarterly production report.

- Mining services is another sector with some serious unwinding to do with Cardno (CDD) -17.43% copping it after the AGM statements dragging Seven Group (SVW) -4.07% and GR Engineering (GNG) -4.94% in its wake.

- Energy stocks losing ground as the crude price continues to slip. Origin Energy (ORG) -2.93% and Oil Search (OSH) -2.36% two of the worst performers.

- Once again we saw weakness in consumer stocks with Blackmores (BKL) +1.29% setting the tone falling then rallying into the close but continued selling in Wesfarmers (WES) -2.73% as brokers moved to downgrade also weighed. Chinese dairy hopefuls and baby formula stocks were also again on the nose with A2Milk (A2M) -4.17% and Bellamy’s (BAL) -3.86% showing steep losses.

- In industrials SG Fleet (SGF) -7.67% held its AGM with nothing too startling but media reports on the sector as a hole did nothing to make investors feel better. Steep losses too for APN News (APN) -11.59% after the recent placement at 245c to fund the purchase of Adshel.

- Seems a spoonful of sugar can’t help the medicine go down as once again former hot healthcare stocks are falling under the surgeon’s knife CSL -1.75% toying with the $100 level. Monash IVF (MVF) -7.49% and Viralytics (VLA) -5.71% the worst of the sector. Healthscope (HSO) +0.89% seemed to have found a base but Ramsay Health Care (RHC) -2.22% seeing some selling again.

- In tech and telcos, Telstra (TLS) -0.40% slipped below $5.00, Vocus Comms (VOC) -2.81% as tech stocks enjoyed some modest gains. Wisetech (WTC) +0.86%, Aconex (ACX) +1.20%, MYOB (MYO) +0.55% though Codan (CDA) -4.40% fell post the AGM commentary.

- Speculative stock of the day: A blast from the past on good volume, Atlas Iron (AGO) +50.00% as the company answered a price query suggesting the recent run in the share price was the result of the run in the iron ore price., Who would have thought.

CORPORATE NEWS

- National Australia Bank (NAB) +0.47% posted a better than expected profit today at $6.48bn and an unchanged 99c dividend. NIM fell only 2 bps as the cost of funding increased slightly. Bad and Doubtful Debts rose 7% to $800m

- Blackmores (BKL) +1.29% in volatile trading, after confirming weak September quarter earnings at the AGM update today. In the September quarter revenues were down 8.1% at $149m as the net profit dived 46.6% to just $12m.

- JB Hi-Fi (JBH) +0.89% reaffirmed guidance for $4.25bn for 2016-17 with total sales up 12.4% and comparable sales up 8.3% in the first quarter. The company hopes to complete The Good Guys acquisition on November 27th.

- Newcrest (NCM) -2.60% has reported higher gold output in the September quarter, helped by improved production at its Cadia mine in NSW and Gosowong in Indonesia. The gold miner produced 615,498 ounces of gold in the three months to September 30, up 3% from the June quarter. Copper production rose 12% to 23,723 tonnes.

ECONOMIC NEWS

- The ABS today released import/export data showing a solid increase in the terms of trade. Import prices have fallen for the fourth straight quarter by 1% whilst export prices were up 3.5% with solid gains in a range of commodities from coal to sugar and meat.

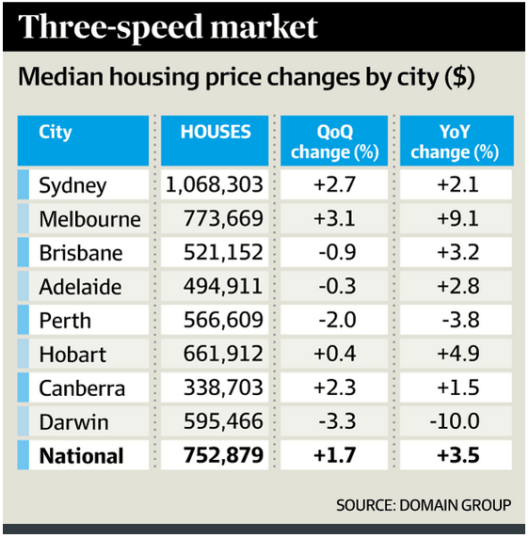

- Sydney and Melbourne house prices have run away yet again, hitting new record highs. Sydney median house price is now at a record $1,068,303, after a 2.7% jump over the September quarter, according to Domain Group data.

- Prices in Melbourne rose the most over the quarter, gaining 3.1% on the quarter and 9.1% from a year ago to a record median price of $773,669.

Why is Canberra so cheap? Cheaper than Hobart.

ASIAN NEWS

- Samsung 3Q profit has dropped 17% after the demise of its exploding not so smart phone. Net income fell to 4.41 trillion won in the September quarter.

- Chinese package delivery company ZTO has raised a huge US$1.4bn in the US in the biggest IPO of the year. So far. The debut gave the company a market value of US$12bn. The money was raised on a valuation of 27 times expected 2017 earnings.

EUROPE AND THE US

- Snapchat now known as Snap, will seek to raise as much as $US4bn in its planned IPO. The IPO would value Snapchat at about $US25bn to $US35bn. The company’s revenue is less than $US1 billion. Much less.

- Deutsche Bank economist Joseph LaVorgna is forecasting the US economy is in danger of slipping into recession as the Federal Reserve’s Labor Market Conditions Indicator has now fallen every month this year except for July. According to the analyst it is only the eighth time in 40 years that the index has been negative and four of those were soon followed by a recession.

- The Bank of England has asked the regulator to assess the exposure of UK banks to German and Italian banks. The BOE has also admitted that lenders are hurt by low interest rates and tough new capital rules.

- In other banking news, if the bank of M&D is closed. That is Mum and Dad Bank and an average Londoner saved 10% of their salary it would take them 389 years to save for a flat in Kensington. That is a lot of smashed avocado. Even in the cheapest part of London it would take 31 years and that is just for the deposit.

- And just to keep things interesting the UK is set to send hundreds more soldiers to the Russian border in its biggest deployment since the cold war.

And finally……………

Clarence on the ABC this morning..think he has nodded off!!!!

Did you hear about the thoughtful Scotsman who was heading out to the pub?

He turned to his wee wife before leaving and said, Maggie – put your hat

and coat on, lassie.

She replied, Awe Jock that’s nice – are you taking me to the pub with you?

Nay, Jock replied, I’m switching the heat off while I’m out.

Clarence

XXXXX