ASX 200 performs better than expected as banks hold their ground with resources in the dog house. The ASX 200 fell a mere 5 points to 5475 in quiet trade again after touching 5433 earlier in the morning. Asian markets slightly weaker with Japan off 0.91% and China down 0.30%. AUD finding its feet at 75.66c and US futures up 20 points

STOCKS AND SECTORS

- Banks saved the day to some extent after a wobbly start with small gains in selective stocks. The big bank basket is currently $162 still grinding higher heading into reporting season. Other financials were mostly weaker with insurers IAG -0.71%, Suncorp (SUN) -1.27 % and OFX Group (OFX) -7.89% in serious trouble, on currency gyrations around the world.

- Resources took their cue from Alcoa results and commodity prices. With BHP -1.51% leading the falls. RIO -0.38% slid too with South32 (S32) -1.58% giving some of yesterday’s stellar gains. Gold stocks were also back in the dog house with Beadell Resources (BDR) -4.76% giving up the gains from yesterday. Alumina (AWC) -3.26% fell in tandem with Alcoa. Falls were taken as an opportunity for some bargain hunting as funds are still underweight the resource sector.

- Energy stocks were in profit taking mode on falls in the oil price. Origin Energy (ORG) -2.42% and Santos (STO) -2.54% in the gas stocks whilst Karoon Gas (KAR) +7.49% is still attracting good support following its moves in Brazil and possible tie up with Woodside (WPL) -0.27%. Coal stocks Whitehaven (WHC) -2.10% but New Hope (NHC) +1.29% and Stanmore Coal (SMR) +18.18% having a truly awesome day following coal contract settlements.

- In industrials, healthcare stocks had a better day led by CSL +1.00% following the AGM buyback announcement, however other large caps failed to catch the vibe with Resmed (RMD) -1.05%, Cochlear (COH) -0.24% and Japara Healthcare (JHC) -2.58%. Estia Health (EHE) -1.85% just keep on falling although the pace has slackened. Viralytics (VLA) +13.13% with Greencross (GXL) +4.43% stirring into life on corporate activity perhaps.

- IT stocks were weak across the board as fears of expensive Pes in former darlings continues. Altium (ALU) -4.02%, Aconex Limited (ACX) -2.62%, Freelancer (FLN) -2.96% and NextDc (NXT) -2.98%. Audio Pixels (AKP) -7.11% one of the sectors biggest casualties.

- Ooh!Media (OML) -2.66% returned from a trading halt following their $65m acquisition of Entertainment Channel and a $60m placement and SPP and only just held its head above the 475c issue price.

- Speculative stock of the day: Mount Ridley Mines (MRD) +40.00% after returning from a trading halt with results from recent diamond drilling with some initial positive results on finding a conductor centred approximately 650m downhole.

CORPORATE NEWS

- CSL +1.00% after the AGM detailed a $500m share buy back as the last $1bn buyback is now nearly complete with 91% done. In some bad news for the company at least management that is the executive pay model received its first strike against the remuneration. Buybacks last year and in previous years have helped boost earnings per share by 26%.

- Slater and Gordon (SGH) -8.33% has been hit with a $250m class action from rival lawyers Maurice Blackburn for wrongdoing including allegedly “blindsiding” them with bad news.. Hardly a surprise given the events of the last year. Ironic really though for a legal company.

- Vocus Communications (VOC) -2.49% following news today that there has been an unsuccessful board room coup with founders of Amcom and Vocus trying to restructure management and James Spenceley and Tony Grist are now gone from the company’s board. Grist had been proposing a “alternative leadership” proposal supported by Spenceley.

- CBA +0.51% has appointed Telstra chairman Catherine Livingstone,as its new chairman.

ECONOMIC NEWS

- The Melbourne Institute and Westpac Bank survey of 1200 people found consumer sentiment rose by 1.1% in October, from September when it edged up 0.3%. Current Conditions components of the Index have been steady while the Expectations components of the Index are up 8.1% on the previous year.

- The survey does indicate that sentiment towards the housing market is waning.

- The government today finalised its 30-year bond offering a 3.24% yield or 101bps above the 10-year yield which was within the expected range. It sold a massive $7.6bn of the bonds with demand around twice that. The issue was supposed to raise around $2bn-$3bn so they were swamped. Triple AAA rated paper yielding 3.25% is pretty attractive.

- Moody’s has predicted that the local economy will be one of the fastest growing triplke A rated commodity exporting economies in 2016. Moody’s expects Australia’s GDP growth to continue to outperformCanada and Norway

ASIAN NEWS

- Nippon Steel & Sumitomo Metal Corp. has agreed to pay the most for metallurgical coal supplies in four years after China’s effort to trim its coal output helped spot prices nearly triple this year.

- Spot hard coking coal climbed to $218.10 a ton in the last few days. A record for the index, which started in January 2013. It averaged about $133 during the third quarter. Contract prices are still below the $330-a-ton record in 2011 after floods curbed supply from Australia, the world’s biggest exporter.

- Samsung continues to fall following the recall of the Note 7 with another 1.75% wiped off the company today.

EUROPE AND THE US

- Putin has called off his trip to Paris as the Syrian crisis continues to worsen.

- More issues in South Africa with Finance minister Pravin Gordhan receiving a summons to appear in court on charges of fraud whilst in charge of the tax collection service a decade ago. Not a good look and the Rand is continuing to feel the heat even more than the Springboks. The South African rand fell more than 3% on the news. President Zuma wants him out it seems in the ever revolving door of the Finance minister.

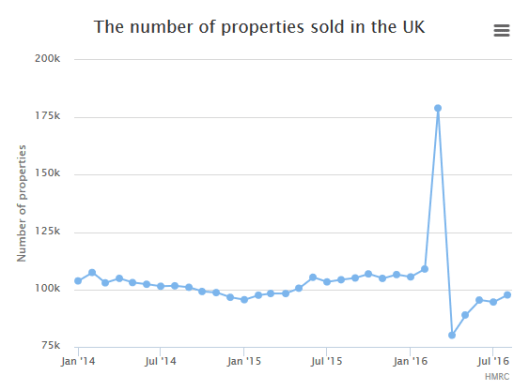

- In the UK the buy to let market, much like our investor housing market is recovering after heavy falls in April. Online property portal Rightmove reported that inquiries for buy-to-let properties had jumped 30pc since May. April brought a sharp increase in stamp duty on second homes and the buy to let market.

- Chinese property hunters are piling into the UK, looking for investment opportunities due to the weak sterling. Juwai, a Chinese listings website, said that buyer inquiries on British property climbed by 12.2% in September alone. This is 90% higher than the same month last year.

- Soft commodities are enjoying some good gains this year with The Food and Agriculture Organisation’s (FAO) food price index prices increasing by 10% year on year and 2.9% on August due to the rising cost of sugar.

- Federal Reserve Bank of San Francisco economist John Fernald has taken a stab at projecting the future normal rate of growth given long-term trends in the economy. He forecast the US economy will now grow at 1.5%-1.75% a major slowdown since the heady days of the 90s if he is right.

And finally…..

| Two IRISHMEN were looking at a Mail order catalogue and admiring the models. One said to the other, The second one replies, The first one says, with wide eyes, The second one smiles and pats him Three weeks later, the youngest IRISHMAN asks his pal, The second IRISHMAN replies…… |

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com