Not too shabby!!

ASX 200 closed firmer at 5539 up 4 points after a late rally in banks and financials. Woolworths led the market down early with broad based losses across the board. Healthcare and consumer staples underwhelm ahad of CPI. Asian markets mixed as Japan falls 1.58% and China up 0.43%. AUD at 75.28c and US futures up 24.

STOCKS AND SECTORS

- Consumer stocks reversed all engines today as the jury came back with the verdict in Woolworths (WOW) -3.29%. Analyst enthusiasm was tempered significantly as the road is long and there is many a winding road to complete the restructure. Easy to restructure a balance sheet not so easy to restructure a business. Other consumer stocks slipped in sympathy with Metcash (MTS) -1.4% and Mantra Group (MTR) -3.47% and Flight Centre (FLT) -0.86%.

- Healthcare stocks were particularly weak led by CSL -1.15% and Resmed (RMD) -1.93%. Aged care Japara Healthcare (JHC) -2.64% and Regis Healthcare (REG) -3.15%.

- Banks wore modest losses with the big four basket at $161 slightly higher from yesterday. Insurers narrowly mixed with Suncorp (SUN) +1.76%, AMP -0.85% and QBE Insurance (QBE) +0.45%.

- Resource stocks weaker led again by gold stocks with St Barbara (SBM) -4.92%, Newcrest (NCM) -2.31% and Ramelius Resources (RMS) -7.76%. Base metals fell

- Big miners were better at the close with BHP +0.1% and RIO -1.12%. Base metals fell again slightly with Independence Group (IGO) -1.69% and Orocobre (ORE) -2.25%. Magnis Resources (MNS) +6.76% bounced back hard with Fortescue Metals (FMG) +1.73%.

- Speculative stock of the day: Dark Horse Resources (DHR) +140.00% after announcing the acquisition of a significant Argentinian lithium portfolio.

CORPORATE NEWS

- SAI Global (SAI) -0.79% says rapid global consolidation of the quality assurance sector has prompted its decision to start a formal process to sell its own quality assurance business which may fetch up to $400 million.

- Smartgroup Holdings (SIQ) +12.98% following news the placement was heavily oversubscribed at a 6.9% premium to raise $54m at 700c to buy Selectus.

- BWX Ltd (BWX) +4.82% Has announced that Boots UK will begin carrying BWX’s Sukin range. Sukin products will also be available for order and on its online stores.

- Monadelphous (MND) +3.78% on news the company was diversifying into renewable energy.

- Perseus Mining (PRU) -0.88% on quarterly numbers showing cash position of $166m. No third party debt. Gold forward contracts for 216,900 oz at an average price of $1272oz and an

- Northern Star (NST) unchanged after reporting a 65% increase in net profit to $151.4m. Final dividend up 33% to 4c and ROE hits 39%. All-in sustaining cost of A$1,041/oz, down from A$1,065/oz in FY15. Cash and equivalents of $326m up $178m.

- ALS (ALQ) -2.3% following a statement from the chairman and a profit update. First half underlying after tax profit to be in the range of $50 to $55m, compared with $61.9m in the first half last year. Declines in oil and gas operations continue with environmental, food, pharma and geo all growing well.

ECONOMIC NEWS

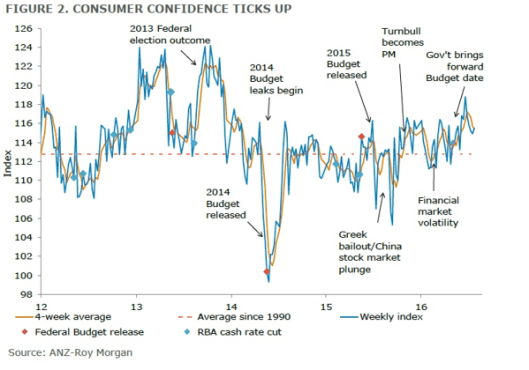

- ANZ-Roy Morgan Consumer Confidence rose 0.5% to 115.5

ASIAN NEWS

- The Japanese stimulus plan appears to be taking shape with more new measures being submitted to the ruling LDP. The media reported on Tuesday that the plan would include 6 trillion yen (US$57 billion) of new spending. The cabinet will make the final decision on the stimulus on August 2. The document says the government hopes the central bank will achieve its 2% inflation target with the package likely to win approval in October and the money to flow in 2017.

- Japan will not meet its goal of reaching nominal gross domestic product of 600 trillion yen (US$5.7 trillion) in fiscal 2020, and may not achieve it even by fiscal 2024 if growth stays sluggish, the government’s projections showed today.

- Casino operators jump in Hong Kong on earnings optimism – Sands China jumped 7.1% in Hong Kong as JPMorgan said the casino operator’s second-quarter results were better than the bank had expected.

- Pokémon maker Nintendo followed up the huge loss yesterday with another drop early before buyers emerged to see it up 1.2% today ahead of its results later this week. Nintendo was still valued at 109 times projected net income after Monday’s plunge, or more than 6 times the average for the Nikkei 225 Index.

EUROPE AND THE US

Modest positive opening for European markets

- Amazon to test drones in UK suburbs and rural areas – Flexible regulations mean a breakthrough for ecommerce company.

- Michelin, Europe’s biggest tyre maker, announced first-half operating profit rose 11% as gains from a cost-cutting plan kicked in and car sales growth accelerated in China. Operating profit before one-time gains or costs increased to 1.41 billion euros (US$1.55 billion) from 1.26 billion euros a year earlier, the company announced Tuesday morning and confirmed forecasts for higher earnings.

- The Confederation of British Industry (CBI) said optimism about business prospects dropped to levels not seen since January 2009 in the three months to July. The CBI’s survey showed just 5% of manufacturers were more optimistic about business environment than three months ago, compared with 52% that were less optimistic. The balance of -47% was well below expectations of a shallower drop to -15%.

And finally………..

On the first day of training for parachute jumping, a blonde listened intently to the instructor. He told them to start preparing for landing when they are at 300 feet. The blonde asked, “How am I supposed to know when I’m at 300 feet?” “That’s a good question. When you get to 300 feet, you can recognize the faces of people on the ground.” After pondering his answer, she asked, “What happens if there’s no one there I know?”

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com