ASX 200 rises, falls and rises again for an 18-point gain on the day to 5274. Banks lead the way with materials and energy the laggards. Asian markets positive with Japan up 1.4%, China up 0.24% and HK up 0.65%. AUD slightly stronger at 74.75 and US futures up 54 points.

A slow burn today as we moved closer towards 5300 before the 11.30am release from the RBA on their minutes. The initial reaction seemed slightly positive with the ASX 200 topping out at 5290 before some nerves came back and we gave up all the 30 points of gains and slipped negative before a slow creep back up closing at 5270 up 13 points.

Yesterday move was explosive to the upside and we needed to consolidate and reassess.

Stocks and Sector Highlights:

- Financials the most positive today with the big four up around 1-1.6% except for National Bank (NAB)-0.3%. Macquarie Group (MQG)+1.4%.

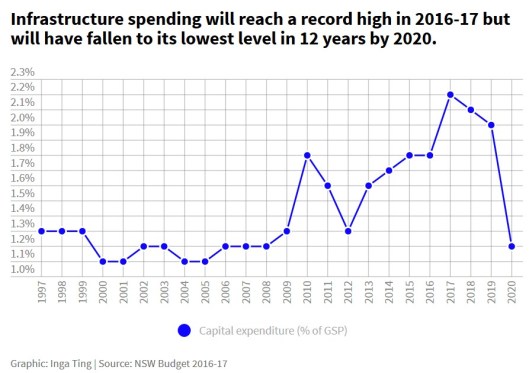

- Infrastructure stocks were in demand following the NSW Budget and increase infrastructure spending. Sydney Airport (SYD)+2.1%% and Transurban (TCL)+1.4%. Healthcare stocks also better, Resmed (RMD)+2.6% and Regis Healthcare (REG)+6.3%.

- Energy and materials were clouded today with Woodside (WPL)-3.5% the biggest loser.

- Lithium stocks continued higher led by Orocobre (ORE)+2.7%, Lithium Australian (LIT)+4% and Mineral Resources (MIN)+3.2%

- Speculative stock of the Day: Rectifier Technologies (RFT)+256% following an announcement on its single phase switched mode rectifier to deliver power for the electric vehicle market.

Corporate News

- BHP -0.9% the company will cut its coal costs by $US600 million by the middle of 2017 and could sell more parts of its coal portfolio. the company had delivered $US3bn of “productivity gains” since 2012. They hope to cut cash costs across its coal arm by a further 16% by the end of June 30, 2017, despite having cut costs by 25% since the end of the 2012 financial year.

- CEO Andrew McKenzie is also in NY spruiking BHP and believes iron ore prices now ‘more realistic’ on basis of fundamentals. “One of the markets that will take longest to come back into balance is the iron ore market.”

- APN News and Media (APNDA)-3.1% APN News & Media has sold its regional newspaper business to its own shareholder, News Corp, for $36.6 million. The regional assets include 12 daily newspapers, 60 community newspapers and dozens of news websites. News Corp already owns a 14.9 per cent stake in APN.

- Fortescue Metals (FMG)-3% appoints Stephen Pearce top the board. Pearce was the CFO since March 2010.

- New Hope Group NHC) -2.7% after the Queensland Competition Authority has refused Queensland’s rail draft access undertaking. This will mean lower access charges until 2012 and will also result in an adjustment for the period between July 2013 and the new period.

- Resolute Gold (RSG) +5.7% to recommence open pit mining at Ravenswood.

- Pilbara Mining (PLS) +% on track for July resource upgrades drilling success continues at the Pilgangoora Lithium-Tantalum project in WA.

- ResApp (RAP)+16.2% after announcing positive clinical trials of their respiratory smart phone app to diagnose chronic obstructive pulmonary disease or COPD.

- Ensogogo (E88) suspended as the CEO and founder has jumped ship from this mobile shopping market place and has joined Commonwealth Bank (CBA) +%. Not a great sign for this tech start up.

- AGL +0.2% will offer customers an All-you-can-charge package for electric car charging at $1 a day or $365pa. The company will also supply a dedicated car charger or a smart meter.

- Bega Cheese (BGA)+1.8% announced their 2016/2017 farmgate milk price of $5.00kg of milk solids. They maintained the 2015/16 price of $5.60kg milk solids.

Economic News

RBA Monthly board minutes:

The RBA noted the continued absence of broader inflationary pressures.

- “Short-term measures of inflation expectations – from consumers, market economists, union officials and inflation swaps – had remained below average.”

- “The latest suite of data had confirmed that labour cost pressures remained subdued in the March quarter, a few of the wage measures were slightly more positive.”

- “Inflation was expected to remain low for some time.”

It seems that the crucial number the RBA is looking at will be the CPI number at the end of July. The currency responded positively pushing ahead to 74.75 cents.

- Bureau of Statistics’ index of dwelling values across the eight capital cities fell 0.2%in the three months to March from the December quarter, when it plateaued. It was the first decline since the September quarter of 2012, when the index also fell 0.2%.

NSW Budget today showed a budget surplus of over $8bn over the next four years.

- The NSW Treasurer said the budget surplus would be $3.4bn this financial year, before growing to $3.7bn in 2016-17, $1.3bn in 2017-18, $1.4bn in 2018-19, and $1.6bn in 2019-20.

- Stamp duty receipts are forecast to rise from $8.9bn this financial year to $9.8bn in 2019-20.

- State funded investment in infrastructure will average $12.1bn a year over the next four years.

- Another $1bn will be spent on new suburban trains for Sydney.

In Asia

- Walmart is buying a 5% stake in China’s JD.com. This looks like a do-over deal for Walmart which has been struggling in China. As part of the deal JD.com will take ownership of Wal-Mart’s Yihaodian online marketplace. The Chinese branch of Sam’s Club also will open a store on JD.com, and the two companies will link up their supply chains. A 5 percent stake in JD.com would be worth about $1.5bn at its current stock price.

- Finance Minister Taro Aso signalled that Japan’s government won’t intervene to stem the yen’s strength without due consideration. The Brexit vote and its effect on the global economy has boosted the yen’s demand as a safe-haven currency.

Europe and US

Big night in Germany as the lands highest court is set to hand down its most important judgement on the legality of the Super Mario ‘whatever it takes’ Outright Monetary Transactions program. Although it has never been needed, the threat has been enough it seems, this is the last resort crisis tool for the ECB to avert a sovereign debt crisis.

Still close on the polls though

And finally………………

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com