ASX 200 finishes the week on a high in thin trading up 16.3 points at 5166.4. Banks reverse early weakness and resources pare losses. Asian markets tread water as Chinese data and the Fed next week give reasons to do nothing. AUD pushed 75 cents and US Futures up 106.

A very quiet day to finish a solid week. Up from 5090 to 5175 (1.6%) in a week. Volumes were anaemic compared to the big numbers we saw earlier and the market is waiting for the Fed next week. Once again the banks were the swing factor and after opening and slipping to be down 30 points at 5118, we rallied back as Asia came online. The rally continued into the afternoon as sellers backed off and buyers squared up positions ahead of the long weekend. (Victoria that is).

There is no doubt that long term the latest ECB bazooka is supportive of the euro economy and equity markets. But as usual traders seemed unable to look beyond the headlines and were left underwhelmed. Maybe as more rational analysis is brought to bear we will see some positivity return.

Some shuffling of the decks today as Index changes helped some and hindered others. Changes to ASX 200 will take place after trading finishes on 18th March.

In: Aconex (ACX), Bellamy’s (BAL) Brickworks (BKW), IPH and St Barbara (SBM).

Out: AWE, Cabcharge (CAB), Karoon Gas (KAR), Slater and Gordon (SGH) and Ten Network.

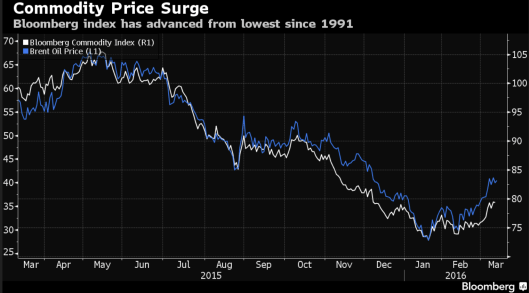

The question is has the commodity cycle bottomed? Well has it? ANZ has said so in a research note today. Who are we to argue?

Stocks and Sectors

- Resources remained weak but well off their lows. BHP-0.51%, RIO-0.36% and Fortescue Metals(FMG)-2.21%. Base metal stocks slid with Western Areas (WSA)-3.97%, Oz Minerals (OZL)-0.95%Sandfire Resources (SFR)-2.75% and Syrah Resources (SYR)-2.1%.

- Energy stocks eased too but again off their lows. Oil Search (OSH)-1.91%, Woodside Petroleum (WPL)-0.3% and Worley Parsons (WOR)-5.81%.

- Gold stocks were the winners from overnight volatility as bullion prices increased Newcrest (NCM)+3.31%, Northern Star(NST)+3.94% and Evolution Mining (EVN)+4.98%, St Barbara (SBM)+5.45% was also in high demand following a quarterly review.

- Financials were better after early losses. Australia and New Zealand Bank (ANZ)+0.27% after reversing early losses. Westpac Bank (WBC)+0.68%, Commonwealth Bank (CBA)+0.3% with Macquarie Group (MQG)+2% also doing well. Other insurers and wealth managers also picked up gains Suncorp Group (SUN)+0.59%Platinum Asset Management(PTM)+3.11% and Henderson Group (HGG)+2.56%.

- Industrials mostly green on screens except for mining services Cimic Group (CIM)-3.84%, Monadelphous Group (MND)-2.24% and Cardno (CDD)-2.14%.IT sector was better with iSentia (ISD)+4.2%, MYOB (MYO)+3.64%, Aconex Limited (ACX)+3.77% and Computershare (CPU)+1.06%.

- Surfstitch (SRF)+6.46% continued their rise after the extraordinary moves from the CEO yesterday. Gaming stocks were better too with 3P Learning (3PL) +9.56% leading the education sector. And Navitas (NVT)+0.83%.

- Healthcare stocks squared up after losses yesterday. CSL +0.42%, Resmed (RMD)+2.08% and Primary Healthcare (PRY)+1.63%.

- Speculative Stock of the Day: 88Energy (88E) +10.45% following a response to an ASX speeding ticket regarding their icewine#1 drilling evaluation.

Corporate News

- Macquarie Bank (MQG)+2% has found itself in trouble with ASIC again after the bank was found to have mishandled client money over a 10-year period. They have imposed conditions on Macquarie’s financial services licence over the breaches including failing to deposit monies into a designated client trust account and for making withdrawals that were not permitted from such an account.

- Looks like BHP—0.51%% and Vale are expecting to start production at the troubled Samarco project in Brazil. Iron ore pellet production for the initial two to three years would likely be at a reduced 19 million tonnes per year compared to the 30 million tonnes it was producing before the tragedy.

- Former MD of Hanlong Mining, Steven Xiao, has been sentenced to over 8 years in jail for insider trading. This is the longest ever sentence in Australian history. The prosecution relates to 100 illegal trades in Sundance and Bannerman in 2011

Economic News

- Nothing to report here today.

In Asia

- China has raised its yuan fix by the most this year. The latest fix at 6.4905. Helping the AUD back up to 74.9 cents

Just another new kid in town.

- Seems there is a new index to track. No longer the Baltic Dry for the index of bulk shipping rates but now the Maritime Silk Road Freight Index which was launched last July.

- The latest read is 65.11 which is 10% lower than the previous month.

- The Baltic Dry index is down from $1222 in August to $384. Seems interesting that the Baltic Dry index peaked last year just before the Chinese authorities moved to devalue the yuan. Coincidence? Maybe.

- Plenty to come this weekend from China with a briefing by PBoC Governor Zhou on financial reform and development. We will also get briefings from financial watchdogs China Insurance Regulatory Commission, China Banking Regulatory Commission and the China Securities Regulatory Commission.

- We also see retail sales. Industrial production and fixed asset investment.

Europe and the US

The key measures announced last night by Super Mario.

- Cut its main deposit rate to -0.4% from -0.3%

- Cut its main refinancing rate to 0% from 0.05%

- Increased the volume of monthly asset purchases to €80 billion from €60 billion.

- Expanded the asset purchase program to include investment-grade corporate bonds

- Announced four more ‘targeted long-term refinancing operations’ paving the way for banks to borrow from the ECB at negative rates in certain cases

- Draghi said banks that lend more to companies and households will be given a discount.

- Promised to keep interest rates at or below the current level until “well after” March 2017.

An interesting graphical representation from the heart of the US Shale boom in Oklahoma.

The red dots are foreclosures

Something to think about when you are at those property opens this weekend.

Clarence

XXX

Get a Global take on things at http://www.ntmarkets.com