Tags

ASX200, Australian Sharemarket, Ben Bernanke, Charlie aitken, diggers and dealers, essex Lion, Fortescue mining, gold, insurance, iron ore, Mario Draghi, Whitehaven Tinkler coal bid cash

ASX 200 down just 0.8 of a point to 4975.4 after a resource rally turns around early steep losses. Banks and Financials continue to be unloved. Asian markets mostly closed today as China takes a week’s holiday. Japan though open and slips 0.8% with US futures up 52 points. AUD remains at 70.89 cents.

Like Alien v Predator, it appears to be a similar story with Resources v Banks. After a steep fall at the open, the resource stocks found their footing and actually pushed us back into positive territory, albeit briefly, before easing back for an almost unchanged close. We touched a low of 4925 early before bargain hunting took us back to 4975.4. There is no doubt that the switch out of banks and into resources is continuing given the very oversold nature of resource stocks.

- Profit results were a little under-whelming. JBH brought some good news but the market needed more and the shock of Western Union walking away from the OzForex (OFX) -42.07% deal was a worry as financials continued to be somewhat friendless. Commonwealth Bank numbers on Wednesday will be crucial.

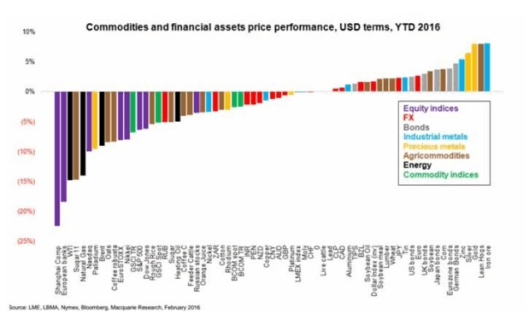

- Iron ore has been the surprise winner this year as China stocks up pre the New Year period. The metal has rallied around 15% since its mid-January low. Temporary supply disruptions from local producers and Brazil are helping the bulls.

The best and the brightest assets this year.

STOCKS AND SECTORS

- Resources especially gold stocks were the big winners today with gold miners continuing to perform and dragging the bulk commodities and base metal stocks higher. In the gold space Evolution Mining (EVN) +6.52%, Newcrest (NCM) +3.74% Regis Resources (RRL) +3.7% and OceanaGold Corp (OGC) +5.15%. Iron ore stocks rose, BHP +1.05% and RIO +2.19% but Fortescue Mining (FMG) -3.43% was unable to shake off the blues. South 32 (S32) +3.49% continued to bounce followed by Independence Group (IGO) +4.53%, Iluka Resources(ILU) +1.91% and Oz Minerals (OZL) +2.38%.

- Energy stocks were mixed with Woodside (WPL) +0.59% slightly better although Origin Energy (ORG) -1.0% and Oil Search (OSH) -0.72%.

- In financials, banks continue to show weakness Australia and New Zealand Bank (ANZ) -1.49% the worst of the bunch but wealth managers again slid, Platinum Asset (PTM) -2.96%, BT Investment Management (BTT) -2.01% and Magellan Financial (MFG) -1.64%. Insurers were mixed with QBE Insurance (QBE) -1.53% and Insurance Group Australia (IAG) +0.94%.

- The IT Sector was a solid red shade today MYOB (MYO) -2.65%, Freelancer (FLN) -4.62% Aconex (ACX) -3.26% and iSentia (ISD) -4.03%.

- In the industrials, gaming stocks eased Aristocrat (ALL) -0.3%, Tabcorp (TAH) -0.7% and Crown Resorts (CWN) -0.17%. Healthcare stocks were weaker too following Capitol Health (CAJ) -20.51% after a market update. Australian Pharma (API) -2.82%, Sirtex (SRX) -0.81% and Fisher and Paykel (FPH) -1.11%. While healthcare is sometimes considered immune (no pun intended) to market volatility and a defensive sector, government cuts and uncertainty can seriously affect revenue. That is why the best ones diversify their income geographically.

- Mining services again weaker Seven Group Holdings (SVW) -1.56%, Reece (REH) -2.17%, Royal Wolf (RWH) -6.67% and Programmed Maintenance (PRG) -8.93%. Aurizon (AZJ) +5.1% enjoyed a very positive day today possibly on the back of the Asciano deal.

- Speculative stock of the day: Raya Group (RYG) +52% has signed a MOU with a leading chipset manufacturer to secure access to XPED patented ADRC technology.

CORPORATE NEWS

- Ansell (ANN) +7.31% reported a 21.6% fall in first half net profits. The CEO is predicting a better second half and will pay a 20c dividend. The news was no real surprise given the market update the CEO gave last week and the market seems to be taking the actual news much better than the guidance last week.

- JB HiFi (JBH) -0.54% upgraded its guidance for the year to $143-$147m after delivering a 7.5% profit increase to $95.2m. Total sales rose 7.7% to $2.12nm on strong sales of mobile phones, IT and fitness products. The stock is one of the year’s best performers and is up around 13% for the year despite large short positions in the stock.

- OzForex (OFX) -42.07% shocked the market this morning with not only Western Union walking away from its bid for the company but also a profit downgrade of around 8.6-9%. The company is puzzled by the response from Western Union but given the downgrade it seems that the due diligence process revealed some issues with the underlying business.

- Asciano (AIO) +2.36% has declared Qube (QUB) its prferred bidder after the Qube team increased their offer to 704c in cash and one QUB for every AIO. The rival Brookfield consortium will now have 5 days to respond to it. The ACCC though has yet to clear the deal by either party and is not expected to report back until the end of March. Assuming it does not delay the response yet again.

- Broadspectrum (BRS) +3.72% after announcing its contract for Manus Island and Nauru was being extending for another 12 months and upgrading guidance for EBITDA to the range of $280-300m. The company is still advising shareholders to reject the current takeover bid from Ferrovial at 135 cents. The independent expert’s valuation is between 160-185 cents.

- Capitol Health (CAJ) -20.51% showed the full extent of its problems today after reporting a 52% drop in underlying profit to $2.2m as patients are deferring expensive x-rays, ultrasounds and CT scans in Victoria. Government reviews on healthcare spending will only increase as the budget looms.

ECONOMIC NEWS

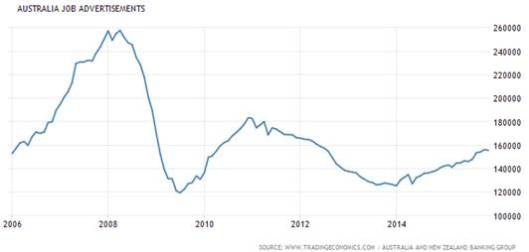

Internet jobs ads rose 1% compared to December and 10.8% compared to a year ago.

In housing, residential rentals are growing at their slowest pace in two years according to CoreLogic RP data. Growth of 0.2% across the capital cities in January but no growth at all over the last year. Over the past 12 months, only Melbourne (2.1%), Canberra (1.8%) and Sydney (1.4%) recording modest rental growth.

In Asia

Chinese markets closed for New Year celebrations. Also closed Hong Kong, Indonesia, Malaysia, New Zealand, Philippines, Singapore, South Korea and Taiwan.

The Japanese have posted the 18th consecutive current account surplus, as cheap oil helps the economy. The excess on trade was 960 bn yen against last year’s 225.9 bn yen, slightly weaker than economists had been expecting. Economists expect the economy to have contracted an annualised 0.8 % in the December quarter when GDP is released next Monday.

The Bank of Japan is investigating claims that the news of the negative interest rate move was leaked a few minutes before the official announcement.

Europe and US

Looks like HSBC will be staying put in London with the final decision imminent.

And finally not only will we be watching CBA this week but Janet Yellen steps in front of the House Financial Services Committee. She will address the Senate Banking Committee the following day. Should prove a tricky act to balance fears with confidence.

Ahead in Europe

- FTSE +36.50 point.

- DAX -127.50 points.

- CAC -27.50 point.

MARKET STATS

- Volume was $4.82bn (Daily average $4.656bn FYTD)

- Dow Jones Futures up 52 points.

- Dow Jones was down 211 overnight.

Clarence

XXXXX

Get a Global take on things at http://www.ntmarkets.com