Tags

asx, ASX200, Australian Sharemarket, Ben Bernanke, BHP, cba, Charlie aitken, china, commonwealth bank, crash, diggers and dealers, fairfax, Fortescue, Fortescue mining, glenn stevens, gold, iron ore, marcus padley, Mario Draghi, RBA, Whitehaven Tinkler coal bid cash

Glenn Stevens? The Rally Killer!

ASX 200 falls 50.3 points to 4993.3 as the RBA stays its hand but leaves the door open for the doves. Media shares take prospect of an early election badly. Asian markets weaker, China up 2.3% in thin trading and Japan down 0.54%. US futures down 95. AUD drops to 70.65 cents.

The market looked a little lost today as it slipped away even before the RBA announcement at 2.30pm. Resources back in the spotlight as energy shares fell on crude losses. Once again the board has kept rates unchanged at 2%. The accompanying statement seemed a little less relaxed than the Christmas missive from Glenn about global gyrations, although they did leave the door slightly ajar for cuts if things were to deteriorate further. Broad losses though across most sectors, punctuated by individual results and announcements. The market slipped post the unchanged rate decision, back through the 5000 level to close at 4982 near its low, as an easing bias seemed to spook the market. It does not take much at the moment to spook the cattle.

STOCKS AND SECTORS

- Resources were once again on the nose, led by BHP -2.16%, RIO –3.67% and Fortescue Metals (FMG) -5.07%. Base metals were also weak, Syrah Resources (SYR) -2.84%, Independence Group (IGO) -5.56%, OZ Minerals (OZL) -0.78% and Iluka (ILU) -0.72%.

- Energy stocks weak after crude falls. Woodside Petroleum (WPL) -3.26%, Oil Search (OSH) -2.75% with Origin Energy (ORG) -4.75% one of the worst. Santos (STO) -4.26% continues to attract media speculation on plans to sell off some of its PNG assets. Liquefied Natural Gas (LNG) +4.03% managed to buck the trade today, drawing strength from recent deals in US gas.

- Industrials were sold off across the board with media particularly hard hit as speculation mounts that an early election is a distinct possibility and media reforms will be put on hold. Nine Network (NEC) -6.17%, Seven West (SWM) -5.29% and TEN (seriously) -7.5%. Information technology was one of the few patches of green today with Computershare (CPU) +2.84% and Altium (ALU) +12.17% both announcing positive deals.

- Banks held up better than most as National Bank (NAB) +0.29% prepares to begin life without a UK drag in management time and earnings. Wealth managers were once again sold down aggressively, led by Magellan Financial (MFG) -5.31% and Challenger Financial (CGF) -6.46%. Insurers tried valiantly to buck the negativity focusing on premium growth in the sector, QBE +0.18%, Insurance Group Australia (IAG) +0.19% and NIB Holdings (NHF) +1.42%

- Healthcare could not avoid the falls with Greencross (GXL) -4.15% and ImpediMed (IPD) -4.29% together with Sirtex (SRX) -3.51% the lowlights.

- Speculative stock of the day: Top End Minerals (TND) +84.62% after it announced plans to acquire an Israeli facial recognition security company for $6m and look to raise $3m in working capital to expand the business.

COMPANY NEWS

- Navitas (NVT) +3.91% after profits rose 44% to $45.1m in the 1H from $31.5m in the pcp, which included a $9m goodwill impairment. Revenue climbed 8% to $518.7m. NVT said it was buying back up to 7.5% of shares using funds from undrawn debt facilities. The buyback is scheduled to begin on February 16.

- Fletcher Building (FBU) +3.59% announced it will buy Higgins road construction company in NZ for NZ$315m.

- BHP -2.16% as S&P cut its credit rating to A from A+ and said further cuts were possible. This will send a shudder through the board and the progressive dividend policy looks as dead as the Norwegian Blue. S&P also placed rival Rio Tinto on Credit Watch Negative due to lower price forecasts for iron ore, aluminium and copper.

- Computershare (CPU) +2.84% has confirmed it is the preferred bidder to manage £30bn of mortgages from lenders Northern Rock and Bradford & Bingley for the UK government, which nationalised them at the beginning of the financial crisis. The deals will almost double the total value of the assets being managed by Computershare subsidiary Homeloan Management Ltd, which it bought in July 2014.

- Altium Technology (ALU) +12.17% after announcing a partnership with Dassault Systèmes for the new SOLIDWORKS electronic computer aided design product.

- National Bank (NAB) +0.29% will trade ex the Clydesdale Bank tomorrow. Exciting times. The bank also raised some business and farmers’ rates today on short term loans. Suspect that may have upset the RBA a little.

ECONOMIC NEWS

RBA decision in detail – The RBA meeting unequivocally retained an easing bias although didn’t quite deliver the rate cut some (a few) had hoped for, so the Aussie dollar went up on the news. Otherwise a read of the statement shows the RBA is reasonably upbeat on the Australian economy whilst concerned about emerging markets in China, commodity prices and inflation (or the lack of it). The message is that all the problems seem to be abroad as the non-mining side of the Australian economy does appear to be taking up some of the slack.

Some Quotes:

- The Economy is continuing to grow though at a slightly slower pace than earlier expected.

- China’s growth rate has continued to moderate.

- Financial markets have once again exhibited heightened volatility recently as Appetite for risk is diminished.

- Funding conditions for emerging market sovereigns have tightened.

- Some positive signs from the Australian economy – expansion in the non-mining sector of the economy strengthened; business conditions moved to above average; employment growth picked up; unemployment rate declined; pace of lending to business picked up.

- Inflation “quite low” at 1.7% for 2015. Likely to remain low for the next year or two.

- It is appropriate for monetary policy to be accommodated.

- Regulatory measures are working to contain the risks in the housing market.

- There are reasonable prospects for continued growth in the economy with inflation close to target.

- The current setting of monetary policy remains appropriate.

- Continued low inflation may provide scope for easier policy should that be appropriate.

Not much mention of the dollar this time round. Jobs numbers now seems to be the focus. Where jobs go, so will rates.

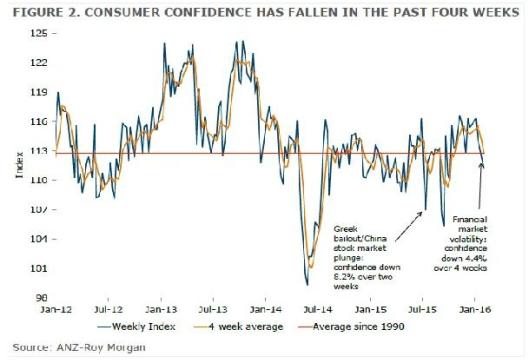

- ANZ-Roy Morgan Australian Consumer Confidence fell 1pt to 111.2 this week, and has fallen 4.4% over the past four weeks. On average, confidence was 2.1% lower in January compared to December.

In Asia

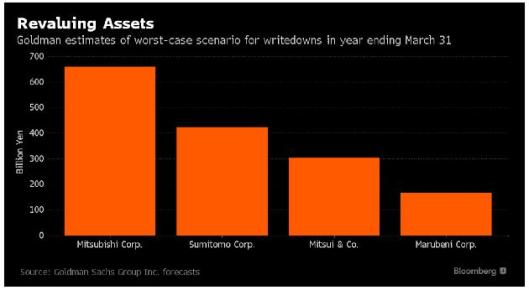

Australian banks are not the only ones with an exposure to resources. Seems our Japanese friends have some serious medicine to take in the current period. “Sogo shosha” are general trading houses like Mitsubishi Corp and Sumitomo and may be on the verge of a US$13bn collective write down.

We are going to hear a lot about write downs in the coming months.

The Bloomberg Commodity Index, a measure of returns from 22 items, has tumbled 40% over that period, touching the lowest level since January 1991.

Europe and US

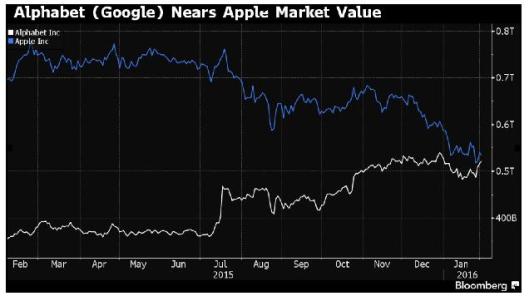

Alphabet (Google, not soup) is poised to become the biggest company in the world by value following figures on Monday night in the US.

Ahead in Europe

- FTSE -28.50 points.

- DAX -16.50 points.

- CAC -20 points.

Clarence

XXXX

Get a Global take on things at http://www.ntmarkets.com