Tags

abbott, anz, asx, Asx 200, ASX200, aussie dollar, australia, Australian Sharemarket, bank of england, banks, ben, Ben Bernanke, Bernanke, BHP, BHP Billiton Limited, billabong, boe, BOJ, BRU, cba, Charlie aitken, china, commonwealth bank, Commonwealth Bank of Australia, copper, CPU, crash, cyprus, diggers and dealers, dollar, dow, draghi, ECB, economy, essex Lion, eu, euro, europe, eurozone, fairfax, fed, finance, fmg, fomc, Fortescue, Fortescue Metals Group Ltd, Fortescue mining, france, gold, greece, igr, insurance, Interest Rates, iron ore, iron ore falls, italy, Japan, Macquarie Group Limited, Mario Draghi, marmota, meu, Mo farrah, NAB, National Australia Bank Limited, National Bank, nev power, Newcrest Mining Limited, oroton.qbe, qbe, RasPutin, RBA, Reserve Bank, results preview, RIO, Russia, SGP, shares, silver, Sirius Resources, slr, stevens, stock, stocks, super mario, telstra, Telstra Corporation Limited, ten, tinkler, TLS, twiggy, uk, Ukraine, wbc, WHC, Whitehaven Tinkler coal bid cash, Woodside Petroleum Limited, woolworths, wow, yellen, zombieland

Good afternoon,

A snapshot of today:

What happened today?

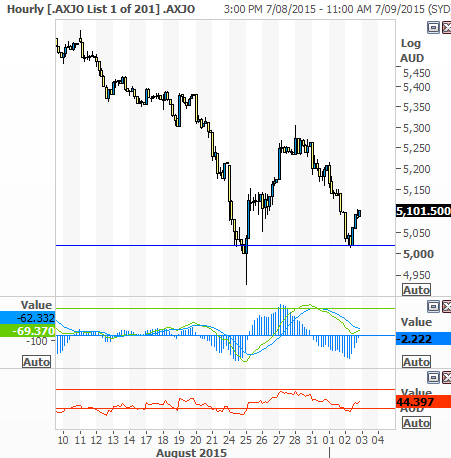

ASX 200 gains 5.1 points to close at 5101 (no conspiracy here) after a strong bank rally saves the day. US futures up 150 with China rallying to positive territory before they close for WWII holiday. Good volume in index futures and 80 point range as support holds.

Today the market staged a bigger come back than John Travolta. As China rallied from early losses and US futures remained positive, bargain hunters were back in for the banks and other defensives. We hit a low of 5015 but finished slightly up for the day after a late match out touch up to the magic 5101. A positive sign, but too early to get carried away. Volatility will continue until the Fed meeting and probably beyond. Conviction is still lacking and nerves frayed.

Support has held again

- Financials were the big comeback kids with both ANZ +1.29% and National Australia Bank (NAB) +0.99% turning positive. Commonwealth Bank (CBA) +0.45% flirted with the rights price at 7150 cents, hitting a low of 7222, and other financials like Platinum Asset Management (PTM) +4.28% and Henderson Group (HGG) +0.95% both escaped the selling.

- In the industrials, builders perked up on possible rate cuts, Fletcher Building (FBU) + 2.49%, James Hardie (JHX) +1.68% and Brickworks (BKW) +2.16% all putting in a strong day.

- Defensive sectors like Healthcare, CSL +1.3 % and Resmed (RMD) +1.39% will benefit from the lower AUD.

- Telcos though continued to be pressured as Telstra (TLS) –0.18% lost ground.

- In resource land, energy stocks fell hard early but did recover. Santos (STO) –0.84% rallied from an oversold position from yesterday. Big miners naturally were hit but again recovered on bargain hunting. BHP -0.08%, RIO +0.34% and South 32 (S32) -0.99%. Other resource stocks managed small gains, Sirius (SIR) +3.85%, Independence Group (IGO) +2.49% and Oz Minerals (OZL) + 2.59%.

- In one of the strangest corporate deals announced, Gerry Harvey has bought into a dairy and cattle business in the Goulburn Valley. Two strange things. One that Harvey Norman is interested in getting into the cattle business and the other that the seller is Gerry Harvey himself. Today HVN paid $34m for 49.9% and agreed to make an advance of $9m. Seems a long way from the normal activities of Harvey Norman (HVN) –3.25% and does raise some corporate governance issues.

- And news today from the Future Fund. Remember these were the guys that sold all their Telstra below 300 cents. Anyway, they have been piling up the cash in their investment portfolio as the risks outweigh the rewards. They did deliver a strong 15.4% return for the financial year to June 30, or $15.6 billion. Investment returns are now at $56.7bn, pushing its assets up to $117.2bn. It is now running at an 8% return against the benchmark of 7.1%

Economic News

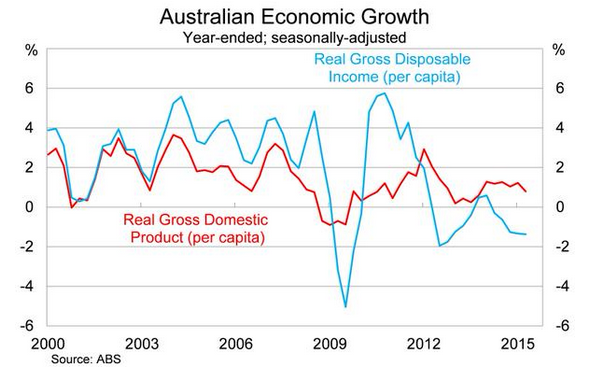

- GDP was the focal point today with 0.2% growth a big miss as exports fell. This means that the economy grew at 2% over the year, which opens the door to the RBA next time around. The AUD fell below 70 cents for the first time in six years as nominal GDP growth was the weakest since 1962.

A similar look to the GDP growth and the chart of the AUD

- In Asian markets, we saw a good rebound after early losses but the afternoon brought back some selling. Japan tried hard to rally on the back of a weakening yen as the cost of insuring debt in the region climbed to a 17 month high.

- Shanghai was -1.07%, Japan -0.39% and Hong Kong – 0.13%. Some food for thought…even after the 25% fall in Chinese markets in the last two months, shares on mainland exchanges are still more than twice as expensive as their identical counterparts in Hong Kong. Dual-listed companies traded at an average 115% premium in China at the end of last month, within three percentage points of a four-year high in July, according to monthly data compiled by Bloomberg.

Early calls for the European Markets from IG

- FTSE up 14

- DAX up 19

- CAC up 11

And finally, September has started badly but historically it can get worse. The average fall is around 5.3% when the first day starts so badly.

- But for the optimists amongst us, Morgan Stanley has issued a rare BUY alert after the recent rout. This is the first time since early 2009, effectively calling the bottom of this summer’s equity slump.

- Morgan Stanley said that all five of its market-timing signals are now flashing a buy signal as selling-fever reaches capitulation levels. This is a rare occurrence, typically leading to a V-shaped recovery that delivers a 23pc gain in stock prices over the following 12 months.

Which is fine, but the same bank also downgraded its ASX 200 target to 5150 for the next 12 months. Looks like International ETF’s it is, and those exposed to the US dollar.

Clarence

XXXX