Tags

abbott, anz, asx, Asx 200, ASX200, aussie dollar, australia, Australian Sharemarket, bank of england, banks, ben, Ben Bernanke, Bernanke, BHP, BHP Billiton Limited, billabong, boe, BOJ, BRU, cba, Charlie aitken, china, commonwealth bank, Commonwealth Bank of Australia, copper, CPU, crash, cyprus, diggers and dealers, dollar, dow, draghi, ECB, economy, essex Lion, eu, euro, europe, eurozone, fairfax, fed, finance, fmg, fomc, Fortescue, Fortescue Metals Group Ltd, Fortescue mining, france, gold, greece, igr, insurance, Interest Rates, iron ore, iron ore falls, italy, Japan, Macquarie Group Limited, Mario Draghi, marmota, meu, Mo farrah, NAB, National Australia Bank Limited, National Bank, nev power, Newcrest Mining Limited, oroton.qbe, qbe, RasPutin, RBA, Reserve Bank, results preview, RIO, Russia, SGP, shares, silver, Sirius Resources, slr, stevens, stock, stocks, super mario, telstra, Telstra Corporation Limited, ten, tinkler, TLS, twiggy, uk, Ukraine, wbc, WHC, Whitehaven Tinkler coal bid cash, Woodside Petroleum Limited, woolworths, wow, yellen, zombieland

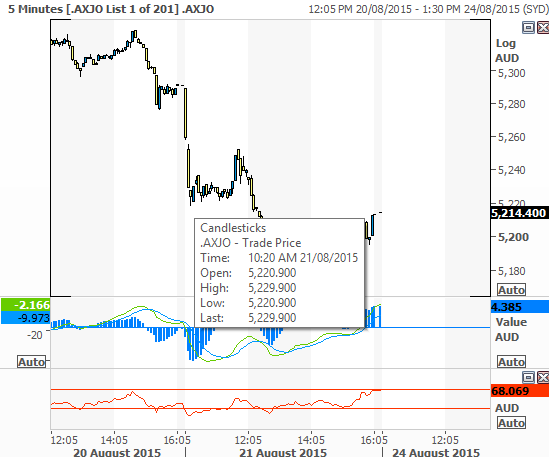

ASX 200 loses 74 points to 5214.6 as a late rally helps, after plunging 117 points at one stage, on weak overseas leads and big volume. China falls again on a worrying PMI miss. Resources outperformed on better commodity prices with results continuing to drive volatility. US futures down 97.

- Another shocking day coming on the back of a bad night on Wall Street. The market opened weaker especially in the financials with the resources holding up well, well relatively well, but news at 11.30 from China on another big miss on the Caixin PMI number. The number came in at 47.1 and the hitherto solid resource stocks threw in the towel and the market collapsed. The only bright spot was in gold shares on the safe-haven allure of the metal.

- Financials continued under serious pressure with CBA -0.74% outperforming the other three which fell around 3.5%. The rudimentary measure we sometimes use is the basket of banks. The big four can now be bought for a total of around $166 having topped out in April/May at $212. Insurers also bore the brunt of the selling following disappointing results from IAG -5.15%. Macquarie Group (MQG) –3.55% and other wealth managers IOOF –1.86 % Management and Magellan Financial (MFG) –5.95% were the worst performers in financials. Medibank Private (MPL) +13.43% bucked the carnage on better than anticipated results and now are above the issue price again. Insurance premiums are up by 5.3% and cost cutting has paid off it seems. Revenue was sluggish but the market was happy to ignore for the time being and look to the solid cost cutting and premium increases.

ASX Financials ex REITS

- In the industrial space, broad losses across the board spread like a virus with few pockets of green poking through. Healthcare usually a defensive sector failed to provide any solace with Mesoblast (MSB) -5.26% and heavyweight CSL –2.01%. Other industrials to shake off the gloom were Coca-Cola Amatil (CCL) +2.69% following better than expected numbers. The food sector was also providing some comfort with Bellamy’s (BAL) +6.72% reporting stronger profit numbers and dragging Select Harvests (SHV) +4.91% and Huon Aquaculture (HUO) +1.75%. Telecoms which are supposed to be defensive were also in the spotlight as Telstra (TLS) –0.82%, M2 Group (MTU) –4.33% and TPG Telecom (TPM) –2.13% suffered, however Spark NZ (SPK) +10.98% issued some solid if unspectacular guidance helping sentiment considerably.

- In resource stocks, iron ore producers gave up early gains with BHP –1.15% continuing to slide with RIO +0.22% outperforming but Fortescue Mining (FMG) –1.29% in trouble again. Energy shares were dominated by the Santos result (STO) -0.18% after worse numbers than expected but importantly no rights issue and also the surprise exit of long-time CEO David Knox. Liquefied Natural Gas (LNG) once again hit hard as profit taking in the high flyers continues. Some base metals stocks were helped by better underlying metal prices with Sandfire (SFR) +8.22%, Sirius (SIR) +5.86% and Independence Group (IGO) + 5.81%. Sims Metals (SGM) +11.19% also doing well today on the result.

Results today included

- IAG –5.15 % – Natural disaster claims and increasing competition, have taken a toll on Insurance Australia Group’s earnings, posting a $1.1 billion full-year insurance profit, down from $1.6 billion in 2014.IAG recorded a net profit of $728 million for the year ended June 30, a plunge from the $1.2 billion it made in financial 2014. The group suffered a “significant increase” of $495 million in natural peril claims costs, lower net reserve releases, and more competition in commercial insurance. The company will pay investors a 16 cents per share dividend, bringing the full year payout to 29 cents per share – lower than the 39 cents per share posted in 2014.

- Santos (STO) -0.18 % shocked the market not just with the result but importantly David Know the long-time CEO has fallen on his sword, and there will be a ‘Strategic Review’ with a new CEO sought. It seems the market has taken this, and comments about asset sales, that this has put the company up for sale.

- CCL +2.69% – A rebound in profits in Indonesia offset continued weakness in Australia,pushing June-half net profit up 0.9 % to a better than expected $183.9 million. Guidance from management for mid-single-digit growth in 2016. Indonesian profits jumped 46.4 % and New Zealand and Fiji up 9.9 %, countering a 6.1 % slide in Australia. Earnings in alcohol and coffee, rose 30.4 %, while earnings from food and services, which includes SPC Ardmona, edged up 1.5 %.The June-half net profit result was well ahead of market consensus forecasts around $173.5 million and EBIT forecasts around $300 million.

- Sims Metal (SGM) + 11.19% returned to profit last fiscal year, as the company cut operating costs and recorded better earnings from its European and North America metals businesses. They reported a net profit of $109.9 m for the year through June. That compared to an A$88.9m loss in the same period a year earlier. Sims said it would pay an interim dividend of 13 cents.

- Also today Apple managed to raise more than $3bn from fixed income fund managers. Apparently they were killed in the rush.

- Asian markets were once again weak as the current currency dislocation and equity meltdown continues. China fell 3.29% , Japan down 2.6% and Hong Kong down 2.3%.Tellingly maybe, Ellerston Asian Investment has increased the size of its IPO to $120m from $100m on increased appetite from investors looking for exposure to Asia.

- According to some commentators, this is the one chart you need to see to explain the global sell-off.

We disagree, this is equal as telling. The line in the sand for the Chinese authorities fighting the malicious criminal short sellers on ‘Judgement Day’. Let’s hope it holds.

- The weekend should prove a circuit breaker in the market and next week we may see some bargain hunters emerge especially in the banking sector which is massively oversold. Volume was big today around $9bn so we may see this as a blow off dip! It has been a long week and analysts will be looking forward to the end of reporting season. We know we are!

- And finally in a sweeping reform GST will be applied to all sales from overseas from July 2017.Local retailers will be popping champagne corks tonight. They just have to hold on until then!