Tags

abbott, anz, asx, Asx 200, ASX200, aussie dollar, australia, Australian Sharemarket, bank of england, banks, ben, Ben Bernanke, Bernanke, BHP, BHP Billiton Limited, billabong, boe, BOJ, BRU, cba, Charlie aitken, china, commonwealth bank, Commonwealth Bank of Australia, copper, CPU, crash, cyprus, diggers and dealers, dollar, dow, draghi, ECB, economy, essex Lion, eu, euro, europe, eurozone, fairfax, fed, finance, fmg, fomc, Fortescue, Fortescue Metals Group Ltd, Fortescue mining, france, gold, greece, igr, insurance, Interest Rates, iron ore, iron ore falls, italy, Japan, Macquarie Group Limited, Mario Draghi, marmota, meu, Mo farrah, NAB, National Australia Bank Limited, National Bank, nev power, Newcrest Mining Limited, oroton.qbe, qbe, RasPutin, RBA, Reserve Bank, results preview, RIO, Russia, SGP, shares, silver, Sirius Resources, slr, stevens, stock, stocks, super mario, telstra, Telstra Corporation Limited, ten, tinkler, TLS, twiggy, uk, Ukraine, wbc, WHC, Whitehaven Tinkler coal bid cash, Woodside Petroleum Limited, woolworths, wow, yellen, zombieland

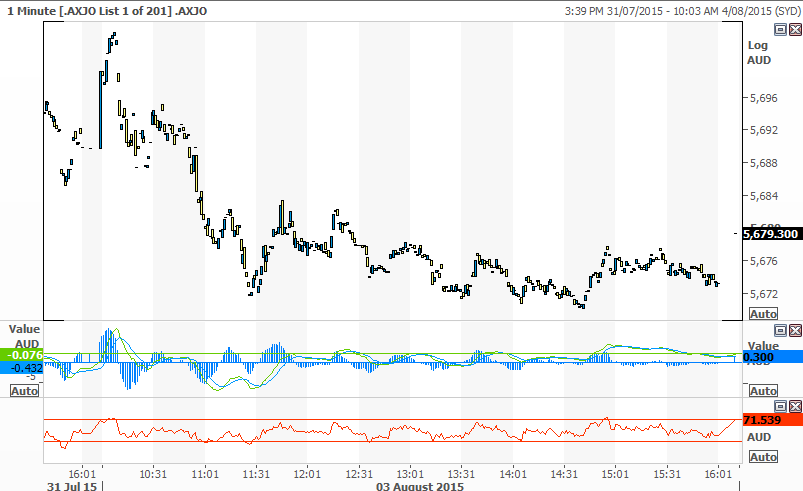

ASX 200 closes down 19.9 at 5679.3.Chinese official PMI lowest since 2011.Dow futures down 7. Big week ahead.

The action today

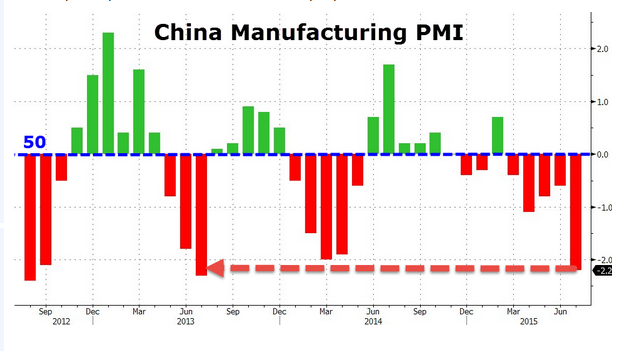

Looking like it is trying to break out A quiet dull start top the week as mining shares came under pressure due to commodity price falls and soft China data. A ‘Bank’ Holiday in NSW didn’t help volumes as we set ourselves up for a big week of economic data and the kick off in results. BHP – 1.02% reversed its recent thrust as did RIO -1.25% with results on Thursday and South32 (S32) -3.36 % having another shocking day. Diggers and Dealers kicked off today in Kalgoorlie with a number of small/mid cap gold miners presenting like Independence Group (IGO -5.82 %) ,Kingsgate (KCN) +1.52 % and Gold Road ( GOR) unchanged Energy stocks also were weaker as oil prices continue to fall, Oilsearch (OSH) – 2.81% were the biggest loser in large caps with small oilers falling heavily too as Australia Worldwide Exploration (AWE) – 4.76%, Sundance Energy (SEA) -6 %, Beach Petroleum (BPT) – 5.64% fare the worst. Financials eased back with more modest falls in Westpac (WBC) -0.03 % and Australia and New Zealand Bank (ANZ) unchanged outperforming their peers as they fell around 0.5%.Insurers though fared much better led by Suncorp (SUN) +0.42 % reporting tomorrow and potential special dividend perhaps? Insurance Group Australia (IAG) unchanged and even Medibank Private (MPL) +0.96 %. In the industrial landscape, gaming stocks found favour with Crown Resorts (CWN) +0.44 %, Aristocrat (ALL) +0.58 % and Echo Entertainment (EGP) +1.99 % all doing well. Other discretionary consumer stocks also in the green with JB Hi Fi (JBH) +0.47 %. Huge move from cloud collaborator for the global construction industry ,Aconex (ACX) + 12.61 % after talking record volumes of new business and positive cash flow of around $4.7m in their quarterly last Friday. Market star CSL -0.13 % came in for some profit taking as they struggle to break through the magic $100 level. News that they had completed the Novartis Influenza vaccine business acquisition fell on deaf ears. In corporate news Affinity Education (AFJ) + 11.49 % already under siege from G8 Education (GEM) +2.94 % are now under even more pressure following a cash alternative, to the scrip bid, of 80c.The stock is still trading above the bid price but with GEM having 19.9% it is hard to see them slipping through their embrace. Skilled Group (SKE) +2.92 % will book an impairment charge of up to $67 million, which has been triggered by the merger proposal by rival Programmed Maintenance (PRG) + 4.6 % to form an enlarged $700-million plus labour hire firm. IOOF (IFL) unchanged after being back in the media today as Senate hearings resume. PwC is yet to start its second ‘independent’ review nearly 5 weeks after the company announced they would do so. Always hard to be truly independent when the company is paying and frames the terms of reference for the inquiry. A copy of the first PwC report showed only two of the 13 allegations were investigated and the review scope was limited in a way that meant PwC were not allowed to interview the complainant, the person who was alleged to have done the wrong doing, or any member of the research team. Their emails, computers and other trading accounts were also not reviewed by PwC. Pretty limited review really and will not be a good look in the media. A new CEO for Federation Centres (FDC) – 4.33 % today with Angus McNaughton filling the spot from Novion replacing Stephen Sewell in a shock announcement. Sewell was the architect of the merger with Novion to create the country’s second biggest property trust with assets of around $22bn. Freelancer suspended today pending a capital raising. Two days after reporting a record result for the first half with revenue up 40% to $16.8m yet still a loss of around $800,000.Looks like a placement at around 135censt is on the cards to raise $10m and also a sell down of substantial shareholder Simon Clausen to raise another $30m In economic news, July ANZ job ads fell for the first time since March slipping 0.4% but remaining 9.3% ahead of the year on year number at 146,121.The RBA meets tomorrow but is odds on to keep rates unchanged yet again. Unemployment numbers are due on Thursday and we expect those to remain steady at 6%. Inflation numbers today from TD Securities/Melbourne Institute advancing 0.2% over the month and 1.6% for the year. Property rates and charges (+3.3 per cent), other food products (+5.5 per cent) and non-alcoholic beverages (+2.8 per cent). These were offset by price falls in water and sewerage (-3.6 per cent), alcohol and tobacco (-1.6 per cent), and automotive fuel (-2.3 per cent). Looks like buying pressure is easing ever so slightly in Sydney and Melbourne property as all the banks have now raised rates for investor loans. The Clearance rate in Sydney and Melbourne both fell this weekend,however house prices ran another 2.8% in July with Melbourne marginally ahead (up 6.1%) of Sydney (up 5.4%) as RP Data values Aussie homes at a massive $6 Trillion. Not even sure how many zeros there are in $6 Trillion! HSBC reported a 10 per cent increase in earnings for the first half of the year, boosted by bumper profits in Hong Kong. They also announced the sale of its Brazil unit to Banco Bradesco SA for 17.6 billion reais ($7 billion). Pre-tax profits in the six months to the end of June were $US13.6 billion, up from $US12.3 billion a year earlier and well above analysts’ average forecast of $US12.5 billion. In Asia, China once again continued its fall after the underwhelming official Caixin/Markit PMI number today coming in at 47.8, the lowest reading since November 2011.

Looking like it is trying to break out A quiet dull start top the week as mining shares came under pressure due to commodity price falls and soft China data. A ‘Bank’ Holiday in NSW didn’t help volumes as we set ourselves up for a big week of economic data and the kick off in results. BHP – 1.02% reversed its recent thrust as did RIO -1.25% with results on Thursday and South32 (S32) -3.36 % having another shocking day. Diggers and Dealers kicked off today in Kalgoorlie with a number of small/mid cap gold miners presenting like Independence Group (IGO -5.82 %) ,Kingsgate (KCN) +1.52 % and Gold Road ( GOR) unchanged Energy stocks also were weaker as oil prices continue to fall, Oilsearch (OSH) – 2.81% were the biggest loser in large caps with small oilers falling heavily too as Australia Worldwide Exploration (AWE) – 4.76%, Sundance Energy (SEA) -6 %, Beach Petroleum (BPT) – 5.64% fare the worst. Financials eased back with more modest falls in Westpac (WBC) -0.03 % and Australia and New Zealand Bank (ANZ) unchanged outperforming their peers as they fell around 0.5%.Insurers though fared much better led by Suncorp (SUN) +0.42 % reporting tomorrow and potential special dividend perhaps? Insurance Group Australia (IAG) unchanged and even Medibank Private (MPL) +0.96 %. In the industrial landscape, gaming stocks found favour with Crown Resorts (CWN) +0.44 %, Aristocrat (ALL) +0.58 % and Echo Entertainment (EGP) +1.99 % all doing well. Other discretionary consumer stocks also in the green with JB Hi Fi (JBH) +0.47 %. Huge move from cloud collaborator for the global construction industry ,Aconex (ACX) + 12.61 % after talking record volumes of new business and positive cash flow of around $4.7m in their quarterly last Friday. Market star CSL -0.13 % came in for some profit taking as they struggle to break through the magic $100 level. News that they had completed the Novartis Influenza vaccine business acquisition fell on deaf ears. In corporate news Affinity Education (AFJ) + 11.49 % already under siege from G8 Education (GEM) +2.94 % are now under even more pressure following a cash alternative, to the scrip bid, of 80c.The stock is still trading above the bid price but with GEM having 19.9% it is hard to see them slipping through their embrace. Skilled Group (SKE) +2.92 % will book an impairment charge of up to $67 million, which has been triggered by the merger proposal by rival Programmed Maintenance (PRG) + 4.6 % to form an enlarged $700-million plus labour hire firm. IOOF (IFL) unchanged after being back in the media today as Senate hearings resume. PwC is yet to start its second ‘independent’ review nearly 5 weeks after the company announced they would do so. Always hard to be truly independent when the company is paying and frames the terms of reference for the inquiry. A copy of the first PwC report showed only two of the 13 allegations were investigated and the review scope was limited in a way that meant PwC were not allowed to interview the complainant, the person who was alleged to have done the wrong doing, or any member of the research team. Their emails, computers and other trading accounts were also not reviewed by PwC. Pretty limited review really and will not be a good look in the media. A new CEO for Federation Centres (FDC) – 4.33 % today with Angus McNaughton filling the spot from Novion replacing Stephen Sewell in a shock announcement. Sewell was the architect of the merger with Novion to create the country’s second biggest property trust with assets of around $22bn. Freelancer suspended today pending a capital raising. Two days after reporting a record result for the first half with revenue up 40% to $16.8m yet still a loss of around $800,000.Looks like a placement at around 135censt is on the cards to raise $10m and also a sell down of substantial shareholder Simon Clausen to raise another $30m In economic news, July ANZ job ads fell for the first time since March slipping 0.4% but remaining 9.3% ahead of the year on year number at 146,121.The RBA meets tomorrow but is odds on to keep rates unchanged yet again. Unemployment numbers are due on Thursday and we expect those to remain steady at 6%. Inflation numbers today from TD Securities/Melbourne Institute advancing 0.2% over the month and 1.6% for the year. Property rates and charges (+3.3 per cent), other food products (+5.5 per cent) and non-alcoholic beverages (+2.8 per cent). These were offset by price falls in water and sewerage (-3.6 per cent), alcohol and tobacco (-1.6 per cent), and automotive fuel (-2.3 per cent). Looks like buying pressure is easing ever so slightly in Sydney and Melbourne property as all the banks have now raised rates for investor loans. The Clearance rate in Sydney and Melbourne both fell this weekend,however house prices ran another 2.8% in July with Melbourne marginally ahead (up 6.1%) of Sydney (up 5.4%) as RP Data values Aussie homes at a massive $6 Trillion. Not even sure how many zeros there are in $6 Trillion! HSBC reported a 10 per cent increase in earnings for the first half of the year, boosted by bumper profits in Hong Kong. They also announced the sale of its Brazil unit to Banco Bradesco SA for 17.6 billion reais ($7 billion). Pre-tax profits in the six months to the end of June were $US13.6 billion, up from $US12.3 billion a year earlier and well above analysts’ average forecast of $US12.5 billion. In Asia, China once again continued its fall after the underwhelming official Caixin/Markit PMI number today coming in at 47.8, the lowest reading since November 2011.  As we go to press, it is off another 2.32%

As we go to press, it is off another 2.32%  The Shanghai market since April Japanese manufacturing activity expanded at the fastest pace in five months in July though not as much as initially expected, a private survey has showed, suggesting economic growth may be slowly recovering after an expected second-quarter slump. The final Markit/Nikkei Japan Manufacturing Purchasing Managers Index (PMI) was a seasonally adjusted 51.2 in July, slightly below a preliminary reading of 51.4 but above a final 50.1 in June. Oil look set to continue its move down with WTI declining to $46.72 a barrel on news from Iranian Oil Minister Bijan Namdar Zanganeh,who said output could increase by 500,000 barrels a day within a week after international sanctions are eased and by 1 million barrels a day within a month after that. Sanctions against Iran’s oil industry should be lifted by late November, he said Heading into the European session we shall hopefully see the Greek stock market open. Seems we have been writing about the impending reopening for some time but tonight it looks like it really is going to happen. Predictions of a fall of around 20% look a tad overdone and would expect some vultures to appear and try to pick the bottom in this one. It has been five weeks since the stock market closed and negotiations continue on the austerity measure s and the bailout. Unfortunately for Greece almost all of the bail out money actually goes to paying back interest to the banks that fell over themselves to lend them money at rate bordering on criminal in the various crisis they have gone through. Should be fun to watch but no effect on major markets.

The Shanghai market since April Japanese manufacturing activity expanded at the fastest pace in five months in July though not as much as initially expected, a private survey has showed, suggesting economic growth may be slowly recovering after an expected second-quarter slump. The final Markit/Nikkei Japan Manufacturing Purchasing Managers Index (PMI) was a seasonally adjusted 51.2 in July, slightly below a preliminary reading of 51.4 but above a final 50.1 in June. Oil look set to continue its move down with WTI declining to $46.72 a barrel on news from Iranian Oil Minister Bijan Namdar Zanganeh,who said output could increase by 500,000 barrels a day within a week after international sanctions are eased and by 1 million barrels a day within a month after that. Sanctions against Iran’s oil industry should be lifted by late November, he said Heading into the European session we shall hopefully see the Greek stock market open. Seems we have been writing about the impending reopening for some time but tonight it looks like it really is going to happen. Predictions of a fall of around 20% look a tad overdone and would expect some vultures to appear and try to pick the bottom in this one. It has been five weeks since the stock market closed and negotiations continue on the austerity measure s and the bailout. Unfortunately for Greece almost all of the bail out money actually goes to paying back interest to the banks that fell over themselves to lend them money at rate bordering on criminal in the various crisis they have gone through. Should be fun to watch but no effect on major markets.