End of day stock market report 26 June 201526th June 2015

The ASX 200 closed down 87 points. Things just went from bad to worse!

The Horror!

The Horror!

The market today seemed to wake up with an almighty hangover. Maybe it was the Stockbrokers Awards last night in Sydney or just the never ending disappointment with our Greek friends but whatever it was it was like a bear with a sore head. From the opening bell it seemed like a rush to see who could get out the quickest, especially in the yield stocks. Lots of ex dividends in the REITs and other leaders didn’t help but BHP -3.54%, RIO -2.79% and the banks bore the brunt. Nowhere was safe except perversely Woolworths (WOW) +3.83% which perked up mainly on the back of some rumours of Private Equity running the slide rule across them for a takeover. Barbarians at the Checkout!

It seemed from the open that a fund was very keen to liquidate a largish portfolio weighted towards yield and with volumes thin due to fence sitting and school holidays, it did not take much to spook the cattle. Options expiry yesterday pushed up the volumes this morning on the open as exercise and assignment notices were put through the market. This weekend is shaping up as make or break for the latest Greek negotiations and no one wanted to be Odysseus.Who can blame them as once again we are poised on the precipice with the Germans and the Greeks at ‘Groggerheads’.

As we approach the end of financial year, it is worth looking at the performance of the ASX 200 over the year. We closed June 2014 at 5525 and today we are up a massive 24 points for the year. Within that there have been some winners and losers. In fact the last week has seen some extreme volatility in some of the year’s winners.

The ASX200 Rollercoaster continues

The ASX200 Rollercoaster continues

It has been a torrid week with a number of former high flyers getting walloped. SEEK(SEK) -1.70%, Slater and Gordon (SGH) -0.40% and Flight Centre (FLT) +3.32% and today it was Bradkens’ turn (BKN) -11.34%, resuming after suspension with news of a $70m joint debt package from a Chilean firm combined with CHAMP. Bradken expects its annual underlying earnings to fall by up to 21% in the current financial year, and has forecast only a slight earnings improvement in the 1H of 2015/16. It will also include a write-down of up to $145m in its 2014/15 accounts, which will further damage its bottom line. It is possible the joint Chilean/CHAMP injection may lead to a merger. At first glance it seemed good news but the market ran a mile anyway.

Winners today were hard to find and most were just bounce backs from nasty falls this week like OzForex (OFX) +2.75% and IOOF (IFL) +1.43%

In other news today Australia Post joined the chorus of laying staff off, with news that they were letting 2000 employees go over the next three years. With losses in its mail delivery business approaching $500 million this financial year, and more than $1.5 billion over the past five years, the redundancies will be purely voluntary. Apparently.

Good news for Telstra (TLS) -1.43% as the ACCC and the Tax office announced they had no objections to the company’s deal to lease its copper wiring to the government for $11bn.

It seems too that the Tax Office is clamping down on the cash economy as 250,000 building contractors have been issued with please explain and pay notices totalling around $2.3bn.So as Joe gives with one hand, those having a ‘red hot go’ are being whacked with the other red right-hand.

HSBC has cut its Australian growth forecast to 2.4% from 2.6% for 2015 because of lower expectations for Chinese economic growth and a lack of investment spending by businesses, which it sees as part of a global phenomenon. Amazingly Paul Bloxham from HSBC had an interest rate rise slated for 2016. Not so after this revision.

Chinese stocks had another horrible day as the government stayed mum about recent falls and the market fell 5.33%. Morgan Stanley came out this morning and forecast a 30% fall in the ‘ShangLow’ Index after the 1245% rally this year. Once again unwinding of margin positions seemed to have driven it lower, as the authorities struggle to deflate the bubble without anyone noticing. It seems that the mums and dads are hoping for some guidance from the authorities on the market direction but sadly this time there is no government put to help them out. Japan continued to buck the trend with a holding pattern.

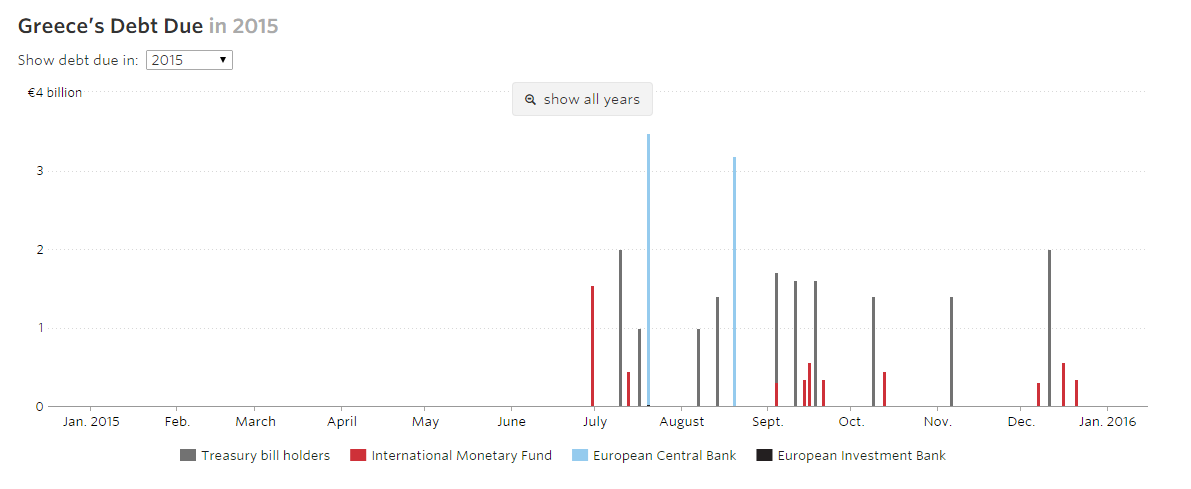

It would be good to think that by Monday the whole Greek issue would be sorted. Fingers crossed but even if this deadline is met, there is another debt repayment around mid July for around $3.5bn. I guess the only good thing is that they can use the $7.5bn they are asking for this time to pay the next instalment in this giant money go round. It certainly is bizarre.

If they do not come to an agreement by Monday they will be issued with an ‘In Arrears‘ notice from the lender, the IMF, and then have 2 weeks before they get a cable from Washington (yes, a cable) stressing how serious it is and if then they don’t pay another cable two weeks later informing them they are overdue in their payment.The situation can be maintained as long as the ECB continues to underwrite the Greek banking system. If they withdraw support, dust off your Drachmas!

This unfortunately is only the start of the repayment schedule as we can see below (and that’s just 2015!). But let’s not spoil the weekend completely.

Clarence

Xxx

Read more at marcustoday.com.au