The ASX 200 jumped 190 points to 8672 (2.2%) right out of the blocks this morning on US/Iranian news and a spectacularly strong US bounce. End of month and short covering helping. Resources roared back to life as the USD fell slightly, and oil prices steadied. BHP up 4.3% and RIO up 3.5% with FMG joining in up 3.8%. Lithium stocks raced ahead, PLS up 3.5% and MIN rising 5.2% with the gold sector rebounding hard. NEM up 4.5% and EVN jumping 8.2% on gold and copper rises. S32 jumped on aluminium exposure, rare earths also doing well, ARU up %. Uranium stocks rallied hard, PDN up 6.9% and NXG jumped 6.7%. Oil and gas stocks took a pause, STO up 0.1%. Coal stocks steady.

In the banks, a decent rise with the Big Bank Basket at $290.26 (+2.0%).MQG soared 3.3% and other financials also did well, ZIP up 10.7%. REITs mixed, GMG rising 2.3%. Tech stocks gained, XRO up 2.5% and REA up 2.5%. Retail better, JBH up 1.4% and travel stocks jumped, FLT up 4.8% and QAN taking off. The All-Tech Index up 3.3%.

In corporate news, APE rose after entering into agreements to acquire two Audi dealers in Melbourne. PRN rose 4.1% on a new CEO. SGR blipped 8.7% higher after Chow Tai Fook Enterprises and Far East Consortium took full control of Brisbane’s Queen’s Wharf precinct.

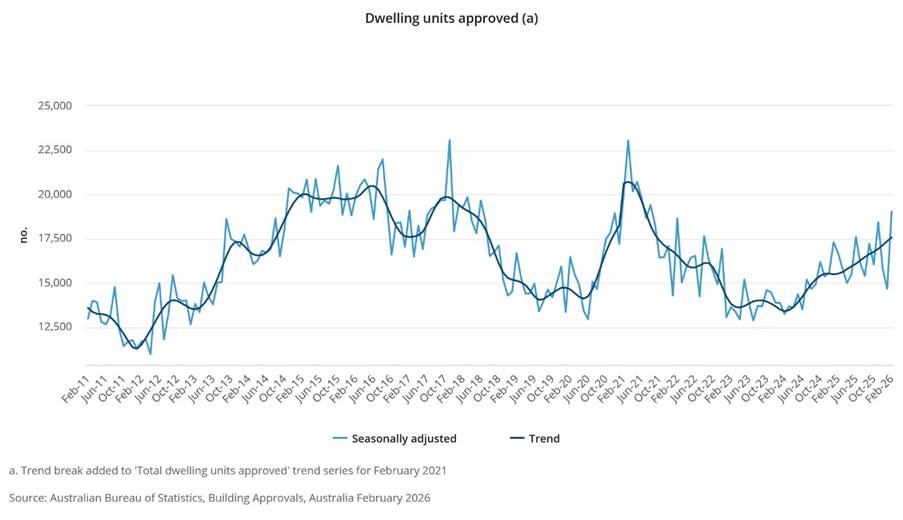

In economic news, dwelling approvals rose 29.7% in February to 19,022, driven by a surge in private apartments.

Asian markets eased, Japan rose 4.6%, HK up 2.0%, and China up 1.4%.

10 -year yields fell to 4.91% on peace hopes.

US futures: Dow up 45, Nasdaq up 92.

HIGHLIGHTS

- Winners: HMC, GGP, EOS, CHN, WIA, DVP, ZIP.

- Losers: PXA, LIN, DTR, EQR, CKF, KAR, TLX

- Positive Sectors: Banks. Iron ore. Gold Miners. Uranium. Lithium.

- Negative Sectors: Nothing.

- ASX 200 Hi 8672 Lo 8606. Optimism builds. Closes on highs.

- Big Bank Basket: Rises to $290.26 (+2.0%)

- All-Tech Index: Up 3.3%

- Gold: Jumps to $6801

- Bitcoin: Rallies to $68504

- 10-year yields: Falls to 4.91%

- AUD: Rises to 69.12c.

- Dow up 44, Nasdaq up 92.

MARKET MOVERS

- PDI +10.1% gold rally.

- EOS +12.7% defence spending.

- ZIP +10.7% buyback update.

- ARU +8.9% executes binding cornerstone equity agreements.

- GGP +14.9% great bounce on production recently.

- SGQ +13.0% slays that dragon. Partners with Boston Metals.

- EUR +11.9% buyback update.

- QOR +7.1% buyers return.

- STN +7.8% MT write up!

- ATX +12.8% another kick higher. In Biotech Basket.

- PXA -14.7% response to ASX query. Undisclosed information abounds.

- DTR -5.5% placement.

- LIN -13.6% oversubscribed placement at 75c.

- ETM -41.9% Kvanefjeld project update.

- Yesterday’s Hero: MCE – unchanged.

- Speculative Stock of the Day: Nothing on any volume.

ECONOMIC AND OTHER NEWS

- Australian Building approvals – Total dwellings approved rose 29.7% to 19,022.

- Prime Minister Anthony Albanese will address the nation this evening at 7pm. Fuel restrictions could be in place after Easter.

- Citi economists expect the Reserve Bank of Australia to lift interest rates by a further 0.25% in June in addition a previously forecasted increase priced in for May.

- Trump says US could withdraw from Iran ‘whether we have a deal or not’.

- The President to address the nation tomorrow.

- OpenAI raises $3bn from retail investors as part of record funding haul.

- Judge halts construction of Trump’s $400mn White House ballroom.

- Nike shares fall on unexpected forecast for sales decline.

- Italy fails to make it to the World Cup yet again.

- Japan deploys first long-range missiles as it steps up deterrence.

- Trump on Tuesday signed an executive order restricting mail-in voting.

And finally…..

Tiger woods is in the news this morning for crashing his SUV. I think it’s time he started using a driver .

Clarence

XXXXX