The ASX 200 slipped again by 19 points to 8800 (0.2%) as CBA continued to weigh, off another 3.1% with the Big Bank Basket down to $279.76 (-1.6%). Joining in the casualty list were 360 off 13.1% on disappointing numbers and ALL down 7.5% as it came up lemons. Our dismal tech sector continues to slide as XRO head lower still, off 2.2% and WTC down 0.8%. REA fell 2.5% and CAR down 1.0%. Industrials were ok, TCL up 0.5% and WES gaining 0.7% with COL and WOW better, TLS gained another 0.4%. GYG continue to be wrapped lower, down 2.0% and TPW also fell hard today, off 4.4%.

In resource land, iron ore improved in Asian trade, BHP up 0.6% and RIO sprinting 2.3% ahead. Gold miners were modestly better, NST up 1.4% and EVN up 2.0%. Lithium stocks better, LTR up 6.1% on its new auction platform, MIN roared 9.2% ahead on selling part of its lithium business to POSCO. LYC slid 2.7% with uranium stocks weaker. Oil and gas stocks better with WDS up 1.4%. Coal stocks weaker.

In corporate news, FLT rose 1% on an earnings update, NWL fell 0.4% after surviving a protest vote at the AGM, MP1 resumed trade after capital raising. A1N dropped 9.7% on much weaker ad revenue. DMP rose 1.8% after an AGM update.

In economic news, investor loan numbers, in Asia hopes for more Chinese stimulus helped iron ore prices higher.

Asian markets mixed, Japan up 0.8%, HK up 0.4% and China down 0.4%.

10-year yields steady around 4.39%

HIGHLIGHTS

- Winners: MIN, DTR, GNG, LTR, CNI

- Losers: 360, SRL, ALL, MI6, ZIP, CU6, TLX

- Positive Sectors: Oil and gas. Iron ore. Gold miners. Lithium.

- Negative Sectors: Banks. Tech. Old ‘Skool’ Platforms.

- ASX 200 Hi 8844 Lo 8805

- Big Bank Basket: Down to $279.76 (-1.6%)

- All-Tech Index: Down 2.0%

- Gold: Drifts to $6301

- Bitcoin: Falls to US$103232

- AUD: Steady at 65.19c.

- Asian markets mixed, Japan down 0.1%, HK up 0.6% and China down 0.4%.

- 10-year yields steady around 4.37%

- US futures – Dow up 31 Nasdaq up 69.

- European markets set to open firmer.

MARKET MOVERS

- DTR +8.8% volatility to the upside.

- MIN +9.2% POSCO deal.

- LTR +6.1% auction site.

- GNG +6.9% Ausbiz shout out!

- SPL +15.6% good volume too.

- STK +8.8% exceptional gold at Gradina.

- G50 +10.0% to present at MS Symposium.

- MYX +1.7% FDA to remove ‘Black Box’ markings.

- 360 -13.1% results disappoint.

- SRL -9.0% volatility continues.

- ALL -7.5% comes up lemons with results.

- MI6 -6.4% falls undercover.

- CRS -6.7% high-grade results extension.

- ZIP -5.4% falls continue.

- Casualty of the Day: 360 -13.1% Results weigh.

- Speculative Stock of the Day: Nothing on any volume.

ECONOMIC AND OTHER NEWS

- The Australian exchange-traded fund (ETF) market has swelled to a total of $322 billion, driven by a record $6bn in net inflows during October, according to the latest Global X report. The market has grown by 38.4% over the past year.

- The number of new investment loans rose by 13.6% to 57,624 in September quarter 2025.

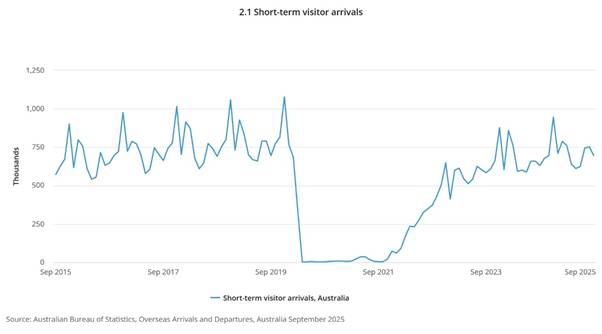

- The ABS reports that foreign visitor arrivals to Australia returned to pre-COVID levels in September, led by strong traffic from New Zealand. China remained below pre-pandemic levels at 83,000 visitors, compared with 99,000 in 2019.

- SoftBank shares plunge as much as 10% after selling Nvidia stake.

- Iron ore futures prices gained on Wednesday, as hopes of fresh stimulus from top consumer China outweighed concerns over a gloomy outlook.

- The most-traded January iron ore contract on China’s Dalian Commodity Exchange (DCE) rose 1.18% to 772.5 yuan ($US108.45) a metric ton, its highest since November 7.

- Trump hints at cutting tariffs on India as loyalist Sergio Gor sworn in as ambassador.

- New Indian IPO ‘Billionbrains Garage’ rose 22% on debut!

- Toto Wolff in talks to sell part of Mercedes F1 stake to CrowdStrike chief at $6bn valuation.

- Chinese bitcoin fugitive jailed in UK over Ponzi scheme.

- China’s cybersecurity agency accused the American government of orchestrating the theft of about $13bn worth of Bitcoin, representing China’s most recent attempt to attribute major cyberattacks to the US.

And finally….

Clarence

XXXX