Tags

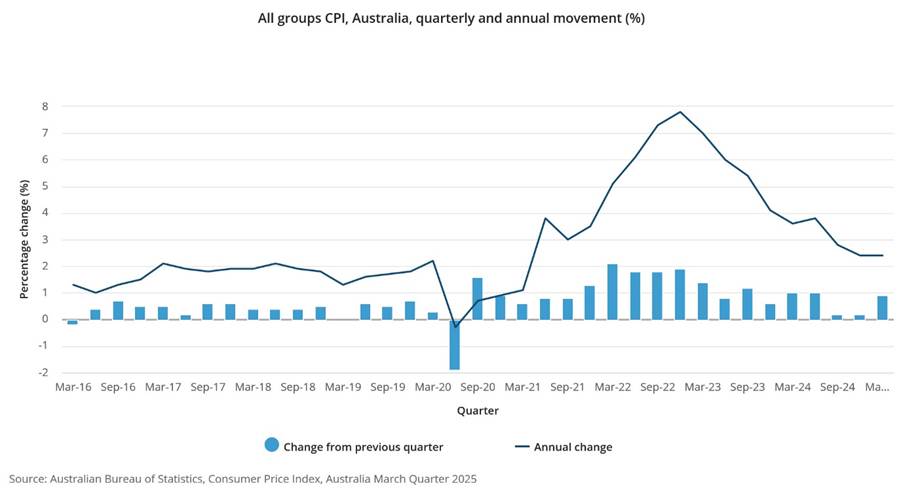

The ASX 200 finished the month up 56 points to 8126 (0.7%) giving us a 3.7% rise for the month. Hard to believe really. A 14% rally off the lows. CPI today came in slightly higher than some expected but clears the way for a rate cut next week. Banks celebrated with CBA pushing 2.2% higher, NAB up 0.5% and the Big Bank Basket up to $265.43 (+1.6%). Other financials were a little mixed, MQG fell 0.5% despite good numbers from UBS. Insurers better, SUN up 2.3% and REITs also going well. GMG up 1.9% and SGP up 1.3%. Industrials firmed with retail again doing better, JBH up 0.7% and WES up 1.6%. COL reported today and eased 0.8%. BXB starting to find support, ALL up 1.9% and Tech doing ok, WTC up 1.0% and the Index up 1.2%. Resources took a breather today as the shorts backed off on the buying, uranium stocks fell back a little as did gold miners, NST still suffering from soft quarterly down another 3.5%. FMG gave back some of yesterday’s gains, down 1.1% and S32 fell 1.1%. BHP and RIO were relatively steady. Lithium stocks slipped a little, PLS down 2.3% and MIN unchanged after the big rally yesterday. JHX finding support up 1.2%. In corporate news, plenty of quarterlies, ORG fell 1.4% on its weaker quarterly. SGR unchanged despite news that losses increased. On the economic front, the local CPI came in at 0.9% and 2.4% for the year, giving the RBA a reason to be cheerful. Meanwhile in China, factory activity fell. No surprise there really. Asian markets were firm, 10 -year yields slipped to 4.17%.

HIGHLIGHTS

- Winners: DVP, PXA, QAL, LLC, BVS, MP1, IGO, A4N

- Losers: CYL. LTR, OBM, ALK, PDN, MXG, AMC, BPT

- Positive Sectors: Banks. Healthcare. REITs. Retail.

- Negative Sectors: Gold miners. Oil and gas. Lithium. Utilities.

- ASX 200 Hi 8126 Lo 8069 – Narrow range. 3.7% for the month.

- Big Bank Basket: Jumps to $265.43(+1.6%)

- All-Tech Index: Up 1.2%

- Gold: Steady at $5160

- Bitcoin: Steady at US$94992

- 10-year yield falls to 4.17%.

- AUD: Eases to 64.09c

- Asian markets: Japan up 0.5%, China down 0.1% and HK up 0.3%.

- Dow futures down 72 Nadaq down 96

MARKET MOVERS

- DVP +5.5% kicks higher again.

- PXA +5.4% FCA approvals for UK sale and purchase product.

- SBM +7.4% quarterly report and Simberi update.

- OCC +8.9% Remplir approved in Canadian market.

- TYR +9.5% takeover talk.

- ZEO +7.8% quotation of securities.

- BOT +2.3% ceasing to be a substantial shareholder.

- CYL -9.4% sell-off gathers pace.

- LTR -7.9% sellers back.

- OBM -6.1% production downgrade.

- PDN -4.4% shorts back off.

- AMC -3.7% 425 ruling.

- MAP -24.4% Q4 FY 25 report.

- 29M -11.1% broker downgrades.

- NMG -16.7% drilling complete.

- APX -9.6% quarterly report.

- Speculative Stock of the Day: WOA +31.48% – Trading halt – Offtake/Distribution agreement pending.

ECONOMIC AND OTHER NEWS

The Consumer Price Index (CPI) rose 0.9% this quarter. Over the twelve months to the March 2025 quarter, the CPI rose 2.4%. The most significant price rises this quarter were Housing (+1.7%), Education (+5.2%) and Food and non-alcoholic beverages (+1.2%).

The stage is set for a rate cut next week.

China’s factory activity slipped into the worst contraction since December 2023.

New export orders fell to the lowest since December 2022 and recorded the biggest drop since April that year.

- China is days late in releasing trade data as US shipping slumps.

- Starbucks’ profit slumps as costs mount from turnaround effort.

- European futures opening unchanged. Earnings in focus. Auto giant Volkswagen posts 37% drop in first-quarter profit.

- UBS beat bottom line expectations amid sharp returns in investment banking while warning of the global trade impact of sweeping U.S. tariffs as it seeks to rein in steep share declines.

- Microsoft and Meta after the bell in the US today.

- Trump’s first 100 days mark worst for US stock market since Gerald Ford.

And finally…..

Clarence

XXXXX