The ASX 200 dropped 30 points to 7969 (0.4%) as the banks came under a little pressure on car tariffs in the US. The Big Bank Basket rose to $245.27 (+0.1%). Financial services also under some pressure as the OPT fall out continues. MQG down 1.1% and GQG off 1.8%. PNI also falling 3.5%. REITs also under some pressure with GMG falling 4.0% as data centre growth seems to be questioned. SCG off 1.4% and GPT down 2.0%. Tech is also under pressure with WTC off 2.0% as AussieSuper sells out on government issues. The All –Tech Index down 2.6%. REA and CAR fell too with DHG down 4.9% on CoStar revised bid being best and final. Retail down too with car stocks sliding, APE off 2.7%, BAP down 2.5% and ARB down 2.0%. Resources were holding their end up, gold miners pushing ahead again, NEM up 0.7% and NST up 0.8%. GOR rose 3.9% as shareholders urged the board to engage. LTR up 1.5% and MIN slightly firmer. BHP, RIO and FMG seeing small gains. JHX finding some support up 2.1% with uranium shorts back in control. BOE falling 5.0% and NXG off 0.3%. Oil and gas better WDS up 1.5%. In corporate news, TRS soared 109.5% on a huge premium bid from Dollarama. RPL fell another 8.9% as OPT fall out continues. DVP quashed rumours on BGL contract. Nothing significant on the economic front although it looks like Albanese will call an election tomorrow for May 3rd. Asian markets were weaker with car makers under pressure. Japan down 0.9%, HK up 1% and China up 0.4%. 10-year yields 4.50%

HIGHLIGHTS

- Winners: HLS, CYL, RHC, MAH, MAD, GOT, RSG

- Losers: FFM, TUA, RPL, VUL, EBR, PME, ZIP

- Positive Sectors: Gold miners. Oil and gas. Lithium.

- Negative Sectors: Financials. Tech. REITs.

- ASX 200 Hi 7989 Lo 7936

- Big Bank Basket: Rises to $245.27(+0.1%)

- All-Tech Index: Down 2.6%

- Gold: Rises to $4809

- Bitcoin: Steady at US$87531

- 10-year yield higher at 4.50%.

- AUD: Steady at 63.10c

- Asian markets: HK and China Firmer, Japan down 0.9%.

- Dow futures up 130 Nasdaq down 8

MARKET MOVERS

- TRS +109.5% Dollarama bids.

- HLS +10.7% update and special dividend.

- GOR +3.9% media speculation.

- RHC +6.2% defensive perhaps.

- COG +15.5% change in substantial holding.

- SBM +11.6% change in substantial holding.

- BKY +7.7% thin and volatile.

- TUA -9.0% broker downgrades.

- RPL -8.9% under pressure again.

- FFM -11.2% profit taking.

- PME -7.8% buyback update.

- VUL -8.0% profit taking.

- CAT -5.0% investor day presentation.

- FND -4.8% SPP booklet.

- Speculative Stock of the Day: Nothing on any volume.

ECONOMIC AND OTHER NEWS

- PM Albanese is set to call an election tomorrow. May 3rd.

- Pengana freezes its unlisted High Conviction Equities Fund redemptions as it braces for big Opthea (OPT) loss. 44.7% of its portfolio invested in healthcare companies such as Opthea and Clarity Pharmaceuticals (CU6). Other positions include Greatland Gold and IperionX (IPX).

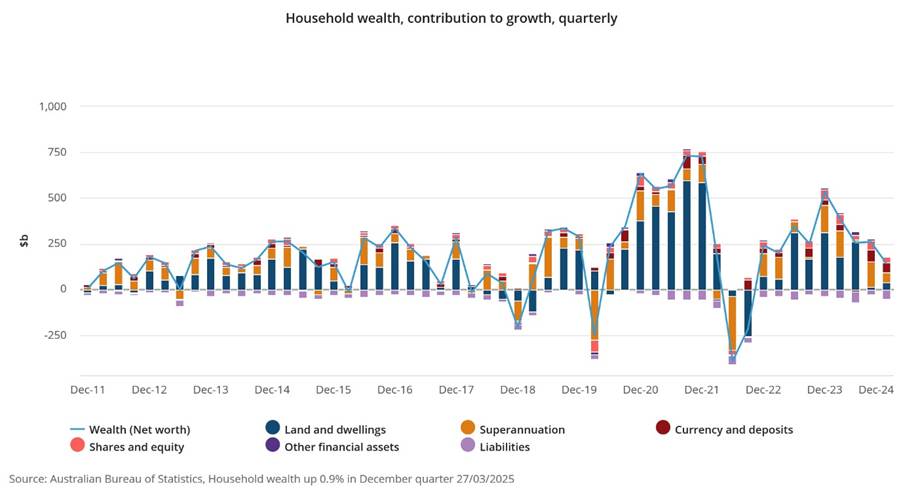

- Household wealth was up 0.9% or $143.6bn in December quarter 2024, the lowest growth since September quarter 2022.

- Profits at major Chinese industrial firms dipped 0.3% in the first two months this year, after three consecutive years of sharp declines, supported by improved profitability in manufacturing and raw material sectors.

- China has told state-owned firms to hold off on any new collaboration with businesses linked to Li Ka-shing and his family. This follows its ports deal in Panama.

- OpenAI is close to finalizing a $40bn funding round led by SoftBank Group Corp. — with investors including Magnetar Capital, Coatue Management, Founders Fund and Altimeter Capital Management.

- TSMC’s $100bn pledge to Trump will not revive US chipmaking, says ex-Intel chief.

- EU calls for households to stockpile 72 hours of food amid war risks.

- Sweden to increase defence spending sharply to 3.5% of GDP.

And finally….

Don’t you think it’s wrong that only one company makes the game Monopoly!

I’ve been prescribed anti-gloating cream.

I can’t wait to rub it in.

Clarence

XXXXX