ASX 200 fell 63 points to close at 7062 (0.9%) on weaker international leads and falling commodity prices. RBA left rates unchanged again, but limited ASX reaction. Resources hit hard with iron ore miners under pressure, BHP down 1.3% and FMG off 0.9%, Lithium stocks remain depressed with IGO falling 6.7%, PLS down 8.5% and MIN copping a 4.3% fall. Gold miners retreated from the heady times of yesterday with NST down 4.0% and NEM slipping 2.7%. EVN raising $525m for an acquisition. Oil and gas stocks also fell hard as crude failed to launch, WDS down 2.7%, STO off 0.9% and coal stocks also down. Industrials held up in places, WOW and COL showed modest gains, WES fell only 0.6% despite its lithium exposure, tech saw profit taking, WTC down 1.0% and XRO off 1.0% with the All–Tech Index down 0.8%. Healthcare better with RMD up 1.8% as the recovery continues. Banks eased back slightly with the Big Bank Basket down to $179.29c (). MQG fell 0.7% and insurers eased back again. In corporate news, ORG returned after the cunning Plan A was rejected by Aussie Super and rallied 2.2%, CMM dropped 8.4% on some director selling, same with 360 falling % and MSB returned from its 150th capital raise and dropped 18.0%. MPL up 0.3% on an agreement to increase stake in My Health. On the economic front, the much-anticipated Xmas present from Michele was delivered with a pause in rate rise. Not much movement on this AUD slid around 0.5% and 10-year yields at 4.41%. Asian markets weaker with Japan down 1.1%, China off 0.8% and HK down 1.8%.

HIGHLIGHTS

- Highs: URW, IFM, RFF, CRN, ORG, NAN

- Lows: CXO, LTR, PLS, CMM, CTT, IGO

- Positive sectors: Healthcare. Utilities.

- Negative sectors: Iron ore. Gold. Lithium. Oil and gas. Financials. Tech.

- Big Bank Basket: Slightly lower at $179.29

- All-Tech Index: Fell 0.8%

- Gold: Eases back to $3088

- Bitcoin: Off highs at US$41,784

- AUD: Lower at 65.84c post RBA decision.

- Asian markets: Japan down 1.1%, China off 0.8% and HK down 1.8%

- US futures: Dow Futures Down points Nasdaq down 40.

MAJOR MOVERS

- SMR +1.9% bounced back from yesterday’s loss.

- ORG +2.2% Plan A fails. Broker upgrades.

- COH +1.7% investors listening.

- EEG +17.7% gas plant acquisition yesterday.

- EXP unchanged- broker upgrade.

- CHN -4.5% poisoned again.

- RSG -3.3% golds suffer.

- CXO -9.8% broker downgrades.

- LTR -9.2% searching for lows.

- CMM -8.4% director sales.

- PLS -8.5% shorts winning.

- IGO -6.7% the sell-off continues.

- MIN -4.3% hitting year lows.

- MSB -18.0% another capital raise sinks shares.

- RDN -16.3% multiple lithium soil anomalies at Mt Sholl.

- SBM -9.3% gold losses.

- Speculative Stock of the Day: Alterity Therapeutics (ATH) +75.0% ahead of webinar.

COMPANY NEWS

.png)

ECONOMIC AND OTHER HEADLINES

RBA leaves rates unchanged.

- Sees High Level of Uncertainty Around Outlook for China

- Decision to Hold Rates Steady Will Allow Time to Assess Impact of Prior Hikes

- Job Market Conditions Continue to Ease Gradually

- Wages Growth Not Expected to Increase Much Further

- Measures of Inflation Expectations Consistent With Targets

- Recent Data in Line With Central Bank’s Expectations

- Whether Further Rate Hikes Are Needed Will Depend on Data

- RBA Cash Rate Target Unchanged at 4.35%

Click here for the full announcement.

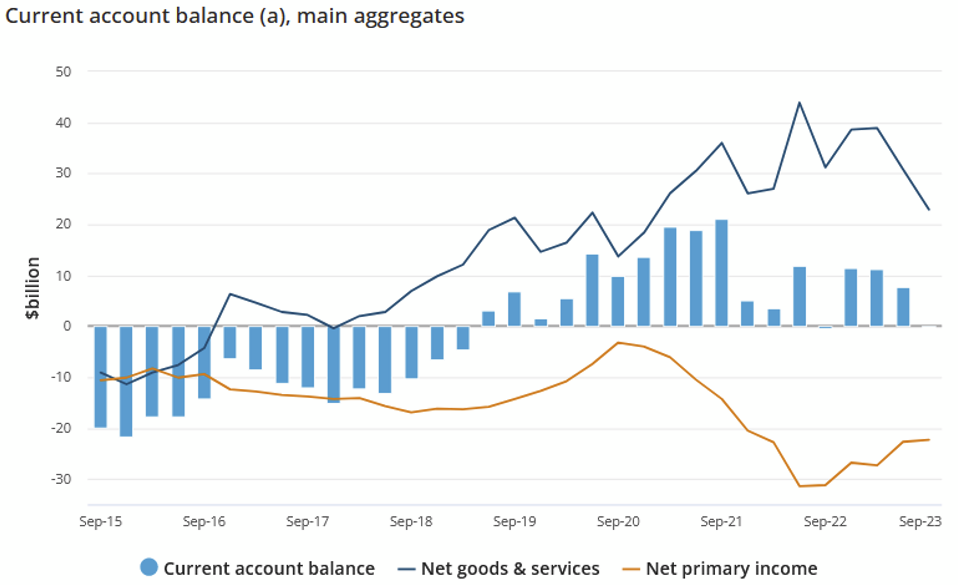

- The current account balance, seasonally adjusted, fell $7,940m to a deficit of $158m.

- “The current account deficit reflected a reduced trade surplus, driven by falls key export commodities prices, while the net primary income deficit narrowed slightly.”

- The capital and financial account surplus was $3,124m, a turnaround of $20,261m on the June quarter 2023 deficit.

- The net international investment liability position was $814,685m at 30 September 2023.

- Fortescue (FMG) has shipped its first batch of African iron ore from the Belinga iron ore project in Gabon.

- The Caixin China services purchasing managers’ index for November climbed to its highest in three months, diverging from China’s official PMI reading that showed a contraction.

- This private survey reading came in at 51.5 in November rising from 50.4 in October and 50.2 in September.

HEADLINES

- Japan’s business activity contracted for the first time this year, according to the au Jibun Bank.

- The inflation rate for Japan’s capital, Tokyo, came in at 2.6%, down from the 3.3% in October.

- South Korean inflation fell to 3.3% for November, coming in below expectations and marking its first decline in three months of acceleration.

- US funding for Ukraine set to run out by end of the year, White House warns.

- US Supreme Court grapples with Sackler liability releases in Purdue bankruptcy.

- Roche to buy Carmot for up to $3.1bn as race for obesity drugs intensifies.

- Nvidia will build a network of semiconductor plants in Japan in partnership with the country’s companies to meet demand for artificial intelligence-powering graphics chip.

- This week’s GOP presidential primary debate will have the smallest stage yet, with just four candidates facing off Wednesday night.

- The Premier League sold four years of UK broadcast rights for £6.7bn(US$8.4bn), mostly to its biggest existing partners Sky Sports and TNT Sports.

- Qatar sells down Barclays stake.

- And finally…..

- Clarence

- XXXX