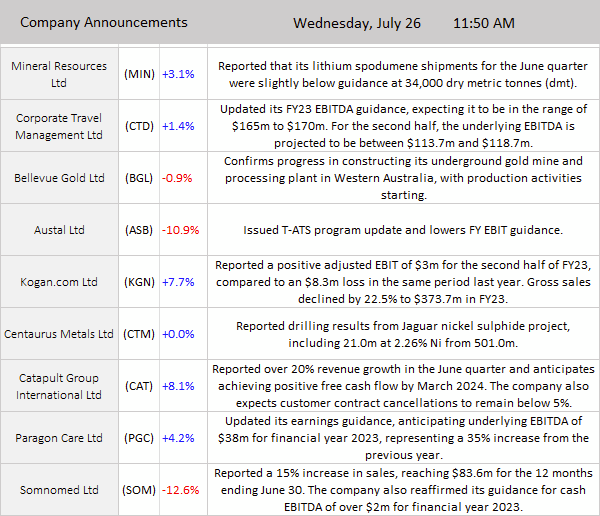

ASX 200 closed up 62 points to 7402 (+0.9%), hitting a five-month high, while the Aussie dollar and bond yields fell on softer-then-expected inflation data reducing pressure on the RBA to tighten policy further. Miners continued their rally today on China’s stimulus pledge, sector majors BHP up 2.3%, RIO gained 1.4% and FMG up 2.3%. Banks up today, recovering yesterday’s losses, with the big four all in positive territory, all gaining over 1.5%. Big Bank Basket up to $180.59 (+1.1%). Tech stocks good, WTC +2.4%, ALU +1.9%, and XRO up 0.7%. Consumer discretionary sector jumped on inflation results, LOV up 3.6%, PMV up 2.8% and WES +1.1%. Energy stocks energetic, BPT up 6.9%, STX +2.3%, and WHC gained 1.8%. Gold struggling to find momentum ahead of Fed meeting tonight. Healthcare sector continues to struggle, CSL off 1.0%. REITS down despite a fall in bond yields, GMG and SCG both down 1.1%. Lithium miners clocked a second great day, with LTR, AKE and PLS up another 1.4%, 2.5%, and 4.6%, respectively. In corporate news, KGN jumped 10.0% on good results, BGL down 0.3% on construction update, CTD +0.9% on increased EBITDA guidance, MIN up 4.1% despite missing lithium shipments guidance, ASB fell 10.5% after lowering FY EBIT guidance, and CAT rose 5.7% after reporting a 20% growth in revenue. In economics, local inflation cools down. Q2 CPI fell to 6.0%, beating expectations of 6.2%, down from 7% in the previous quarter. Monthly CPI came in lower as well at 5.4% in June from 5.5% in May, matching expectations. Bond traders pricing in a 54% chance of a rate hike by the RBA next week. Asian markets are down letting go of yesterday’s gains, Japan down 0.1%, HK off 0.7%, with China slipping 0.5%. Australia’s 10Y yield down to 4.01%. Dow Jones futures down 24 points, and Nasdaq futures down 28 points. European markets opening flat. Earnings in focus.

HIGHLIGHTS

- Winners: KGN, BPT, WGX, JIN, CIA, REG, PLS

- Losers: ASB, GRR, AAC, DVP, IMU, SYA

- Positive sectors: Banks. Iron ore. Lithium. Oil and gas. Retailers.

- Negative sectors: REITs. Healthcare (CSL really)

- High 7421 Low 7340. CPI number spurs rally.

- Big Bank Basket: Lower at $178.60 -0.6% 180.59 1.1

- All-Tech index: Unchanged.

- Gold steady at $2902

- Bitcoin: Eases to US29145

- Aussie Dollar: Steady at 67.67c

- 10-Year Yield: Flat at 4.01%

- Asian markets: Japan unchanged HK down 0.7%, China down 0.5%

- US Futures: Dow down 11 Nasdaq down 20

- European markets opening flat to unchanged. Earnings in focus.

MAJOR MOVERS

*Rio numbers just out and look at little below forecasts. Div US177c. Forecast US180c.- Net cash generated from operating activities of US$7.0bn. Iron ore looks good.*

- KGN +10.0% positive business update

- BPT +6.9% 4Q activities report.

- CIA +5.4% iron ore run.

- WGX +6.2% June Quarter update.

- LRS +1.5% quarterly.

- PLS +4.6% brokers warm to it.

- MIN +4.1% Quarterly update.

- JIN +6.0% Jackpot time. I’m in!

- ONE +15.0% bounces back on quarterly.

- QOR +14.3% Quarterly.

- PLY +10.6% new ‘Dumb Ways to Die’ coming.

- MAF -0.6% fund lock up.

- ASB -10.5% big profit hit.

- CXL -3.4% very low volume.

- VNT -1.0% Index effect didn’t last.

- GRR -5.2% Quarterly report.

- AAC -4.6% Joe Lewis gets charged with alleged inside trading.

- WA1 +8.1% drilling commencement at P2.

- MVP -7.7% continues to unwind.

- AMA -16.7% another smash, no repair on ASX query.

- DTZ -16.3% capital raise.

- PAN – IGO will not invest in cap raise even at 5c.

- Speculative Stock of the Day: CDX +18.2%. Not great volume but good announcement on a filing for a Nasdaq listing. CDX is a medical technology company focused on developing vascular biomarkers.

COMPANY NEWS

ECONOMIC NEWS

- Australian CPI comes in at 6% bearing forecasts of 6.2%. Sparks rally. RBA less likely to raise rates next week.

.png)

.png)

- Goldman Sachs has trimmed its call for the peak cash rate from 4.85% to 4.6%.

- CBA cutting jobs across the board. At least 100 staffers are understood to have lost their jobs.

- RBC Capital’s economics team said the Reserve Bank may lean to an “uneasy pause” on August 1.

HEADLINES

ASIAN MARKETS

- The Chinese administration has appointed the country’s top diplomat Wang Yi to succeed Qin Gang as foreign minister after he went MIA for a month.

- Investment banks warn investors of potential BoJ surprise

US AND EUROPEAN HEADLINES

- Fed is widely expected on Wednesday to approve what would be the 11th interest rate increase since March 2022. It will take its benchmark borrowing rate to a target range of 5.25%-5.5%. Highest since 2001.

- Deutsche Bank AG weathered the trading slowdown better than analysts had expected.

- Unicredit posts stronger results. Santander beats too.

- Nat West Chief Executive Officer Alison Rose is stepping down after a row over the way the British bank closed accounts held by politician-turned-pundit Nigel Farage.

- British billionaire Joe Lewis has been charged with insider trading in the US.

- Britain’s wealthiest man, Gopichand Hinduja, condemned the U.K.’s departure from the European Union as a bad decision,

- California’s main power grid operator issued an emergency watch notice as people cranked up the air con.

And finally…..

I went to a fancy dress party dressed as an alarm clock. I left early. People kept winding me up!

Had a game of football in a quarry last week, we lost 4-3 on aggregate.

Whoever stole my copy of Microsoft 365, I will find you!

You have my word.

Clarence

XXXX